| 2021 | 2022 | ||||||

| Price: | 7.35 | EPS | 0 | 0 | |||

| Shares Out. (in M): | 232 | P/E | 0 | 0 | |||

| Market Cap (in $M): | 1,704 | P/FCF | 0 | 0 | |||

| Net Debt (in $M): | 43 | EBIT | 0 | 0 | |||

| TEV (in $M): | 1,747 | TEV/EBIT | 0 | 0 | |||

Sign up for free guest access to view investment idea with a 45 days delay.

- SPAC!

- None found

- BETA

- PUBMATIC INC PUBM 04/29/2022

Description

Summary: Taboola is an overlooked ad-tech business trading at 2.6x fwd gross profit and growing in the mid-teens. Taboola is a content recommendation system that matches publisher inventory with the right advertisers. The combination of going public through a SPAC and being in the ever-changing ad-tech industry underpin the mispricing today. I believe that Taboola is at an inflection point in growth and will take significant market-share from its competitors. Furthermore, Taboola is particularly well-positioned to take advantage of changes like IDFA and the impending disappearance of 3rd party cookies. Putting things together, I think it is not unreasonable to assume that Taboola will earn $940m of Gross Profit in 2025 and be valued at ~$3.4b by YE 24, or a 102% 3-year return.

Business Overview

Taboola is a founder-led content recommendation platform for ads on the Open Web. Particularly, Taboola has one of the largest inventories of non-programmatic ads on the internet. As companies are looking to diversify advertising away from Walled-Gardens (Facebook, Google, Amazon), Taboola is unlocking a new TAM that was previously overlooked. Most popular is their widget at the bottom of the page, which is ad space that was previously never used.

Right after going public, Taboola decided to acquire Connexity and Skimlinks for ~$800m. Connexity is a performance-based marketing software for e-commerce. Perhaps the most popular version of their product is a buy-now widget embedded in articles to link products (Appendix 1). The platform drives $4B of annual sales for their retail partners and includes blue-chip clients like Wayfair and Chewy. Skimlinks is the leader in affiliate marketing software.

Industry Overview

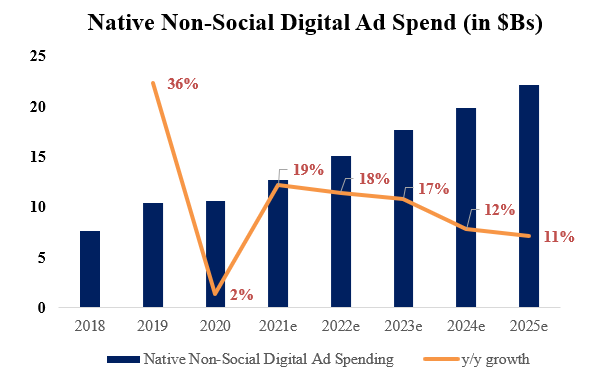

Taboola is part of the digital display ad market and is particularly exposed to non-social display ad growth. eMarketer estimates the total digital ad spending in 2021 to be ~$211B, out of which Taboola’s market niche, Native Non-Social Display Ads, will be $12.7B.

The key player’s in Taboola’s end-market are them, Outbrain, and to a much smaller extent Revcontent. Given the reliance on 1st party data, there is an opportunity for winner-take most dynamics to occur in an end-state. Superior data and data-analysis means better targeting, leading to better returns on ad spend for advertisers and higher RPMs (Revenue per Mile, measure of publisher revenue for given ad inventory) for publishers, and market-share gains for the most-scaled player.

It is not hard to foresee Taboola’s market growing to roughly $22B by 2025, which I project by growing it slightly faster than eMarketer’s estimates for the overall Digital Ad spending market. This is reasonable given Non-Social Native ad spend grew 36% in 2019 compared to 19% for overall digital ad spending growth.

If Taboola were to simply grow in-line with industry growth rates, they would generate $865m of ex-TAC gross profit and $260m of EBITDA in 2025. Tacking on another ~$50m generated by Connexity, which will likely prove to be fairly conservative, this would result in $310m of EBITDA in 2025. At a modest 12x fwd EBITDA, Taboola is a more than 2x in 3 years from here.

However, it is also very likely that Taboola will put up above industry average growth rates given they will take share vs competitors and non-programmatic ads will take share.

Thesis

-

IDFA & 3rd party cookie changes will drive mix-shift in ad spend towards Taboola

-

Taboola is poised to win the non-programmatic digital ads market, given they are deepening the data moat vs Outbrain, leading to better yield and market share gains

Thesis 1) IDFA & 3rd party cookie changes will drive mix-shift in ad spend towards Taboola

While advertisers have already been trying to diversify away from Walled Gardens, IDFA changes are negatively impacting ROAS for companies like Facebook that were somewhat reliant on it. However, perhaps the bigger loser is DSPs and SSPs, who will have a harder time profiling users now. So, while Taboola will be slightly negatively impacted from the IDFA changes, their reliance on mostly 1st party data means that the impact on Taboola’s RPM will be far more muted than on that of large programmatic players.

The demise of 3rd party cookies in 2022, and ongoing and past privacy changes like GDPR in 2018 or California Consumer Privacy Act (CCPA) in 2020 are going to have a similar impact. DSPs and SSPs that are heavily reliant on 3rd party cookies will be significantly impacted. Agentcooper2120’s Magnite write-up thoroughly discusses this, but it is interesting to note that currently, 2/3rd’s of Magnite’s revenue is exposed to 3rd party cookie data.

Per a Taboola Former regarding IDFA impact & 3rd party cookies impact:

“I think it's an opportunity for them to steal share in that because I think they will be impacted. I don't know. If I was going to guess, their CPMs could take 10% to 15% hit. I think other places might take a 30% hit. So, if now their value is even better than it was before, hopefully, they can steal share.”

Thesis 2) Taboola is poised to win the non-programmatic digital ads market, given they are deepening the data moat vs Outbrain, leading to better yield and market share gains

Given the heavy reliance on 1st party data and the fact that this business is purely driven by RPMs, Taboola’s recent acquisitions of Connexity and Skimlinks make them best positioned to deepen their moat and win market share. While I am cognizant of companies that like to make nice IR decks and put-up pictures of flywheels, I think the graphic here makes sense:

Publishers also confirm this:

“So, I mean, super impressed by what they brought together because I mean, we use Outbrain today, which is one of the Taboola competitors. But we use all three pieces that they have purchased, and you can definitely see how they could come together and bring better solutions for publishers as one.” – VP at Meredith

I also think that deepening the data moat prevents the race-to-the-bottom risk between Taboola and Outbrain. If both players had access to the same data set, and we make the assumption that Taboola and Outbrain have the same R&D capabilities, the product is simply commoditized and the publisher revenue split would quickly dwindle as both would try to gain share. Having access to greater data, hence, builds a competitive advantage for Taboola, since they should be able to drive structurally higher RPMs.

However, I also believe Taboola has a superior value proposition for advertisers and has the flywheel spinning now. Two key reasons why:

-

Per industry experts, Taboola has the most ad inventory on their platform. This is further supported by Taboola having 9,000 digital property partners on their platform compared to 6,000 for Outbrain. At least in Europe, here is what a customer thinks:

“Taboola has acquired a lot of the inventory that other channels used to have. Typically, the reason why you would want to mix before is because Taboola had Mail Online and Outbrain had the Financial Times and Sky News. To get access to the maximum inventory, you would have to work across multiple networks. Taboola now has essentially acquired most major publications and media brands in Europe.”

-

Taboola has a cleaner platform and superior content recommendation algorithm. Firstly, they outspend Outbrain by more than 3x on R&D spend. This translates to a better algo, and here is a quote from a customer supporting this:

“The other thing that we found especially with Outbrain is it was a lot less optimized and refined than Taboola was in terms of its algorithm and ability to target people. The cost to acquire customers on Outbrain was a lot higher than it was on Taboola” – Director of Marketing at a Customer

Putting things together, I think that having a structural data advantage and superior supply vs Outbrain will mean that more ad dollars will flow to Taboola. If Taboola is truly successful in aggregating supply, or better-put, their incremental supply market share starts to inflect upwards, demand will follow.

Does Management Help?

Adam Singolda is the Founder and CEO of Taboola. I am positively biased towards founder-led businesses, and Adam definitely has big-hairy goals that he wants to achieve. The concept of Taboola Everywhere was thrown out in their recent investor deck, but the LT vision for the business is to be in every android device and he is already thinking of news feeds in autonomous cars. While it is easier said than done, Adam seems like the right man for the job. A testament to his ability is the fact that he bootstrapped what is today a ~$500m gross profit business as his first job.

Reasons Mispriced

-

Went public through a SPAC: Beat down recently

-

Ad Tech is undergoing significant change, and there is a lot of skepticism around players overly reliant on 3rd party cookies. However, Taboola is a strong business with a moat that will benefit as programmatic players are impaired.

Valuation

Valuation math is attractive for Taboola when it is priced at 2.6x fwd Ex-TAC Gross Profit, which is more so reflective for revenue. The cost structure on this GP base should be minimal at scale, since Taboola will be similar to a scaled marketplace connecting buyers and sellers with great S&M efficiency. As such, assuming a 30% normalized EBITDA margin, the valuation can be cut two ways:

-

As discussed earlier, a top-down build means the stock is more than a 2x in 3 years from here

-

Bottom-up, I forecast Revenue through projecting advertisers and spend/advertiser:

-

Advertisers: Taboola has over 14,000 advertisers on the platform today and added 2,000 in 2019. Furthermore, I think that they were far more focused on aggregating supply than driving advertiser growth over the last few years. I think it is fairly conservative to assume ~1,500 advertiser net adds/year through 2025

-

Spend/Advertiser: Spend/Advertiser has been flattish for the last 2 years, but NDR on the advertiser side is in the 110s in 2021. I grow this at ~1%/year through 2025, and think there is upside risk of this being a lot higher.

-

Connexity: Taboola believes there is ~$100m of revenue synergies between them and connexity. This combined with organic growth means that it is not hard to imagine $168m of Net Revenue in 2025 compared to $77m in 2020.

Together, this yields a ~$940m in Ex-TAC Gross Profit opty in 2025. If this drops down to EBITDA at 30% as the company has guided, and I think is quite conservative, that is $280m EBITDA, which at a 12x fwd multiple yields a $3.4B EV, or 102% upside from today thru 2024.

Downside Protection:

Taboola was supposed to merge with Outbrain in Sep 2020, but it was called off given the industry was undergoing change during Covid-19. Earlier this year, Taboola bought Connexity for $800m, suggesting that they see more value in trying to go after the market with a data moat, rather than consolidate. Today, Outbrain is a $550m EV, so if Taboola really feels the need, they can try to restart merger discussions and become a unified scaled player.

Appendix 1: Connexity Overview

Buy now widget is powered by Connexity

I and/or others I advise do not hold a material investment in the issuer's securities.

Catalyst

- Initiations from larger banks

- Market share gains

| show sort by |