| 2019 | 2020 | ||||||

| Price: | 21.70 | EPS | 1.728 | 0 | |||

| Shares Out. (in M): | 20 | P/E | 12.6 | 0 | |||

| Market Cap (in $M): | 554 | P/FCF | 12.7 | 0 | |||

| Net Debt (in $M): | 68 | EBIT | 55 | 0 | |||

| TEV (in $M): | 622 | TEV/EBIT | 11.3 | 0 | |||

Sign up for free guest access to view investment idea with a 45 days delay.

Description

Trading at a TTM 7.4% unlevered FCF yield compared to a GBP discount rate 1%+ below USD, XP Power is a good business, consistently earning 20+% returns on equity on an unleveraged basis. Serving a diverse portfolio of capital goods equipment manufacturers, geopolitical and macroeconomic nervousness has cut the stock price almost in half over the last 9 months. But results so far have been resilient, despite the Q4 18 slowdown. And management has been here before: possessing a two decade track record of constantly evolving their business towards high value-added products and relationships with their customers.

Business Quality

XP Power designs and manufactures power controllers, the essential hardware component in every piece of electrical equipment that converts power from the electricity grid into the right form for equipment to function.1

At first that might sound like a pretty terrible business, based on personal experience of the commodity products that charge our consumer devices. But these are not the cheap power converters that some motels now give away for free.2

Instead XP custom designs each model to fit the exact needs of each commercial customer at the design stage of their own capital equipment. This could be a medical device used during surgery, when reliability is crucial; or a commercial oven where incorporating a cutting edge power converter at the design stage reduces the equipment’s sales price and ongoing running cost. 2018 sales were split:

-

Industrial (43%, the most fragmented of its segments, with only a few customers featuring in its Top 30)

-

Semiconductor manufacturing (24%, see risks)

-

Healthcare (22%)

-

Technology (11%)

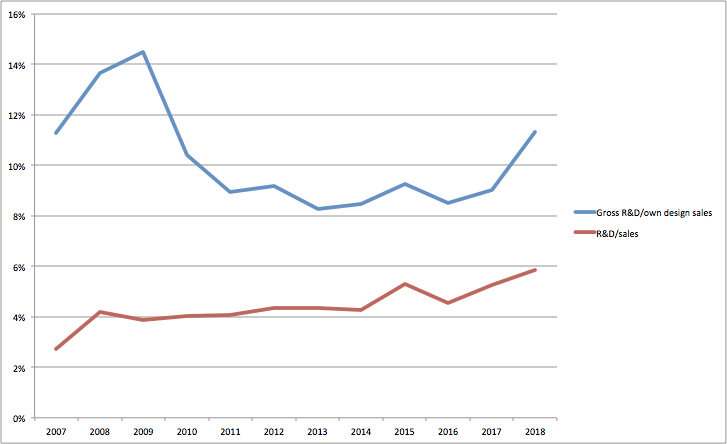

The commitment required for each potential design win is significant, both in time (revenue might take two years) and R&D expense (some of which is capitalized, included in the gross number below):

A design win will typically be manufactured and sold by XP for the life of that particular model of capital equipment.

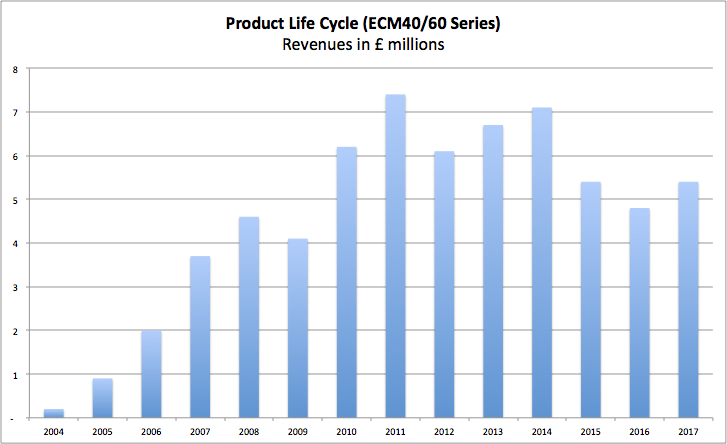

Once designed into a programme, XP Power has a revenue annuity over the life cycle of the customer's product which is typically 5 to 7 years depending on the industry sector.3

Some models have even longer lived life cycles:

Source: http://www.xppowerplc.com/archives/financial/2017-results-presentation.pdf

Margins (45.0%-49.6% Gross Margins 2009-18 and around 20% Operating Margins) are attractive because the typical purchase does not emphasize price comparison. Custom-designed for a specific model of capital equipment, sold face to face, purchased under time pressure, after a lengthy qualification period, and assembled from standardized but state of the art components manufactured at low cost in China and Vietnam, the cost base is structurally lean, while the sales price reflects several opportunities for a good supplier to create genuine value for its customers.

Our sales process is generally a technical sale, between XP Power sales engineer and customer design engineer. Our customers are typically experts in their field, whether it is a drug delivery device, a piece of complex factory control machinery or a high-end communications device operating in a harsh environment. They will approach a company such as ours to recommend and assist them to design a power converter into their end system to allow it to function.

Generally, with larger customers it is not possible to engage on a specific opportunity until we are on an approved or preferred vendor list. This will involve qualification by the customer’s technical, quality and purchasing teams and may often involve a physical audit of our quality systems and a factory audit.

1 IDENTIFICATION

A new design programme is identified at a customer where we are an approved or preferred vendor. This is typically quite late in the customer’s development cycle as they will not usually know the total power requirement of their system until they have a working prototype.

2 QUOTATION

An XP Power sales person will work with the customer to understand the requirements including the power requirements at different voltages, communication required between the power converter and end system, any specific safety agency requirements and the physical dimensions. XP Power will then advocate a solution and provide a quotation to the customer. This solution could be a modification of one of our standard products.

3 SAMPLE

One or more samples are provided to the customer for them to evaluate in their system.

This is a critical stage of the sale and we often find that the first company providing a sample that works in the equipment will win the design slot. Speed is therefore critical. Our power systems engineers will often work closely with the customer at this stage to assist them with any issues they might experience such as dealing with electrical noise.

4 APPROVAL

The power converter is approved for use in the customer system following the customer’s technical evaluation and external safety agency approval. This is generally the longest part of the sales cycle as the technical and safety evaluation are very time consuming for the customer. XP Power will often add value by providing technical assistance during this stage and it is not unusual for us to have a technical power systems engineer working directly with the customer.

5 PRODUCTION

The customer commences production of their product and XP Power’s revenue stream starts. This is typically around seven years depending on the application and end market.4

All of this adds up to a good business, as evidenced by its 10 year ROE ranging 21.9%-42.5%, ROA 12.3%-19.6%, achieved with very low leverage. Pre-tax returns on (working capital plus net PP&E) have exceeded 45% over the period, which includes the 2009 recession.

XP Power currently holds 12% market share each of its North American and European markets. It has held at least 6% and 8% respectively of these markets for the past 15 years. It has a much lower 1.6% market share in Asia due to regulations requiring export and re-import of any Chinese sales, meaning only the highest value-added products win there.

But is it predictable? The competitive advantages that have delivered such results have been hard won and have evolved over time. Therefore this is not a business that could be effortlessly run by a ham sandwich.

Management Track Record

When it listed in 2000 on the London Stock Exchange, it was merely a distributor of power converters, facing a tough capital spending future for its main telecommunications customers during the tech bust. Management have done a superb strategic job over the last couple of decade. They consistently skate to where the puck is going, rather than where it has been.

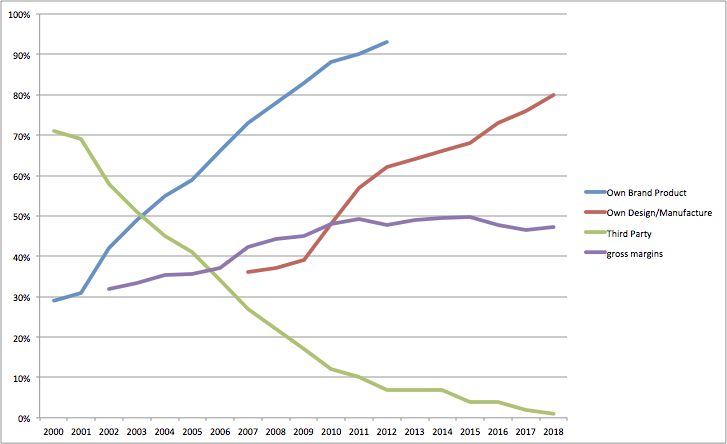

Big picture they have transformed the business since 2000, when 71% of sales was distributing third party products plus a bit of own brand product which was mostly just labelled, then increasingly selling own branded product, and then the full migration to own design and own manufactured product that now accounts for 80% of sales.

2002: Increase contribution of high margin own designed products

New product development is vital to the long-term success of our business. Fragmented requirements of customers in the mid-tier and the lack of resource devoted to suitable product development for the mid-tier amongst the top-tier players has given us an advantage in this arena.5

2005: Shanghai Manufacturing JV: followed customers to China.

We continue to see a trend, particularly amongst our larger customers, where the design work is performed in Europe or North America but the customers’ product is transferred to Asia for manufacture. Our Shanghai operation now provides both local technical and logistical support to our customers who chose to manufacture in China.6

2006: Re-domiciled to Asia from UK.

Our suppler base is in Asia. Our customers are moving there. Our competitors manufacture there. More competitive corporate tax cost. Higher calibre and lower cost people.7

2007: Bought out the JV, in response to customer demands for full control over supply chain.

the manufacturing joint venture has enabled us to target a whole new group of customers who will only do business directly with a manufacturer.8

2008: Vietnam Manufacturing. Purchased land for two factories, with the second completed when capacity was required in 2018.

2008: Capacity expansion in Vietnam...mitigates continued rise in China costs and spreads geopolitical risk.9

2019: Our product is affected by the so-called Section 301 tariffs that they have imposed in the USA. The US has imposed a 10% tariff on electronic products produced in China, including power supplies. We are in a fortunate position actually because we also have a factory in Vietnam, and we have just completed a new factory there. So where relevant, we have been diverting product from China to Vietnam, to hopefully put us in a better position than some of our competitors who only have the opportunity to manufacture in China.10

2009: Green product innovation. Major commitment to “Lead our industry on environmental issues” improved efficiency (and therefore running costs) of power converters, investing significant in Low Standby power and High Efficiency products. These quickly differentiated XP Power from their competition.

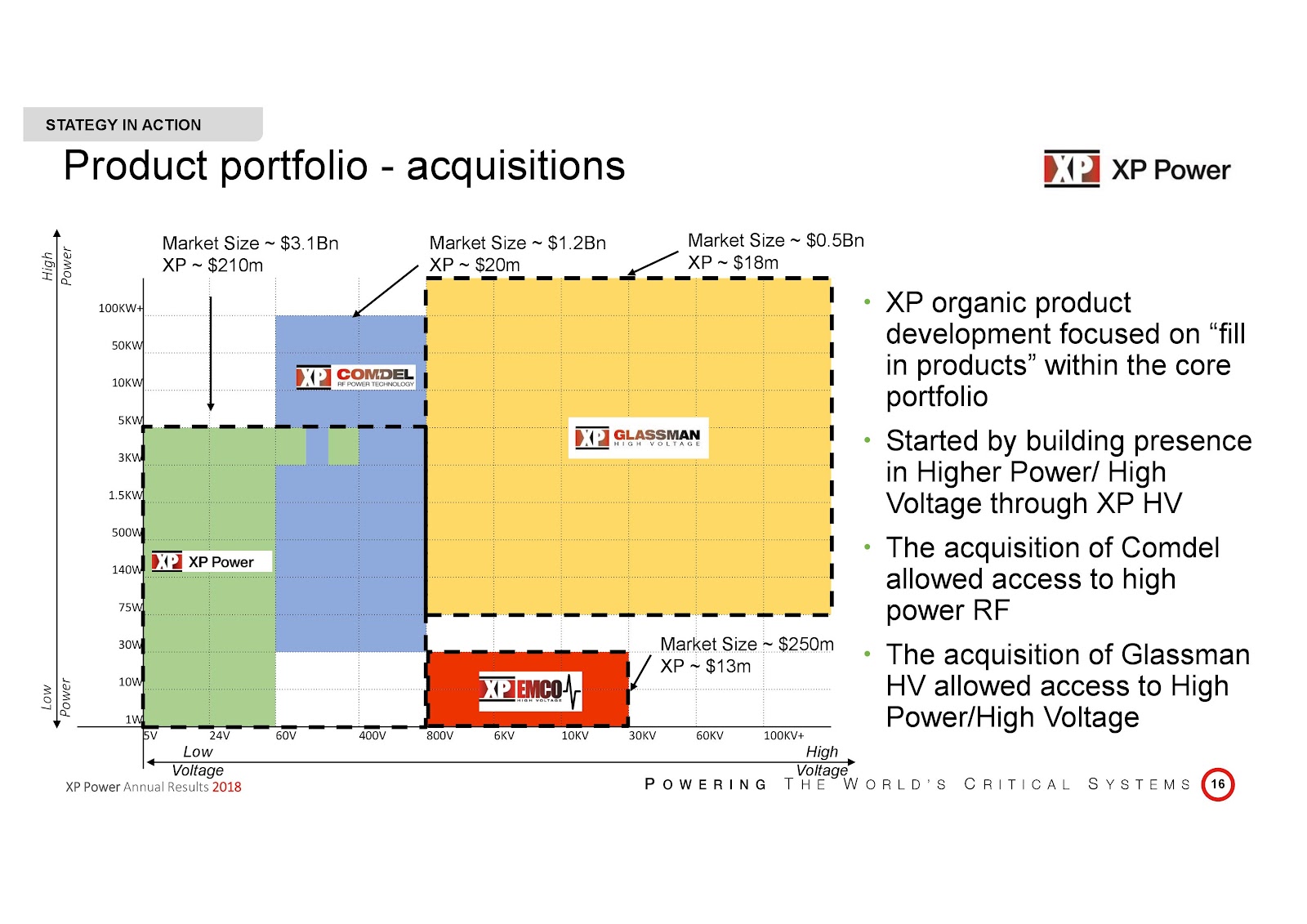

2015-now: Acquisitions. Thoughtfully acquire companies to move the company from low voltage, low power to high voltage, high power products where differentiation should be more durable to Asian competition. Strategically sound. Well executed (purchased New Jersey-based Glassman from the estate of Sanford Glassman, Glassman’s founder and major shareholder, within 2 months of his passing, aged 95). Well disclosed: they give more disclosures than required for shareholders to measure the performance of their acquisitions.

Source: http://www.xppowerplc.com/archives/financial/2018-results-presentation.pdf

This kind of evolution has been crucial. Without it, I suspect the business would no longer exist. The constant exposure to relentless Asian competition has made management keenly aware that any advantage that they might currently possess is probably fleeting. I find them good at transparently informing investors of future targets, and measuring past performance. This is not common.

Key Management

-

James Peters (60) Non-Executive Chairman, 8% shareholder. Founded XP in 1988, having worked as a sales engineer at the then dominant power converter company Lambda (subsequently bought by TDK).

-

Duncan Penny (56) CEO since 2003.

-

Mike Laver (56) President Global Sales.

-

Andy Sng (48) GM Asia.

-

Larry Tracey (71) the original Chairman pre-float, played a significant role in the development of the company until cashing out at £16 per share in 2014.

Compensation is restrained. Equity participation has been encouraged, but not at the cost of an expanding share count.

Management is long standing and has demonstrated an ability to adapt to changing macro-economic and competitive environments. Mainly this seems to be the result of getting as close to their customers as they can:

Having evolved from a sales and marketing background as a specialist distributor of power conversion products, then moving into design and then later into manufacturing, we have a unique understanding of our customers and the market compared to much of our competition. We are now expanding our engineering solutions group to further enhance the value we can deliver to our key customers.

We have carved out a leading position in our industry. An up-to-date, high efficiency product offering, delivered to our customers by the largest and most technically competent sales engineering team in the industry, backed up by highly-skilled power systems engineers, combined with the safety and reliability benefits of world-class manufacturing provide a compelling value proposition to our customers.

Our model is to sell directly to our key customers where we can add genuine value, offering excellent service and support combined with class-leading products.11

Risks

-

Technology. Fat technology tails I think are mainly on the left, not right, of expected outcomes for this business. Even industry insiders could be surprised at developments that revolutionize this business.

-

Stock volatility. Not just the boilerplate language you read in 10-k’s. The fact that in 2009 this traded at 2.5x TTM P/E, or 1.4x forward (actual) P/E. All the company’s products are designed into capital equipment. When investors are depressed about the capital equipment cycle, this stock can get crushed.

-

Capital equipment cyclicality. In particular semiconductor manufacturing represented 24.3% of 2018 sales; cycle concerns have obviously increased in recent weeks. This time last year management already called out the semi risk, when it was a smaller proportion of sales.

While we cannot be immune from any economic shocks or cyclicality in our end markets, and in particularly the semiconductor manufacturing equipment sector which represented 17% of our business in 2017, we are optimistic regarding the outlook for 2018.12

Appendix: Case Studies

Industrial Case Study: Commercial Kitchen Equipment13

The Opportunity

-

Customer supplies equipment to the food industry

-

Historically using old fashioned linear power converters

-

Harsh environment with elevated temperatures and peak loads

-

Not familiar working with switch mode products so we sent an engineer to work alongside their design team

The Benefits to the Customer

-

Universal input allowed them to cut down variants from 82 to 20

-

Higher reliability

-

Standard product reduced engineering resource

-

Smaller footprint

-

Saved the customer significant amounts of money

XP revenue

-

$1 million plus revenue program per annum

Healthcare Case Study: Multi-Parameter Patient Monitor14

XP Power received a challenging design brief from a large international medical equipment manufacturer for a high performance power converter for use in a multi-parameter patient monitor. The monitor was compact, containing no cooling fans, and had a high internal ambient temperature. Space for the power converter was limited and a very small footprint was required so that the electronics would fit tightly into the equipment.

In common with all medical applications, reliability and equipment lifespan were critical to the customer. Since higher temperatures within equipment shorten the expected lifetimes of some of the critical electronic components, it was extremely important to find ways to minimise the heat produced in operation and remove as much heat as possible from the equipment.

XP Power’s solution was to specify its ECS100 converter – an innovative product with only

a 2” × 4” footprint and capable of producing 80 Watts of power without the need for fan cooling. The ECS100 delivers high end performance in a small package but at a very competitive price.

In order to meet the customer’s lifetime specification XP Power needed to ensure that the electrolytic capacitors would run as cool as possible. A detailed design review with the customer had identified the use of a heat sink on the back of the monitor to provide cooling for other electronics, and it was therefore proposed that this also be utilised to provide additional cooling for the power converter.

To utilise this cooling method it was vital to determine an effective way of conducting the heat from the critical ECS100 components

to the outside world. Drawing on experience gained in the development of its ECC100 product, a conduction cooled converter utilising a baseplate to conduct heat away, XP Power proposed an innovative design. The ECC100 was designed specifically for harsh environments without fans or air flow for cooling and made use of a special thermal material which, when placed around key components and compressed effectively, dissipated unwanted heat by conduction.

The first proposal was for an ECS100, fixed to a custom baseplate and surrounded by the special thermal material, to be bolted into the monitor’s heat sink. Although technically a good solution, two potential issues were identified. First, the heat generated by the power converter could raise the temperature of the heat sink, which would affect other components bolted to it, and second, the cost of all the extra metalwork would drive up the cost of the end equipment. The solution was to divide the heat sink in half and bolt the power supply directly to one side, giving it a dedicated conduction path.

In a collaborative development effort, the customer designed a unique aluminium heat sink based around the shape of the monitor and XP Power developed the mechanical interface to secure the ECS100 power converter to the heat sink.

Today the whole power converter and heat sink assembly is manufactured in XP Power’s factory in Kunshan, China. Since XP Power had not previously used cast aluminium heat sinks in its products, the customer introduced us to one of their existing approved suppliers in China to fabricate the heat sink and took responsibility for getting the tooling produced and the negotiations with the vendor.

XP Power project managed the entire process to ensure that parts arrived on time in the factory, enabling initial production batches to be produced. The whole assembly was also safety approved to medical standard IEC60601-1. The monitor went into initial production during the second half of 2012 and will enter full production in 2013.

Successful completion of the project provides an excellent example of how XP Power’s engineering capabilities and flexibility delivered genuine value to the customer.

Critical success factors

• Availability of a highly efficient base power converter with a small foot print

• Engineering resource that could work directly with the customer’s design team

• Flexibility to modify the design to meet the customer’s stringent life time requirements

• Flexible in-house manufacturing capability

• Ability to approve the whole power converter assembly to the latest medical standards

• Low cost Asian manufacturing

• Collaborative relationship with the customer throughout

Technology Case Study: Smart Meter15

Customer is a global leader in smart grid technology.

Customer’s application provides wireless communication capability for real time data management to utility companies and to the end users. They were releasing a firmware update to their latest residential smart meter.

The new firmware required increased power. Needed for existing product field retrofits and new orders.

Technical challenges:

-

Unique form factor with severe space restrictions

-

Unusually low profile

-

Power requirements in a rugged environment (full power at temperatures from -40C to +85C)

-

Communication feedback to report remote power supply health status

-

Capability to withstand AC surges lightning surge protection features

Result:

-

We designed and delivered first article units in just seven weeks.

-

The pilot product units are already in the field and we expect the program to go into production in the first Q1 2018.

-

The design resulted in a five year contract to support field upgrades and fulfil new orders.

Sources

- Annual Results for the year ended 31 December 2018

- https://www.wsj.com/articles/SB10001424052748704532204575398002385885596 The Sands in San Luis Obispo goes a step further: It keeps a basket of 12 phone chargers in the breakfast room of the 70-room hotel with a sign that says, "Take one if you need one." Aug. 7, 2010 WSJ.

- Annual Results for the year ended 31 December 2018

- Annual Report 2017, p.12

- Annual Report 2002

- Annual Report 2005

- http://www.xppowerplc.com/archives/financial/2006-results-presentation.pdf

- Annual Report 2007

- http://www.xppowerplc.com/archives/financial/2010-results-presentation.pdf

- CEO Duncan Penny speaking on 2018 Annual results video

- Annual Report 2017, p.12

- Annual Report 2017, p.23

- http://www.xppowerplc.com/archives/financial/2013-results-presentation.pdf

- Annual Report 2012, p.15

- http://www.xppowerplc.com/archives/financial/2016-results-presentation.pdf

I and/or others I advise hold a material investment in the issuer's securities.

Catalyst

| show sort by |