| 2019 | 2020 | ||||||

| Price: | 52.30 | EPS | 0 | 0 | |||

| Shares Out. (in M): | 112 | P/E | 0 | 0 | |||

| Market Cap (in $M): | 5,860 | P/FCF | 0 | 0 | |||

| Net Debt (in $M): | 5,500 | EBIT | 0 | 0 | |||

| TEV (in $M): | 11,360 | TEV/EBIT | 0 | 0 | |||

Sign up for free guest access to view investment idea with a 45 days delay.

- winner

- XPO LOGISTICS INC XPO S 08/12/2021

- XPO LOGISTICS INC XPO S 04/21/2016

- XPO LOGISTICS INC XPO 10/19/2012

- BETA

- Saia SAIA S 08/01/2022

- RED ROCK RESORTS INC RRR 12/02/2021

- Lindsell Train Investment Trust PLC LTI 09/28/2023

- RADIANT LOGISTICS INC RLGT 11/17/2015

- PACIFIC GAS & ELECTRIC CO PCG 06/29/2020

- UNIVERSAL LOGISTICS HLDGS ULH 09/04/2024

- IES HOLDINGS INC IESC 08/15/2022

Description

We currently see a relatively timely opportunity to buy shares of XPO Logistics. The stock is off by ~50% from its 2018 highs nine months ago and is now trading at an attractive valuation. The opportunity exists due to a combination of recent company-specific issues paired with the trade-related macro worries and some YoY softness in the transportation sector that have hit company valuations across that space.

XPO is a successful roll-up of a dozen different logistic businesses that took place between 2011 and 2015. A roll-up history always tends to skew people's opinion of a company to the extremes - either it is a great capital allocation story with a long runway or a yet to blow-up run by irresponsible people. XPO is not new to VIC and was already pitched along those theme-lines, once as long in 2012 and then as a short in 2016. We view the generally moodier trading character of roll-ups as a plus due to increased chances to buy low in a confidence crisis and sell high when optimism overshoots.

Recent events, especially the rapid revenue loss of XPOs biggest client Amazon (and a customer bankruptcy that resulted in impairment charges) plus softness in Europe led to more than one guidance revision. That, along with higher than usual c-suite employee turnover opened the door to question the health and strategy of the whole business again. A well polished and timely, but mostly fabricated public short report by Spruce Point helped to increase uncertainty and push the share price down further.

XPO at that time was on the hunt for a big new acquisition, but the share price decline changed capital allocation plans and the company responded with an aggressive share buyback program that reduced the fully diluted share count by ~24% in just a little over four months (35m shares for $1,9b @ ~$53 a share). It was a bold move by Bradley Jacobs, the architect and 18%-owner (20m shares) of the company who by now, is well known for his “boldness”… In addition, the two biggest shareholders who together hold over 34m shares now, eq ~ 30% of the fully diluted shares, added both to their positions alongside those buybacks. The buyback increased the leverage to ~3x net-debt/EBITDA. A level we accept but one where we wouldn’t mind half a turn lower - even just to preserve optionality. However, leaving the rare possibility of insanity aside, it is also a clear indication of the high confidence Jacobs and the large insiders have in the business trajectory and its cash generating ability in a downturn. Here is Jacob's answer to a question around leverage and the buybacks from the last CC:

CC Q1 2019 - Ariel Luis Rosa, BofA Merrill Lynch, Research Division

Great. That's helpful colour. And then on my second question, just wanted to touch on the capital structure a bit and return, I think we talked about earlier, but by my calculation, you guys are now at roughly 3x net debt-to-EBITDA and I think you had previously talked about the target range being somewhere in the 3 to 4x area. So just wanted to see, do you think there's capacity to further lever up and maybe M&A comes back on the table? Or do you see kind of buybacks is continuing to be an attractive opportunity? I think you have roughly $600 million remaining on your authorization. Is that something we should look maybe to continue and maybe the means to continue that is through a little bit further leverage?

CC Q1 2019 - Bradley S. Jacobs, XPO Logistics, Inc. - Chairman & CEO

Well, we could lever up. We certainly could lever up from the point of view of being able to service the debt very, very easily and comfortably even in a downturn because as you know in our business model, during a downturn, we cut back growth CapEx, working capital becomes a source instead of a use. We even turn back - we'll even turn back maintenance CapEx a little bit, and we're going to throw off significantly more free cash flow during a downturn than we do ordinarily, while we're expanding and growing during this part of the cycle.

XPO under Jacobs leadership quickly became a large US & European transportation and logistics company that is active across more than one business line. The company provides a good 60-pages long, always up to date overview and bullish long case. Here is the Link. It certainly makes sense to read through it. I also won’t repeat the intro into all the various segments here again. If one believes in everything the company says, one shouldn’t take too long to hit the buy button. However, the management team is certainly on the promotional side. Generally a tad too promotional for our taste, but we decided to accept it, given that they also tend to deliver a lot. Jacobs has proven himself multiple times already. The assets are quite decent and currently cheap enough to also be a little more forgiving. If one is super principled in that regard, XPO is not the right company. We simply cap the remote risk of being screwed over with a smaller position size.

The bear case out there can be found here:Link In our opinion, the most destructive and therefore important part of Spruce Point’s report - that the company is a failed roll-up built on aggressive debt-funded acquisitions with little cash returns to show for it years later - is fabricated and wrong. XPO has executed well and improved and grown both the top and the bottom line of the acquired businesses.

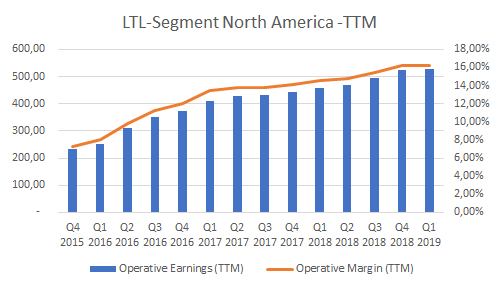

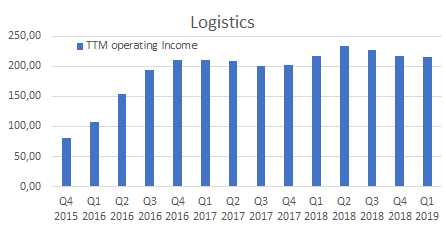

Con-Way, XPOs largest US acquisition is a good example. XPO bought the business for an enterprise value of $3b (EV/EBITDA = 5,9) in 2015. At the time the less than truckload (LTL) segment, the most valuable part of Con-Way did around $300m in EBITDA out of an overall $510m. XPO sold the full truckload (TL) business for $558m to Transforce in 2016 (link), which is, by the way, something Spruce Point conveniently left out. Fast Forward to today and the LTL EBITDA is nearly double that number at $700m. Overall capex for Con-Way prior to the acquisition averaged ~$280m annually. Part of Capex went away with the TL sale. So it is very hard to argue that this ~$2,5b purchase was a bad use of capital. The following graph shows the LTL operating income and margin on a TTM basis.

LTL is a relatively decent business if it is well run, at scale and one enjoys good labour relations. There are barriers to entry and scale benefits given the requirement of many cross-docks/service terminals across the nation in the right locations, local pickup and delivery density and an accompanying large volume of business to reshuffle and distribute loads efficiently. You can’t just buy a truck and start off like in full truckload. Due to those barriers to entry, LTL is fairly concentrated with the 10 largest players accounting for ~80% of the market and only modest annual market share shifts between those participants.

For outside reference, bulls can point to the leader Old Dominion with aspirational mid-teen net-margins, more or less unlevered mid-twenty equity returns, ~10x return from the pre-crisis 06/07 levels till now, and an EV roughly on par with XPO's overall EV, even though XPO's LTL business is less than 10% smaller than Old Dominion's and there is so much more under the XPO umbrella besides LTL. Bears, on the other hand, can point their fingers at YRC or ArcBest, two unionized competitors who are barely breaking even or at best not earning their cost of capital. The next recession will likely bankrupt YRC, still a large player and once the LTL leader with over 25% of the market and twice its current revenue. The unionized players all together still account for ~27-28% of the market and will continue to be market share donors to the more efficient industry participants for the foreseeable future, a trend that has been in place for a long time.

Given XPO’s non-unionized labour force and currently only a remote risk of getting one, we think both YRC and ArcBest are bad comps. Using them for any relative valuation frameworks or comparable operating metrics doesn’t make a lot of sense. They not only have less flexibility to be as efficient due to restrictive teamster contracts, they also carry 500 bps higher employee costs. Old Dominion’s business is a much better proxy for XPO’s LTL future financial potential. We think XPO’s LTL business can continue to improve and close part of the gap to Old Dominion’s operating performance. Old Dominion is a very soundly run company operationally, but at the same time not very technologically sophisticated, which is an area that will continue to become more relevant, no matter if the industry participants like it or not. XPO, on the other hand, not only pushes hard on operational excellence but also embraces new technology. It’s definitely a plus, even if they likely overstate their level of differentiation and technological “leadership” to a degree. Competitors are generally more sleepy. The majority of smaller players are at a disadvantage.

XPO is targeting to get to $1b in LTL EBITDA and a full year operating ratio in the low 80s in the next few years. Besides cost and efficiency initiatives they are filling up their network with more local clients that are more profitable than national accounts. Looking at Old Dominion, the two goals don’t seem to be impossible to achieve. A strong bull case can be built on just that, with the other segments staying course. Here is some recent commentary around the segment from the recent Q1 2019 CC:

CC Q2 2018 - Scott B. Malat, XPO Logistics, Inc. - Chief Strategy Officer

We've come a long way in LTL. We still have the opportunity to improve our operating ratio by several hundred more basis points. Our goal is to reach a full year ratio in the low-80s over the next few years

CC Q3 2018 - Scott B. Malat, XPO Logistics, Inc. - Chief Strategy Officer

We still have plenty of runway to optimize our LTL network. We're working on a number of technology projects that have the potential to add approximately $100 million to operating profit over the next 2 years. For example, we just launched Phase 1 of our new linehaul bypass model. This creates truckloads dedicated to direct freight shipments, instead of having the trucks stop at multiple service centers. So far, this change has shown an approximate 2.4% increase in direct loads.

CC Q1 2019 - Bradley S. Jacobs, XPO Logistics, Inc. - Chairman & CEO

“Yes, we are fully on track to achieve $1 billion of EBITDA in LTL in the next few years. EBITDA is going to go up every year in LTL and it's going to draw off a boatload of cash as well. It's a winning model. It's got a great service metrics, got a great installed customer base. It's functioning. It's functioning and it's going to keep growing and expanding, and we will hit that $1 billion EBITDA sooner than you may think.”

CC Q1 2019 - Bradley S. Jacobs, XPO Logistics, Inc. - Chairman & CEO

So in our LTL, our -- what we call our local account are booming, and we're seeing enormous growth in that, and that's something if you look over the last several years, you've seen a big shift in the percent that we have with those smaller customers going up to where it is right now. So that will continue in LTL. We'll also get more national account business, but there's more growth in those smaller accounts.

CC Q1 2019 - Bradley S. Jacobs, XPO Logistics, Inc. - Chairman & CEO

“Our smart program is our labor management tools and they work so well in our contract logistics business that we're now rolling them out in LTL. And in LTL, we have about $1.7 billion in labor costs. Really, we have a vision to be able to run the set of business we have right now at $100 million to $300 million less labor costs over time. How we're going to that? By using smart labor tools. The smart labor tools allow us, in an objective way, in a mathematical way, using predictive analytics, by using AI, to say, what's the right amount of headcount we want? Not too much, not too little, but just the ideal headcount for the project, and we have to use predictive analytics in order to understand what the tonnage is likely to be the next day. And then we use the smart technology to know what's the right ratio between full-time workers and part-time workers, what's the right ratio between dockworkers and drivers, what's the right amount of overtime.”

General favourable secular market dynamics, like an ongoing move to just-in-time delivery across supply chains, continuing e-commerce and omnichannel growth along with shorter delivery times (Amazon now pushes hard on 1-day delivery times as the new Prime-standard) and greater supply chain complexity for traditional retailers and brands plus higher customer expectations on the technology front along with the necessary investments regardless of size should provide continuing growth opportunities for the larger, well run players. This does not only apply to LTL. Positive industry trends should be tailwinds across the various XPO segments more broadly.

If one looks at the biggest acquisition, Norbert Dentressangle (ND) for an EV price tag of $3,5b (they own only ~86,25% of the shares) one can’t objectively say that they have failed here either. The operating improvements are less exciting than what they have achieved in LTL with Con-Way but they are nonetheless notable. ND also has close to 30% of the business each in the UK and France, so macro hasn't exactly been a tailwind. EBITDA is up by $100m or ~30%. The stub share price is up >40% and relevant ~3-year average KPIs prior to the acquisition and after the acquisition paint a decent picture:

|

In USD at 1,12 exchange conversion |

Sum of years: 2013,14,15 |

Sum of years: 2016,17,18 |

Delta in $ and % |

|

EBITDA |

$925m |

$1210m |

$285 / +30% |

|

OCF |

$630m |

$1080m |

$450 / +71% |

|

CAPEX |

$495m |

$565m |

$70 / +14% |

|

FCF |

$135m |

$515m |

$380 / +280% |

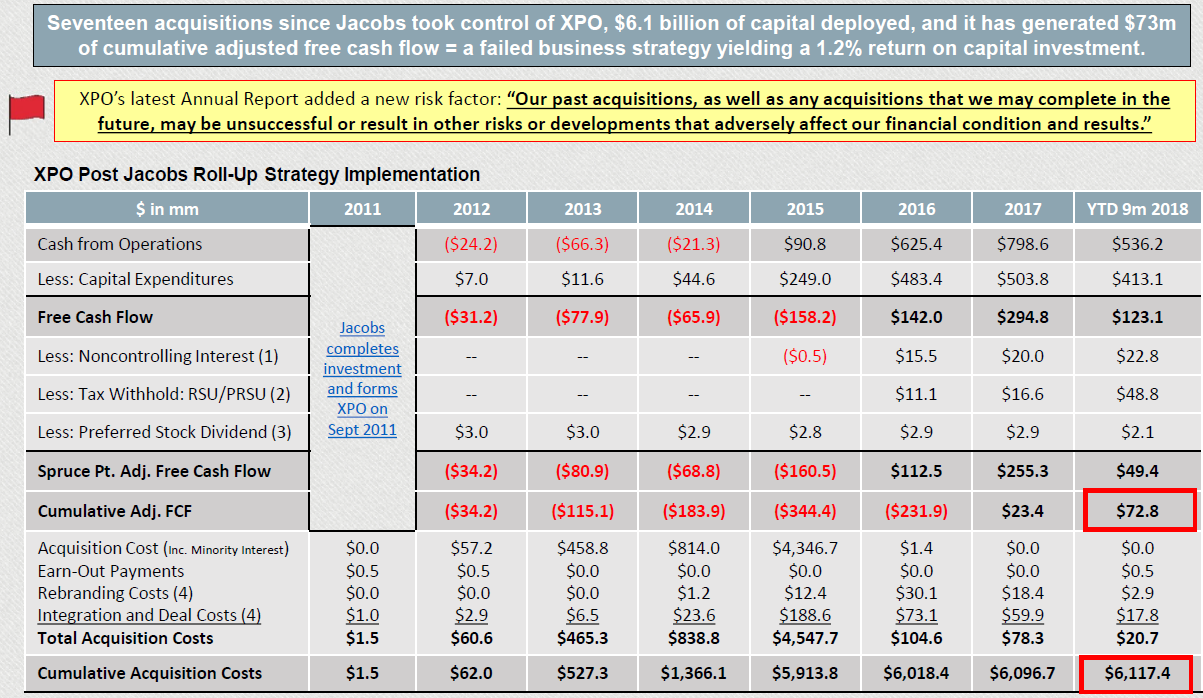

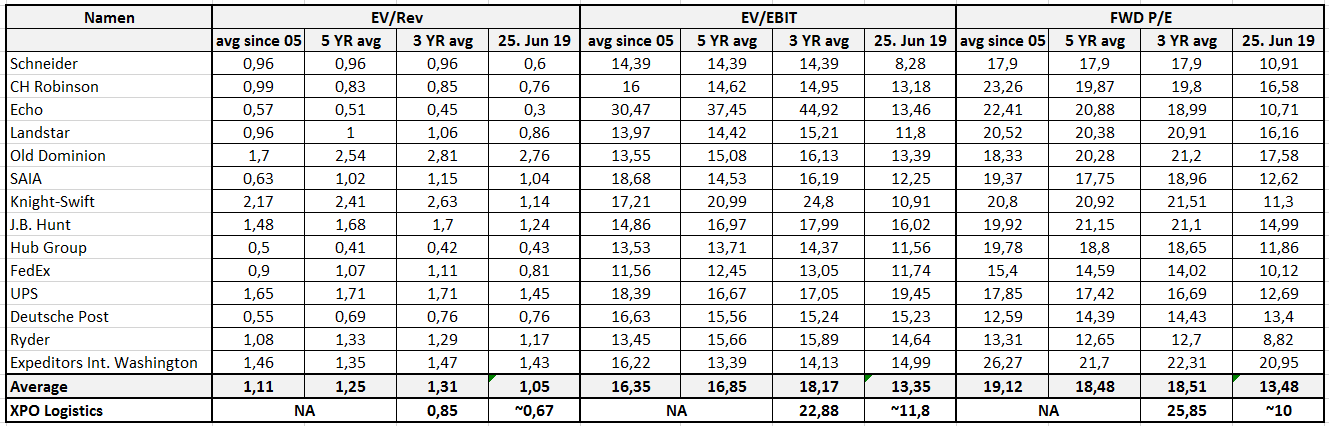

True capex is also only ⅔ of the stated number and FCF accordingly higher due to continuous equipment sales, which have already regularly taken place long before XPO took over the business. The market currently values ED at an EV of $4,3b in case one wants to think about a SOTP valuation for XPO. With LTL covered and some evidence that they are in fact good operators and not just financial Ponzi scheme artists, we can almost move on to talk about full truckload and contract logistics. Here is one more slide in Spruce Points deck that looked like this:

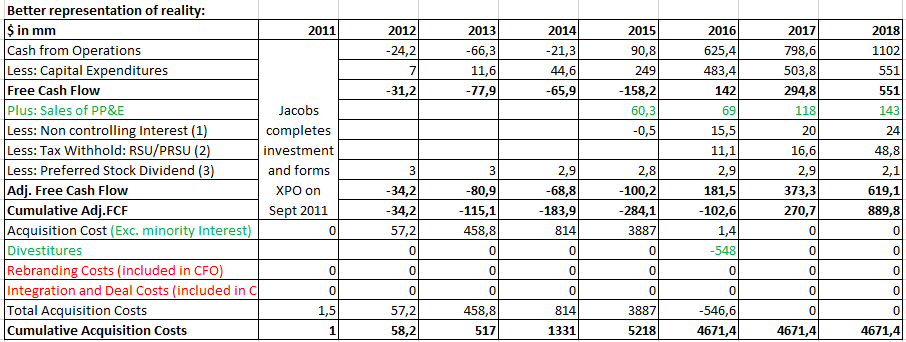

However, if you take the full year 2018, include the divestment and PP&E sales that are part of the business, don't double count rebranding and integration costs that are already included in cash flow, the picture looks more like the following table and the return edges up to 20%. With a good chunk of debt involved you also have an explanation why Jacobs still owns 20% of the business stemming just from his $150m investment in 2011. His stake is currently worth $1b. Valued more fairly he has achieved a 10x return.

Truckload and freight brokerage

TL is by far the largest segment of the transportation industry. With its many thousand trucking companies in operation, it is much more commoditized and considerably less attractive business than LTL. The largest asset-based player in the market is Knight-Swift Transportation but with their owned fleet of close to 20’000 tractors, they are still only a drop of water in the ocean of trucks out there. The 10 largest operators account for only ~5% of the market and apparently 80% of all truck drivers work at companies with less than 10 trucks. Given this very fragmented landscape, with thousands of shippers and carriers with different needs across the country, somewhere out there is always the best truck for a particular freight and vice versa. Therefore, the most value creation and capture has come and will continue to come from successfully connecting those parties. XPO quickly sold the self-operated TL US business of ConWay after they acquired the company and as a result is mostly active as a freight broker in TL. They only kept NDs fleet in Europe in addition to acting as a freight broker there.

The brokerage business continues to become more important and has grown to around ~20% of the total freight market, twice its pre-crisis level. It is an integral part of the transportation business, with many asset-based carriers active as brokers as well. If their sales person can get a transportation job, they obviously don’t want to say no to the new business just because they don’t have matching trucks/drivers for the job themselves. With the knowledge of all those empty trucks and small operators out there, it is relatively easy to do so and simply a forgone opportunity not to. At the same time, every carrier is willing to take at least some work from other trucking companies, because you want your trucks to run as full as possible, but won’t be able to get all the freight you need to minimize empty miles on your own. Shippers engage with brokers because they don’t want to or don’t have the means to manage the logistics complexity and relationships with multiple players themselves. There is a desire for an outsourced solution that takes care of all transportation needs. Otherwise, you have to take those people on your payroll and increasingly you’d also need to build advanced software solutions in-house. While someone like Amazon certainly has the means and technology capabilities to insource more and more of their transportation needs (long-term they will quite likely also become a provider to other companies), it seems more likely that fewer companies will be able to do so successfully the more technology there is involved.

The brokerage business has its obvious attractions, it is asset light, has high returns on capital, scale advantages and ongoing growth potential. At the same time, there are certainly also margin compression risks for everyone involved and disruption risks for players who won't be able to stay on the tech forefront. There is still an awful lot of costly human labour involved in brokerage. With a growing importance of technology and less reliance of human labour and relationships, the business will certainly see consolidation. Here is a recent take on the future development of the brokerage industry from Jacobs, which we tend to agree with:

CC Q1 2019 - Bradley S. Jacobs, XPO Logistics, Inc. - Chairman & CEO:

I think brokerage going pretty much along the way that we thought it was going to go years ago. It's becoming more automated, bigger impact of technology, more and more digital interactions, electronic interaction rather than human interactions. I think long term, margins come down. I don't necessarily think short-term margins come down, but long term, I think, as costs come out of the way brokers do business, a good chunk of that cost savings is going to get passed along to customers and that's going to degrade margins. Now having said that, lower margins on a much larger amount of business with lower SG&A can still be a beautiful thing and you can still create a lot of value from that. And I think there will be a shrinking of the number of players. There's not going to be 10,000 or 20,000 brokers 5, 10 years from now. I think it will be a smaller number of larger brokers who have very significant investments in technology and are tightly integrated electronically with both customers and carriers.

XPOs total TL brokerage revenue adds up to be #2 globally behind the leader C.H. Robinson, a company that probably isn’t a stranger to many. In the US, XPO is further behind CHWR in a field of other notable players like private TQL (larger), public Landstar (larger), UPS subsidiary Coyote (similar size), DHL subsidiary Worldwide Express (smaller) or public Echo (smaller). Thereafter follows a long list of other smaller brokers. The currently frequently discussed new modern tech first entrants like Convoy or Uber are all even taken together still small. They will probably accelerate margin compression and tech adoption in the business, but they likely won't replace the largest participants that are awake. The required software is not that revolutionary that only the best 100 people in the world can build it. The massive market will quite likely also see more than just three winners for a long time and XPO seems large and fast-moving enough to be among those winners.

CC Q3 2018 - Bradley S. Jacobs, XPO Logistics, Inc. - Chairman & CEO:

Over 50% of our loads in truck brokerage today are offered to our carriers electronically. Not from someone talking on the phone to a dispatch, talking to a driver. Automatically, electronically, over the computer. And they're customized for the carrier's preferences. So we're very much at the cutting edge of technology in terms of truck brokerage, and we firmly intend to stay at that cutting edge. Now you asked about some of the start-ups and some of the new entrants. Some of those new entrants aren't going to work, but some of them will over time. But today, at this moment, if you add up all the new entrants who've come in over the last 5, 6, 7 years, you don't even get to $1 billion of revenue in aggregate. So our competition today is, of course, C.H. Robinson is much larger than us in truck brokerage, at least here in United States. And TQL and Echo and they're large established, for lack of a better word, bricks-and-mortar trucks brokerage. Like all of them are also going electronic as well. We're leading the pack on that.

Scale and breadth across more than one service line are also advantages for lining up large shipping customers that the new guys lack. The advanced algorithms also need scale to do the network optimization properly. Furthermore, even if the new entrants are able to get carriers to adopt their services with low acquisition costs, they still need a salesforce like everyone else does to get the shippers onboard. There is too little new magic involved that shipping customers will adopt those services on mass just by themselves. The margins in the spot business will see quicker compression and a faster route to full digitalization than the contractual side. XPO like everyone else always has a mix of spot and contractual, that moves around depending on market conditions. Here is some commentary

CC Q3 2018 - Bradley S. Jacobs, XPO Logistics, Inc. - Chairman & CEO:

A significant shift from spot exposure to contractual business. And our proportions have basically flipped. And right now, we're roughly 45% spot, 55% contractual. We've got assets that, early in the year, would've been exact opposites. So yes, customers are looking - absolutely preferring more to do long-term contractual business than spot. Now they can't - many customers can't go to 100% spot -- 100% contractual because they don't know what their volumes are going to be. So there's ebbs and flows, and they rely on the spot market for those peaks.

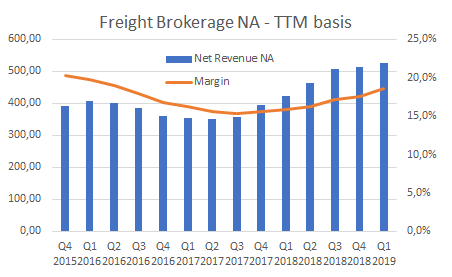

The following chart shows XPOs net revenue and net margin trends on a TTM basis. Net revenue is the spread of what they charge to shippers and pay to carriers. So basically the only relevant revenue for a broker.

The business is growing, nothing outstanding to note here. The LED introduction plus decent economic growth last year tidened the market quite a bit with conditions now easing again. This spread business obviously has demand and supply based cycles. However those cycles are to a degree leveled out by always having a mix of spot and contractual business where margins often move in opposite directions in the short term. With XPO’s reporting it is hard to know how profitable the segment exactly is, so valuing it becomes even more of a guessing game than it usually is. Together with the last mile business and managed transport it contributes around $300m in EBITDA and $150m in operating profit.

Logistics business

XPOs last business segment is contract logistics, where they basically take over and run warehouses on behalf of customers. XPO is a large player in the market (globally #2 behind DHL) with customers coming from many different industries. In total they run over 800 warehouses with warehouse space of over 18m square meters. The value creation and attractiveness of this business is all over the place. It ranges from basically providing simple labour arbitrage, where the outsourcing’s party primary reason is to avoid having the required employees on the payroll and to save some money because the third party can pay less, to providing a national warehousing solution with shared warehouse space across multiple locations to enable 2-day shipping across the country, where also modern automation solutions come to bear. In a bull case they continue to grow at a healthy clip, are able to deploy more technology to this field, find success with XPO Direct (the shared warehouse space) and partnerships like the one they have with Nestle in the UK (both projects are described in XPOs pitch book referenced at the beginning). The automation equipment inside the warehouses will likely always be bought externally which means everyone else can buy as well. However, XPO also has internally developed warehouse management systems that connect to clients ERPs. They are also in a position to easily extend out and integrate it with their transport management systems. So in their role, they can and likely will continue to be a strong operator experienced in best practices with decent software solutions that can partner with many companies for complex logistics.

The business adds up to $500m in EBITDA and ~$240m operating income to XPO. Roughly ~60% of it is booked inside of ND which contributes the majority (over 2/3) of operating income and ~40% is booked outside of it directly in the mothership.

Profits recently got hit by a larger customer bankruptcy in the UK where they took a $16m impairment in Q3, they also lost business from Amazon and closed down two facilities. Amazon overall pulled $600m of businesses, which hit the transport segment harder, but also hit this segment. Overall they booked impairments of $19m in Q4 2018 and $13m in Q1 2019. Here is some commentary around logistics ambitions and recent events.

CC Q4 2017 - Bradley S. Jacobs, XPO Logistics, Inc. - Chairman & CEO:

We actually have a lot of e-commerce business in our contract logistics business here in United States because of the -- all the reverse logistics, the returns management that we do and because of the omnichannel distribution. But our contract logistics business is broad: we have 11 different verticals. We have omnichannel retail, we have aerospace and government, we have automotive and industrial, technology, food and beverage, chemical, healthcare, oil and gas, agribusiness, consumer packaged goods, and a small portion is managed transportation. And that's - so it's really broad-based, and that's reflective of our whole company. We are exposed to every part of the economy all across Europe, North America and a few places elsewhere.

CC Q2 2018 - Bradley S. Jacobs, XPO Logistics, Inc. - Chairman & CEO

The network (XPO Direct) is primarily for heavy goods, but it's also competitive for small parcel solutions, but that's through arrangements with the parcel carriers. We had an RFP and we selected 1 partner for that and that's who we're using. Customers want predictable, fast, integrated, end-to-end solutions for all their transportation needs, that is where the world is going towards. People don't want to have 5 different vendors to get their goods from where they are to the end customer. So that's what we're giving them. We're giving them an opportunity to have an integrated one-stop shop. Will we have to add more capacity as the business grows? Yes, because we expect this to be a $1 billion revenue business within a few years. And each part of the business that we have, whether it's the warehouse component, whether it's LTL component, whether it's last-mile component, we'll grow the business with that. But there will be great returns from it.

CC Q2 2018 - Bradley S. Jacobs, XPO Logistics, Inc. - Chairman & CEO:

On XPO Direct, you're exactly right. It is ramping up. This is roughly $1 billion business opportunity annually to report $1 billion in revenue from this over the next 3 to 4 years. What we're seeing is a lot of demand not only from the retailers and the e-tailers, we talked about that, where they're signing for time definite, fast order fulfillment for store replenishment. But we're also seeing a lot of demand from manufacturers, from suppliers. They're looking at this as a one-stop shop, where they can pool their inventory, they can fulfill for all their selling channels. Things like their own websites, when they're selling goods, things like partner retailers that they work with. This is an opportunity that will likely have higher margins than our average margin in contract logistics. Right now, it's in investment stage

CC Q3 2018 - Bradley S. Jacobs, XPO Logistics, Inc. - Chairman & CEO:

We're excited about the growth path we've created for contract logistics. Customers are continuing to outsource to us at a rapid pace. They like our advanced automation, our deep vertical expertise and our ability to secure talent. XPO is known in the industry as being a strong operator and the partner of choice for complex logistics. Last month, we announced plans to deploy 5,000 more intelligent robots in our logistics sites through a strategic partnership with robotics manufacturer Gray Orange. These robots have helped our employees to be about 4x more efficient while improving order accuracy. We've also been able to increase the density of product storage and enhance workplace safety.

CC Q3 2018 - Bradley S. Jacobs, XPO Logistics, Inc. - Chairman & CEO:

Our XPO Direct shared space distribution network is ramping up fast. We now have 94 facilities in the network, up from 75 last quarter, with 2 more locations opening this month. Last week, the total value that ramped through XPO Direct was approximately 20x greater than what we shipped weekly during the summer. Most of this is coming from e-commerce and omni-channel customers. We also have some manufacturers looking for flexible distribution capabilities. We expect volume to step up again this quarter followed by an even more significant increase in the beginning of 2019. We expect XPO Direct to be a $1 billion business over the next 3 years.

CC Q4 2018 - Bradley S. Jacobs, XPO Logistics, Inc. - Chairman & CEO:

So we're clearly in growth mode in the contract logistics. Growth remains very strong there. You saw that in -- North America organic revenue growth in the fourth quarter is 17%. And our strength in consumer packaged goods and in food and beverage and e-com, growth is accelerating in these places. Now I feel very, very bullish about our -- I think on the supply chain part of our business very, very strong. So the challenge we have is more on the tech. Now you mentioned a couple of facilities that get a lot of press closing, 2 of them, which were -- one on the East Coast, one in the Midwest. That was with our largest customer. So those were contracts that had been many year contracts and the contract were coming up for renewal or for ending. And they chose to end them. And I don't know for sure whether they brought them in-house or not, but whatever they decided to do with them, we respect that decision. The customer is the king, and the customer can decide whatever they want to do with those. You mentioned the Verizon facility. We have a great relationship with Verizon. It goes back decades. They're an important partner of ours. It's strong. We serve them in many parts of the country, and we love them. We think they're an amazing company, and we wish we had more of Verizon. We did close 1 facility in Tennessee because Verizon is always evaluating its supply chain. They have a complex supply chain, a big supply chain. It's a global supply chain. And they made the decision to transition the distribution of their wireless products out of Memphis to several other distribution centers around the country. So that is just one part of their ongoing process.

Prior to losing ⅔ of Amazon business, the top 5 customers accounted for about 11% of revenue and Amazon was a little more than 1/2 of that. Going forward, it will be more diversified. The top 5 customers in 2019 should be around 7% of revenue and no customer will be more than 2% of revenue. Generally the diversification not only across customers but more importantly across different business lines as well as geography (with the US and Europe) provide a more resilient business than some of their peers have, who are often operating in just one business line and just one geography.

Here are XPO’s recently published full-year 2019 financial targets:

- Revenue growth of 3% to 5%, which corresponds to organic revenue growth of 5.5% to 7.5% year-over-year*

- Adjusted EBITDA in the range of $1.650 billion to $1.725 billion, an increase of 6% to 10% year-over-year

- Free cash flow in the range of $525 million to $625 million**

- Net capital expenditures in the range of $400 million to $450 million

- Depreciation and amortization in the range of $765 million to $785 million

- Effective tax rate in the range of 26% to 29%

- Cash taxes in the range of $165 million to $190 million**

*The 5.5% to 7.5% outlook for full-year organic revenue growth equates to the 4% to 6% target issued in February 2019, adjusted for the exclusion of direct postal injection revenue in our last mile business

**The 2019 targets for free cash flow and cash taxes assume cash interest expense of $275 million to $315 million. We expect an incremental benefit to free cash flow of $125 million to $150 million from trade receivables programs in 2019

We think a more reasonable enterprise value for XPO should be around $13-15b, which translates into:

- 12,5-14 x EBIT (with the non-economic of ~160m amortization added back)

- 7,5-9 x EBITDA

- 13-16 x FCF for equity

- Upside of +30-60% for the shares

Here is some external reference to chew on:

For XPO we have added back the non-cash amortization from the acquisitions. We also do not count the leases that came on the balance with the recent accounting changes in XPOs EV and don’t add back rent expenses. The majority of those leases are tied to individual logistics contracts matching contract lengths. Overwhelmingly they can easily get out of those leases if a customer decides to terminate the contract earlier than agreed upon. Those leases are much more an operating cost than a liability that is stuck with you no matter how business goes.

Finally, let's look beyond the current issues and draw a bullish future where a share price back at over $80 wouldn’t be shocking at all. In about a year people can start to firmly look at 2020 guidance which will be better than this year with some easy H1 lapping and ongoing growth. At that time the company will have moved beyond its current problems, with a permanent CFO quite likely in place and the elevated C-suite turnover as a story of the past. The lost business from Amazon will be replaced with more profitable business by smaller customers that have less negotiation leverage. Amazon’s ding to the numbers will be visible as such and can no longer be interpreted as a threat of overall deterioration. People can start to become excited about getting LTL to $1b in EBITDA. New innovations from the bigger players on par with the new entrants, but at work on a larger scale could make questions and stories about them less exciting and them also appear less threatening. Some deleveraging will have taken place and Jacobs might have already started to hint at doing some exciting and very accretive acquisitions again.

I wrote down those lines because we believe the narrative here can change quickly. This is of course not meant to get VIC members excited. We value guys don’t get excited by such stuff. We, on the other hand, worry about a potential recession, which would certainly postpone a narrative change and more love for XPO. And here you have written down also what we believe to be the biggest risk to XPO, a deterioration in the broader economy.

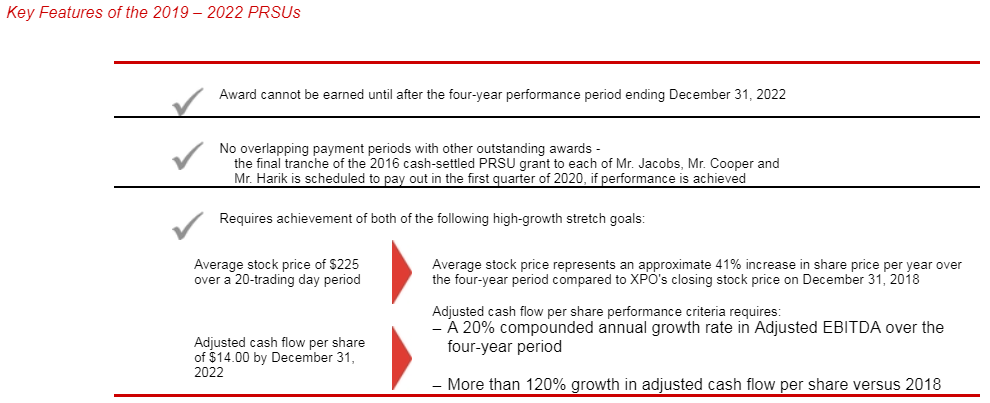

Just before this current episode hit XPO, they have put out a new compensation plan for the next several years. Here are the main points:

The targets are certainly bullish (CFO is also their definition of FCF). The good thing is, we are not paying for any of that to have to play out. We are paying ~10 x cash earnings for this business. Here is some Q and A after they have implemented this comp plan:

Bascome Majors, Susquehanna Financial Group, LLLP, Research Division - Research Analyst

The 8-K you filed this morning gave some color on serious restricted stock award around the interim CFO. And the disclosure was basically that stock needs to double again to $200 over the next 5 years, which would be a compound equity or return of about 15% over that period. Brad, can you share your and the board's thought process behind that incentive? And what it says about your longer-term expectations for XPO and shareholders?

Bradley S. Jacobs, XPO Logistics, Inc. - Chairman and CEO

Yes, we are fervent believers that management should not get paid a lot of money, if we don't deliver a lot of shareholder value for our owners. And we are equally fervent believers that if our management team delivers superior value to our shareowners then they should get paid really well, that is what allows us to attract great talent and that's our philosophy in compensation. In terms of how we calculated the number, it goes back to the earlier question on the call, which is, if we continue to grow EBITDA in the mid- to high-teens percent and then you look at the leverage that we have, and you take the free cash flow we generate and then pay down debt, it's just math. If we keep the same multiple, the stock should go up in the mid-20s per year. And if we get multiple expansion then every turn of multiple expansion is about $13, $14 a share. So with Sarah, we made it so that she gets a grant of about $2.5 million that, at today's price, obviously, we work twice that at $200. And it dependent on that and there's other conditions as well. But we're all in it for the shareholders. So we want our compensation plan to be geared towards shareholder appreciation. It's as simple as that.

Bascome Majors, Susquehanna Financial Group, LLLP, Research Division - Research Analyst

I appreciate that thoughtful response there. And kind of maybe extending that discussion, I think, we're about 2.5 years into the current long-term incentive plan for senior management, which I believe is tied pretty squarely to improving free cash flow per share of the company. Now -- it sounds like we're about to add some business at the portfolio, before the not too distant future here. Just how do you expect that long-term incentive to maybe change, as we get through the next round of acquisitions here?

Bradley S. Jacobs, XPO Logistics, Inc. - Chairman and CEO

Well, all of our -- we have many different compensation plans throughout the company. And as you go down in an organization and closer into the field and close to the customer, we like to tie the compensation to what that person or that group of people can do to contribute towards that $1.6 billion EBITDA, Nick, this year and the higher amount of EBITDA next year and the following in the following year. But we don't just usually, tie it to EBITDA. We tie it to EBITDA minus CapEx minus other charges that get us to free cash flow. And at the end of the day, cash is king. And tying compensation to free cash flow makes a lot of sense. But the people in the field don't have a whole lot of control over that. So we try to have their compensation tied to their KPI. At the senior level, we do feel that compensation should be primarily tied towards things that create shareholder value. And from a financial perspective, it's cash.

Bascome Majors, Susquehanna Financial Group, LLLP, Research Division - Research Analyst

Great. So it sounds like the focus on free cash flow at the senior management level is unlikely to change?

Bradley S. Jacobs, XPO Logistics, Inc. - Chairman and CEO

It's unlikely to change. You could see variations of it as we adopt best practices and we fine tune it with shareholder input, which we always take. But the basic concept of tying senior management equity incentives to long-term shareholder value is a core part of our culture. We pay our people well, but if and only if, they deliver superior value to our shareholders. Otherwise they get a reasonable, but not great base salary.

And finally some more capital allocation comments in no particular:

Bradley S. Jacobs, XPO Logistics, Inc. - Chairman and CEO

And the other part of your questions, do we plan to buy truck brokers in terms of our long-term growth plans? I don't know. We always wanted to buy truck brokers. We bought a few small ones. We never -- the reason we mainly didn't buy many more truck brokers is because the valuations are really high. In the private market, the larger truck brokers don't come on the market very often and when they do, they go for very big multiples. And we're very conscious about the price we pay in M&A. For us, M&A -- the purchase price is critical because that's the I in ROI for - in M&A. So it's the same reason we haven't gone big in M&A in Asia, you have scarcity value and then when properties come out in the market, the multiples get very, very rich. So I don't know. I don't see brokerage multiples coming down any time soon. So I don't know and I don't see us returning to the M&A market immediately either.

Bradley S. Jacobs, XPO Logistics, Inc. - Chairman and CEO

Our M&A strategy is to buy a great company or two at a reasonable valuation. One that's strategically compelling. One that's very, very accretive to our earnings. One that our -- one or two that our customers really like us doing, and one or two that our shareholders will like us doing. The tax law is sort of a side issue in terms of what we're doing there

Do you see an opportunity for additional LTL consolidation in the US?

Bradley S. Jacobs, XPO Logistics, Inc. - Chairman and CEO

Well, not for XPO. We don't see any need -- we have a network. We have a network of nearly 300 service centers all over, very strategically placed. And we cover nearly all zip codes. So we have a very fine functioning field network of service centers. Wouldn't make much sense for us to buy another asset network company. I can't see the logic in that off the top of my head. It's not something that is on our drawing board. In Europe, as opposed to here where we're the second largest, we actually are the largest. We're the leading LTL player in Western Europe. And there we use a combination of both an asset-based model and a non-asset-based model, for example in Spain, in response to customer demand.

I and/or others I advise hold a material investment in the issuer's securities.

Catalyst

change in narrative like laid out in the write-up

| show sort by |