| 2020 | 2021 | ||||||

| Price: | 1,983.00 | EPS | 0 | 0 | |||

| Shares Out. (in M): | 146 | P/E | 0 | 0 | |||

| Market Cap (in $M): | 2,750 | P/FCF | 0 | 0 | |||

| Net Debt (in $M): | 10,300 | EBIT | 0 | 0 | |||

| TEV (in $M): | 13,050 | TEV/EBIT | 0 | 0 | |||

| Borrow Cost: | General Collateral | ||||||

Sign up for free guest access to view investment idea with a 45 days delay.

Description

Recommendation: Short Showa Denko (4004 JP) equity

Thesis Summary

Showa Denko (4004 JP) is a short because 1) following the completion of its expensive, debt-financed acquisition of a commodity chemical business, the pro forma entity is far more expensive and levered than the market likely perceives; and 2) the profitability of its largest segment is declining precipitously this year and will remain anemic going into next year as peak profitability from the prior two years rolls over as a result of coronavirus-driven demand destruction and high graphite electrode inventory levels.

-

Pro forma for its expensive, debt-financed acquisition of commodity chemical business Hitachi Chemical, Showa Denko trades for a far higher multiple and is significantly more levered than standalone Showa Denko figures would suggest. Despite the tender offer being completed on April 20, much of the the sell-side has yet to recast their numbers and targets based on the pro forma entity, leading to an information vacuum that has likely temporarily obscured how the acquisition has significantly altered Showa Denko’s leverage and valuation profile. In our experience investing in Japan, we’ve found sell-side analysts and other market participants in the region to be unusually slow at reacting to fundamental developments. On our estimates, the pro forma entity has a staggering 11.1x turns of leverage on 2020 EBITDA and 8.7x turns based on our normalized EBITDA estimate.

-

As a result of collapsing steel demand due to COVID-19 and high levels of graphite electrode inventory at steelmakers heading into the virus-driven demand destruction, the spread between graphite electrode and needle coke prices (the primary driver of profitability for Showa Denko’s largest segment) has collapsed from ~$8,000/tn in 2019 to ~$3,000/tn currently. Based on our work and industry checks, we expect this subdued spread to persist throughout 2020 and into 2021, meaning Showa Denko will face a significant decline in operating earnings just as it levered up for an expensive acquisition – a toxic combination for the equity.

At 10x (slightly over one standard deviation above standalone Showa Denko’s average historical multiple) our estimated pro forma EBITDA assuming a $4,500/tn spread between graphite electrode and needle coke prices, the stock would be worth ~¥1,050, representing 54% downside. The pro forma entity currently trades at 6.4x – in-line with Showa Denko and Hitachi Chemical’s blended average multiple – on 2019 EBITDA figures that reflect near-peak graphite electrode segment profitability. As such, downside to a short position should be relatively limited even if the market completely looks through the impact of the coronavirus on 2020 numbers and is willing to value the business based on historical (peak) profitability.

Thesis Points Detail

The pro forma entity is far more expensive and levered than is likely perceived by the market

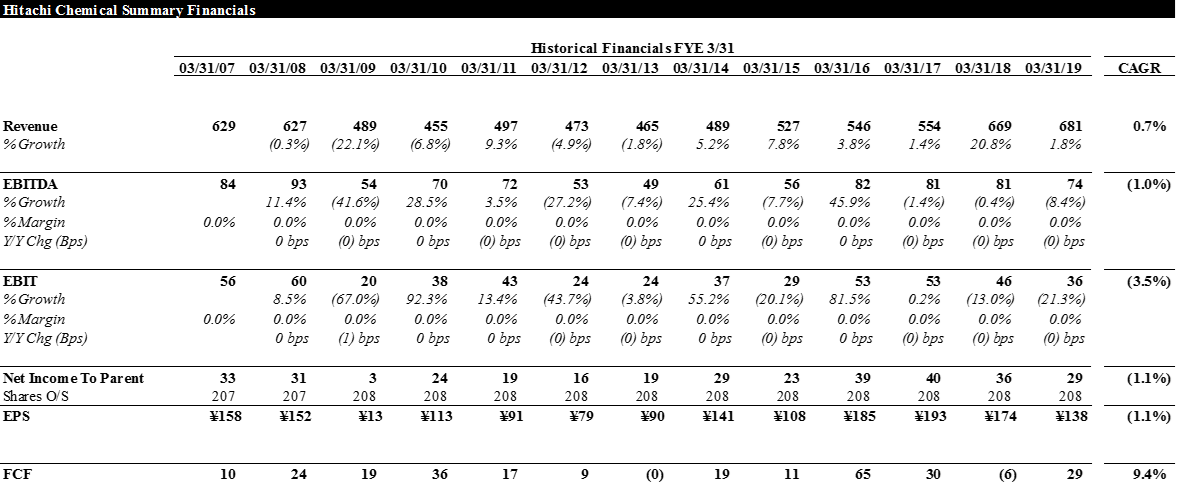

- Hitachi Chemical is a commodity chemical business that’s exhibited anemic revenue growth and FCF conversion over the last decade. Despite its uninspiring long-term track record, Showa Denko paid ~14x LTM EBITDA for the business, a significant premium to Hitachi Chemical’s historical average multiple in public markets (5.4x EBITDA) as well as Showa Denko’s own historical average multiple (7.2x EBITDA average).

-

Despite management touting ¥20bn in synergies, Showa Denko and Hitachi Chemical’s business lines have little overlap and the cited sources of expected synergies are questionable. Even taking the ¥20bn synergy target at face value, the post-synergy EBITDA multiple is ~11x, still a significant premium to Hitachi Chemical’s historical average and an expensive multiple considering Showa Denko is paying roughly a market multiple for a significantly below-average business.

-

Showa Denko took on significant debt to consummate the acquisition. Specifically, the acquisition was financed with:

-

¥400bn Non-Recourse Term Loan (at SPC/subsidiary level)

-

¥295bnbn Senior Loan (at parent level)

-

¥275bn of preferred shares (at SPC/subsidiary level)

- Leverage and valuation multiples for the pro forma entity are substantially higher than standalone Showa Denko numbers would imply

-

Leverage: Pro forma net debt / EBITDA on trailing numbers is 4.8x vs. just 0.7x for the standalone entity. However, given our view around the decline in operating earnings Showa Denko will face as a result of the coronavirus, leverage on our estimated 2020/normalized pro forma EBITDA is 11.1x and 8.7x, respectively, for a business whose components have historically traded at 7.2x (Showa Denko) and 5.4x (Hitachi Chemical).

-

Valuation Multiples: The pro forma entity trades at 6.1x trailing EBITDA vs. 2.5x using standalone Showa Denko figures. Based on our 2020 estimates, pro forma EV/EBITDA is 14.0x.

- Despite the tender offer being completed on April 20, much of the sell-side has yet to recast their models and target prices based on the pro forma entity, leading to an information vacuum that has likely caused many market participants to overlook how the Hitachi Chemical acquisition has significantly altered Showa Denko’s leverage and valuation profile. In our experience investing in Japan, we’ve found sell-side analysts and other market participants in the region to be unusually slow at reacting to fundamental developments. For example, when we reached out to the Jefferies analyst that covers Showa Denko to ask them how they derived their ¥4,100 price target (as their most recent notes haven’t included an enterprise value to equity value bridge), we received the following reply (emphasis added):

“We’ve been quite late to update our numbers on 4004 due to uncertain market conditions. As of Feb, we have Y120bn EBITDA, based on $7.8k/t GE vs. $2.8k/t NC prices. Also this does not include Hitachi Chem. GE price/demand environment has been very shaky due to the pandemic.” - In other words, Jefferies hasn’t updated their numbers for either the transformative (in this case, for the worse) acquisition of Hitachi Chemical or the major demand destruction in Showa’s key commodity. While some other sell-side analysts have updated their targets, many others remain behind the curve. As sell-side analysts update their models and the market digests the impact of the Hitachi Chemical acquisition, analysts and market participants will be forced to acknowledge the significantly higher leverage and valuation multiples of the new entity.

Profitability of Showa Denko’s largest segment is under significant pressures this year and next

- The profitability of Showa Denko’s graphite electrodes segment (its largest business, accounting for ~43% of pro forma trailing EBITDA) has decline significantly in 2020 vs. 2019, and our diligence suggests that this weakness will persist into 2021. This is primarily the result of the confluence of two main factors:

-

Collapsing steel demand as a result of the coronavirus

-

High graphite electrode inventory levels at steelmakers going into the period of demand destruction. These high inventory levels were a result of steelmakers stockpiling graphite electrodes to avoid the shortages seen during 2018 and 2019. However, declines in steel demand have turned what were merely high inventory levels meant to ensure safety of supply into significantly excessive inventory levels. Even before COVID-19, Showa Denko had already guided to lower graphite electrode volume and profitability as a result of high inventory levels.

- Additionally, prices of needle coke (the key input used to make graphite electrodes) could see upward pressure de-coupled from factors affecting graphite electrode prices as a result of the factors outlined below. I would note that these factors are secondary to the impact of collapsing steel demand and high levels of graphite electrode inventory outlined above and would represent sources of additional downside to my estimates for graphite electrode-needle coke spreads (the key determinant of profitability for graphite electrode producers such as Showa Denko).

-

Lithium ion battery demand grows as a proportion of total needle coke demand as electric vehicle production grows faster (or shrinks less) than demand for steel (as has been the case in recent years).

-

Less needle coke being produced as gasoline refiners (who produce petroleum needle coke as a byproduct of the gasoline refining process) curtail needle coke production in tandem with decreases in gasoline production as a result of significantly reduced demand for gasoline (less miles driven as people quarantine, etc.). Our channel checks indicate that Phillips is already limiting needle coke production, though this may turn out to simply match decreases in steel/graphite electrode demand.

- While there is no widely-accepted graphite electrode reference price and the market can be rather opaque, based on our industry checks, we believe that the spread between graphite electrode and needle coke prices (the primarily determinant of graphite electrode producers’ profitability) has gone from ~$8,000/tn in 2019 to ~$3,000/tn currently. GrafTech, which is vertically-integrated, disclosed in its 2Q20 earnings release that its average price on spot sales in the second quarter was $5,500/tn, and that it expects spot prices to further weaken in 3Q20. Our checks suggest that spot needle coke prices are currently around ~$2,500/tn (note: the ratio between the amount of needle coke needed to produce a given amount of graphite electrodes is 1:1). This collapse in GE-needle coke spreads alone represents a ~¥100+bn y/y hit to Showa Denko’s operating earnings.

- While the outlook for the graphite electrode business is particularly bleak, Showa Denko and Hitachi Chemical’s other business lines primarily serve various industrial end markets that should also see considerable demand destruction as a result of the coronavirus and the accompanying economic slowdown throughout the remainder of 2020.

- This significant decline in operating profitability is occurring just as the company levered itself up significantly to purchase a mediocre asset, a toxic combination with significant negative implications for the equity.

- Based on our estimates, the pro forma entity will burn cash in 2020, which could force the company to suspend their dividend (the company currently trades at a 5.5% dividend yield, which may be supporting the stock despite its challenged outlook and leverage profile). The company announced that they wouldn’t pay out a 1H dividend in the 2Q20 pre-announcement, but the year-end dividend is still undecided.

Valuation

- Base case assumptions:

-

Graphite Electrode – Needle Coke Spread: Assume a normalized spread of $4,500/tn. Compares to ~$8,000/tn spread in 2019 and ~$3,000/tn currently.

-

Merger Synergies: Assume no synergies. Given the limited overlap between the two businesses and the unconvincing rationale for synergies cited in the merger deck are highly suspect, we believe that Showa Denko will be able to realize very limited synergies as a result of the merger. Moreover, even the legitimate synergies that do exist would presumably take several years to materialize.

-

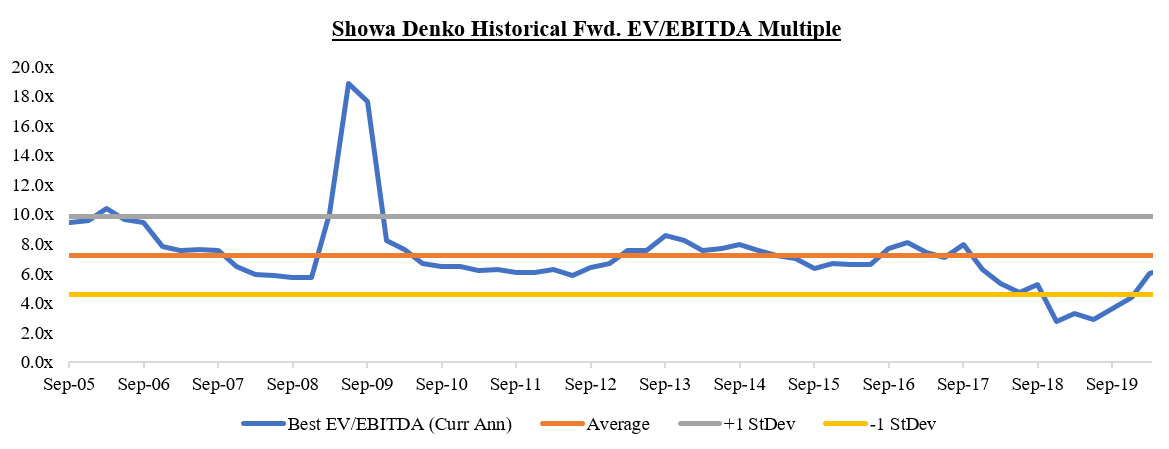

Multiple: 10x pro forma EBITDA. Represents approximately one standard deviation above Showa Denko’s long-term average standalone multiple (average = 7.2x; +1 StDev = 9.8x) and a considerable premium to Hitachi Chemical’s 5.4x average EV/EBITDA multiple. Generously assumes that the market is willing to capitalize earnings at a significantly above-average multiple relative to Showa Denko and Hitachi Chemical’s blended average historical multiples.

- Near-term downside should be limited as the pro forma entity currently trades at 6.1x – in-line with Showa Denko and Hitachi Chemical’s blended average multiple – on a 2019 EBITDA figure that reflects peak graphite electrode segment profitability.

- Given that the company is significantly over-levered post the Hitachi Chemical deal, valuation is a bit tricky to get a fix on. Nonetheless, we believe that there’s significant downside based on conservative assumptions.

- We arrive at a target of ¥1,100, representing ~46% downside.

Risks

-

The market looks past 2020/2021 numbers and the impact of the coronavirus

-

Mitigant: Even if the market were to look through the impact of the coronavirus and value the business based on historical profitability, the business trades at 6.1x pro forma trailing EBITDA, in-line with the Showa Denko (7.2x) and Hitachi Chemical’s (5.4x) blended historical average multiple. As such, the only scenario in which there is material downside over the next year is one in which investors are willing to capitalize historical profitability at an above-average multiple at a time when the company’s operating environment is one of the worst in recent memory and the company has significantly more leverage than has historically been the case.

-

While headline leverage on pro forma 2020 numbers would suggest significant leverage issues and possible risk of an impairment event for the equity, this is mitigated to a degree by the favorable structure of the company’s debt (long-dated maturity profile; some debt is ring-fenced at a separate SPC that will take ownership of Hitachi Chemical).

-

Mitigant: High leverage and declining operating earnings will nonetheless manifest in collapsing 2020 net income and levered FCF figures and may necessitate a dividend cut/suspension (stock is likely supported in part by its current 5.5% dividend yield).

Appendix 1: Showa Denko and Hitachi Chemical Historical Valuation Multiples

Appendix 2: Graphite Electrode Market Overview

Below is a brief overview of the graphite electrode market and its recent history. We would refer readers to past VIC write-ups on GrafTech for more detail on the industry.

Graphite Electrodes Overview

-

Graphite electrodes are used by Electric Arc Furnace (EAF) steel producers. As EAF steel producers comprise the overwhelming majority of demand for graphite electrodes, graphite electrode producers’ fortunes are generally tied to those of the steel industry.

-

EAF is one of the two primary methods of steel production in addition to blast furnace-based production. The two methods of steel production can be contrasted as follows:

-

Blast Furnace: Blast furnace steelmaking uses a combination of raw materials (iron ore and met coal) and steel scrap (usually <30%) to produce steel. Blast furnace is generally more capital-intensive than EAF production and is considered less environmentally-friendly. This is the primary means of producing steel in China and certain other developing countries.

-

EAF: EAF steelmaking doesn’t involve iron-making and uses existing scrap steel in order to produce new steel. EAF production is considered to be more environmentally friendly and has lower capital costs, but also (depending on the commodity price environment for scrap steel vs. iron ore and met coal) generally entails higher variable costs. Today, EAF represents ~65% of crude steel production in the United States vs. ~12% in China, though the latter is seeking to increase their share of EAF steel production.

-

Electrode production outside of China (including at Showa Denko) is primarily focused on ultra-high power (UHP) electrodes for EAF steel producers, while the majority of Chinese production today is focused on the production of smaller-diameter ladle electrodes used by blast furnace steelmakers. Per our research, while demand and production are somewhat fungible between UHP graphite electrodes and ladle electrodes, it’s generally best to view these as two distinct markets with independent supply/demand dynamics.

-

Graphite electrodes (and UHP graphite electrodes in particular) are critical to operating an EAF steel mill and cannot be substituted

-

The cost of electrodes represents a relatively small part of steelmakers’ cost structure; constituting ~1%-2% of total costs

-

The graphite electrode industry is relatively concentrated, particularly outside of China

Needle Coke Overview

-

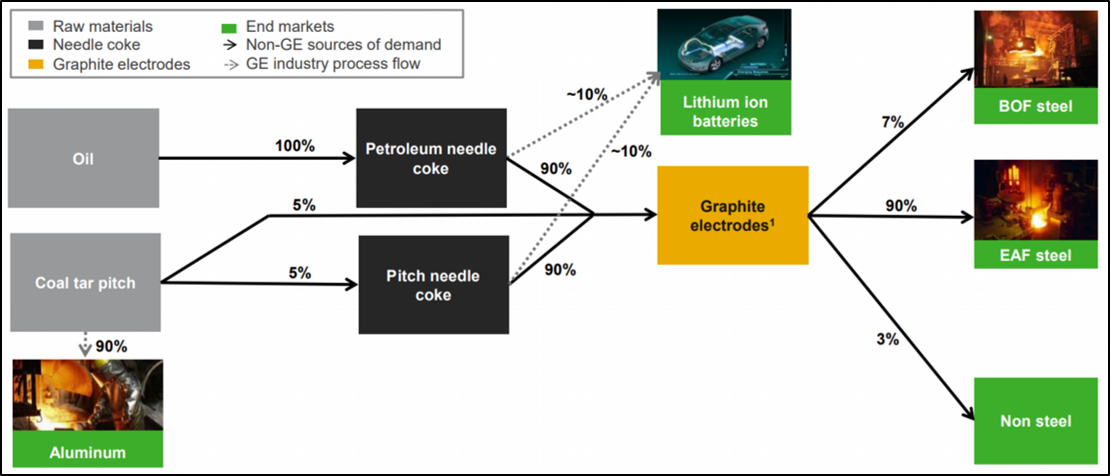

Needle coke is the primary raw material used in the production of graphite electrodes and represents one of the largest components of graphite electrode producers’ cost structures

-

Needle coke comes in two varieties:

-

Petroleum Needle Coke: Made from decant oil, which is a byproduct of the gasoline refining process. It generally takes ~2-3 months to produce petroleum needle coke from decant oil. Graphite electrodes made with needle coke is generally considered to be of higher quality (as it has fewer impurities and has a structure that makes it more resilient to fracturing) and is the primary type of needle coke used by producers of UHP graphite electrodes such as Showa Denko (though Showa Denko and the other Japanese producers do use pitch coke to a very limited extent).

-

Pitch Needle Coke: Made from coal tar pitch, a byproduct of coking met coal used in blast furnace steelmaking. This is primarily used by lower-quality graphite electrode manufacturers located in Asia (primarily China).

-

Building new needle coke capacity is highly expensive, requires considerable technological know-how, and is a long process (takes 5+ years). As a result, there’s no meaningful needle coke capacity being added outside of China.

-

Production of petroleum needle coke is highly concentrated, with just 4 producers accounting for essentially the entirety of global supply outside of China

-

Phillips: Produces petroleum coke as a byproduct of operating its refinery business.

-

Seadrift: Owned by GrafTech (a competing UHP graphite electrode manufacturer whose ownership of Seadrift underpins its vertically-integrated strategy).

-

Petrocokes Japan

-

JX Nippon Oil & Energy

-

While graphite electrodes have historically accounted for the essentially the entirety of demand for petroleum needle coke, in recent years lithium ion batteries for electric vehicles have emerged as a significant secondary source of needle coke demand outside of graphite electrodes and now account for ~10% of total demand. Given that electric vehicle production is growing much faster than demand for steel/graphite electrodes, there should be upward pressure on needle coke prices independent of trends affecting graphite electrode producers.

Evolution of Historical Graphite Electrode Prices and Needle Coke Prices

-

Below are Showa Denko’s historical realized graphite electrode and needle coke prices (in USD)

-

In 2018 and continuing into 2019, graphite electrode prices and spreads rose sharply. This was a result of multiple factors:

-

Shutdown of Chinese graphite electrode and needle coke capacity: Beginning in 2017, the Chinese government started to aggressively crack down on pollution in China. As part of this, the government shut down graphite electrode and needle coke plants representing ~1/3 of the country’s capacity. Before these reforms, Chinese graphite electrode producers exported smaller diameter ladle graphite electrodes throughout the world. After a significant portion of this production was shut down, the price of ladle electrodes spiked as China was no longer exporting significant quantities of ladle electrodes. To take advantage of this, UHP graphite electrode producers repurposed some their capacity to produce smaller diameter ladle electrodes, which effectively took away capacity away from UHP electrodes. Note that based on our work, essentially all of this re-purposed capacity has already been re-converted back to UHP capacity.

-

Increase in steel demand: Steel demand began to increase after a period of demand weakness from 2011 to 2015.

-

Shift from blast furnace to EAF steelmaking in China: On top of the increase in overall steel demand, steel production in China shifted from ~9% EAF to ~11%-12% EAF-based by the end of 2018, which was also largely in response to the same environmental mandate that led to the shuttering of significant graphite electrode and needle coke capacity in the country.

-

Low graphite electrode and needle coke inventories going into the increase in demand: Prior to the recovery in steel demand and the shutdown of Chinese graphite electrode capacity, there was little graphite electrode and needle coke inventory in the system, exacerbating the impact of the sudden shortage. Since graphite electrodes are essential for steelmakers to effectively operate their plants yet a relatively small part of their cost structure, steelmakers were willing to significantly pay up for graphite electrodes in order to ensure their plants continued to operate.

I and/or others I advise hold a material investment in the issuer's securities.

Catalyst

Dividend cut; sell-side analysts update targets/models; continued weakness/further decline in graphite electrode market.

| show sort by |