| 2020 | 2021 | ||||||

| Price: | 7.45 | EPS | NA | NA | |||

| Shares Out. (in M): | 32 | P/E | NA | NA | |||

| Market Cap (in $M): | 241 | P/FCF | NA | NA | |||

| Net Debt (in $M): | -36 | EBIT | 0 | 0 | |||

| TEV (in $M): | 205 | TEV/EBIT | NA | NA | |||

Sign up for free guest access to view investment idea with a 45 days delay.

Description

eGain (EGAN) is an opportunity to own an underfollowed, high quality SaaS software company at ~3x recurring revenue. We see a path to 2x-3x upside over 5 years with minimal downside at these levels.

Investment Thesis

· Attractive valuation at ~3x recurring revenue (90%+ of the business is recurring)

· Stable recurring revenue has grown at a ~15% CAGR over the past decade while total revenue growth has been masked by the SaaS transition

· Recurring revenue is sticky, which is a function of high switching costs

· The current base of recurring revenue protects your downside given that the company has a 93%+ gross retention rate and 100%+ net-dollar retention rate; a run-off of the current revenue stream would generate ~$6.20/share of cash

· Our channel checks suggests that superior functionality, feature-set, and pricing has allowed it to compete favorably with players such as Salesforce, LivePerson, Moxie, etc.

· Large addressable market supports long runway for growth

Business Overview

eGain is a provider of customer engagement software. Some of the largest companies in the world—such as Comcast and Vodafone—use their software in their call centers. An example use of the software is when you call into the call center of Comcast. The eGain Knowledge Base allows the call center agent to find the right answer from your query within seconds or minutes. This knowledge base gets smarter overtime with each interaction, which creates a huge switching cost as Comcast would have to re-write the knowledge articles for a new software provider. This is all integrated with the virtual assistant, social, chat, and analytics features. When you use the chat feature on the website, information is pulled from the knowledge base to guide you to the right answer. eGain customers can also pull information from other channels—email, SMS, Facebook, etc. The information from these channels is pulled into the knowledge base, which creates a more efficient and quicker interaction for the call center agent, contributing to better customer service levels and happier end-customers.

The software is used by large enterprises in the financial services, telecommunications, retail, government, healthcare, and utilities sectors. Financial services is a 30%+ end-market. The software is currently sold through a direct sales force and partners. eGain’s largest partner, Cisco, represents roughly ~20% of revenues currently. The eGain functionality is sold in conjunction with Cisco’s contact center solutions, and in other instances, sold as an upsell. Because eGain’s customers are comprised of large, well-capitalized enterprises, we believe eGain will be able to withstand any prolonged, deep downturn in the economy.

eGain has spent much of the last 4-5 years transitioning to the cloud/SaaS model, which has clouded top-line revenue growth. As you can see, total revenues over the past 5 years has stagnated around ~$70M, while subscription/recurring revenues has grown from ~$40M to $60M+ today. By the end of FY 2020 (June end), 90%+ of the business will be recurring, with ~87% of recurring revenues being SaaS.

Our channel checks revealed that superior functionality, feature-set, and pricing were the primary factors customers chose the eGain knowledge management solution. Features such as the natural language processing approach and guided help were much more sophisticated and extensive compared to competitors such as Salesforce, Moxie, and Oracle. The eGain solution was more flexible and agile in terms of the desired implementation for the customer (for example, eGain could maneuver the content more seamlessly in the implementation). The eGain platform also had an integrated email and chat platform which the competitors lacked. Other software vendors, even Salesforce, in the space are still incredibly manual. Even with superior functionality, our checks revealed that eGain was priced at a ~30% discount compared to its comparable competitors.

Our channel checks are also confirmed very high switching costs: changing out the eGain platform would be an extensive, lengthy process. It would take at least 6-8 months to switch to another platform because one would have to re-write the knowledge articles for the new platform. Because one cannot convert the underlying, historic data of the contact center retained by the eGain solution, one would have to start a whole new data mine for the new solution. In other implementations, eGain was integrated with other business applications within the organization, which required huge amounts of work and investment. Overall, once customers had a robust, working knowledge management platform with eGain, they stuck with them for a very long time. Not surprisingly, the company boasts a steady 93%+ gross retention rate and a 100%+ net dollar-retention rate resulting from upsell/cross-sell of additional features/functionality.

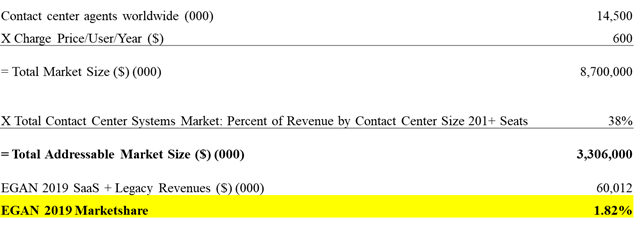

Market Sizing

We estimate that the total addressable market for eGain is roughly ~$3.3B and eGain represents a tiny portion of that space. We believe that eGain’s superior cloud knowledge management offering should allow it to gain market share for the next 5+ years

Valuation

Price $7.45

Shares (000) 32,335

Mkt Cap (000) 240,896

Debt (000) 3,959

Cash (000) 40,321

EV (000) 204,534

Despite similar organic recurring revenue growth rates, EGAN trades a discount to its larger public peers.

|

Enterprise Value (EV) ($M) |

EV/Forward Recurring Revenue |

Recurring Revenue Growth Rate |

|

|

Liveperson (LPSN) |

1432 |

4.2x |

18% |

|

Verint Systems (VRNT) |

3,064 |

4.2x |

9% |

|

Average |

|

4.2x |

14% |

|

eGain (EGAN) |

205 |

3.2x |

15% |

In a conservative theoretical run-off scenario, we estimate the shares have minimal downside. The current investments in S&M and R&D are predominantly for growth and new logos—the company can be run at 45%+ EBITDA margins if management wanted to solely run this for cash flows, retention, and minimal growth. Using a 10% discount rate (conservative for a steady recurring revenue stream in our view), we can discount the future cash flows and obtain ~$6.20/share of run-off value.

In our base-case, we have SaaS growing ~15% CAGR and legacy maintenance -35% for the next 5 years. We exit 2025 close to $110M of recurring revenues and assume a conservative 4x recurring revenue exit multiple. EBITDA margins average around 5%. This yields a $15/share outcome, or an 18% unlevered IRR over the next 5 years.

In our upside-case, we have SaaS growing ~20% CAGR and legacy maintenance -35% for the next 5 years. We exit 2025 close to $126M of recurring revenues and assume a 5x recurring revenue exit multiple. EBITDA margins average around 8%. This yields a $21/share outcome, or a 27% unlevered IRR over the next 5 years.

Our more recent channel checks as of late March 2020 suggests that the eGain software is being more utilized than it has ever been due to higher call volumes to call centers, more email/social media traffic, and the increasingly remote workforce. We believe these trends bode well for eGain and its growth through the current economic climate.

We believe EGAN would have multiple buyers spanning from middle-market PE firms (who would better balance growth and profitability) to strategic buyers such as Salesforce or Oracle (who would want their unique technology). In this case, we believe the company would obtain at least 5.5x recurring revenues, or $12/share today, or close to a ~60% upside today.

Management/Board

The company is run by a very technically competent CEO and founder who is clearly committed and aligned (with 32% ownership); we believe he has improved on the Sales & Marketing front in recent years as the sales team has begun to mature and execute. His only way out of the position is through the sale of the company.

Risks

· Pricing pressure as result of existing competitors bringing price points down

· If Cisco acquires a knowledge management competitor, then the Cisco relationship would be at risk

Conclusion

Given the downside protection from the balance sheet and sticky recurring revenue model, EGAN is ultimately a call option on an acquisition or continued growth in the business. In today’s world, it is important enterprises have a more knowledgeable, capable call/contact center. We believe eGain—due to its unique technology and favorable pricing—is well positioned to capitalize on this trend.

I and/or others I advise do not hold a material investment in the issuer's securities.

Catalyst

Investor exposure

Continued growth and marketshare

Acquisition

| show sort by |