| 2018 | 2019 | ||||||

| Price: | 1.48 | EPS | 0 | 0 | |||

| Shares Out. (in M): | 576 | P/E | 0 | 0 | |||

| Market Cap (in $M): | 103 | P/FCF | 0 | 0 | |||

| Net Debt (in $M): | -21 | EBIT | 0 | 0 | |||

| TEV (in $M): | 82 | TEV/EBIT | 0 | 0 | |||

Sign up for free guest access to view investment idea with a 45 days delay.

- oil service recovery bet

- Standard Drilling SDSD 04/24/2020

- Standard Drilling SDSD 06/02/2017

- BETA

- DANAOS CORP DAC 02/08/2023

- Trico Marine TRMA 01/23/2008

- MC Shipping MCX 12/29/2006

- NAVIGATOR HOLDINGS LTD NVGS 03/13/2015

- CENTENNIAL RES DVLPMNT INC CDEV 02/08/2020

- COOL COMPANY LTD COOL NO 02/28/2023

- Rand Logistics RLOG 12/30/2008

- GASLOG LTD GLOG 12/03/2014

Description

Summary: Standard Drilling (Oslo: SDSD) is a holding company set up by the Norwegian investor Oystein Spetalen to acquire oil supply vessels from distressed sellers in the North Sea at the bottom of the cycle. Spetalen has an outstanding record making these investments, selling near peak cycle, and returning all cash to shareholders. We think he will most likely sell SDSD for ~2x the current market cap in 1-2 years. The North Sea started recovering in early 2018, but this opportunity still exists because SDSD is overlooked: it has a ~$100mm market cap, trades ~$120k/day and is only covered by Norwegian sell-side. Even if the recovery takes longer than we expect, several Nordic peers will likely be forced sellers of vessels again. As the only player with significant net cash, SDSD would be poised to make more attractive buys. It therefore has limited downside but 2x upside.

SDSD was written up well by Barong last year, so we have kept this article to the point and included a detailed appendix. We think the stock is significantly more attractive now.

Company and Industry Overview

The Norwegian investor Oystein Spetalen has an outstanding record of buying Nordic energy assets and selling them for significant returns within 3 years. He has done this with numerous companies and has already done it twice with SDSD in the past. The company is now repeating the approach for a third time and has used the collapse of oil prices since 2014 to acquire stakes in 20 platform supply vessels in the North Sea from distressed sellers. These vessels carry cargo such as equipment and fluids to offshore oil fields, for operators like Statoil and BP. The North Sea market consists of ~130 vessels, of which ~60 are in layup after arguably the worst downturn in its history. The industry is highly cyclical and ultimately driven by confidence in future oil prices, which drive the capex of oil companies and the demand for rigs and vessels. Like other cyclical industries, many companies took on large amounts of debt to order vessels at peak cycle and have since become forced sellers. We became interested in SDSD after our industry contacts consistently and voluntarily picked it out as the one company that has been able to take advantage of this. As one source said:

“That particular company is very unique. They’ve got cash in reserve and they’ve been able to take advantage of distressed sales in the market… There are not really any companies buying vessels at the rate they are buying. They’re good quality vessels. Able to work freely in the North Sea on a range of contracts. They should make probably substantial profits for those PSVs that they bought very cheaply.”

The market is now clearly recovering:

Investment Thesis

1. Spetalen will likely sell SDSD’s vessels in 1-2 years and return cash to shareholders.

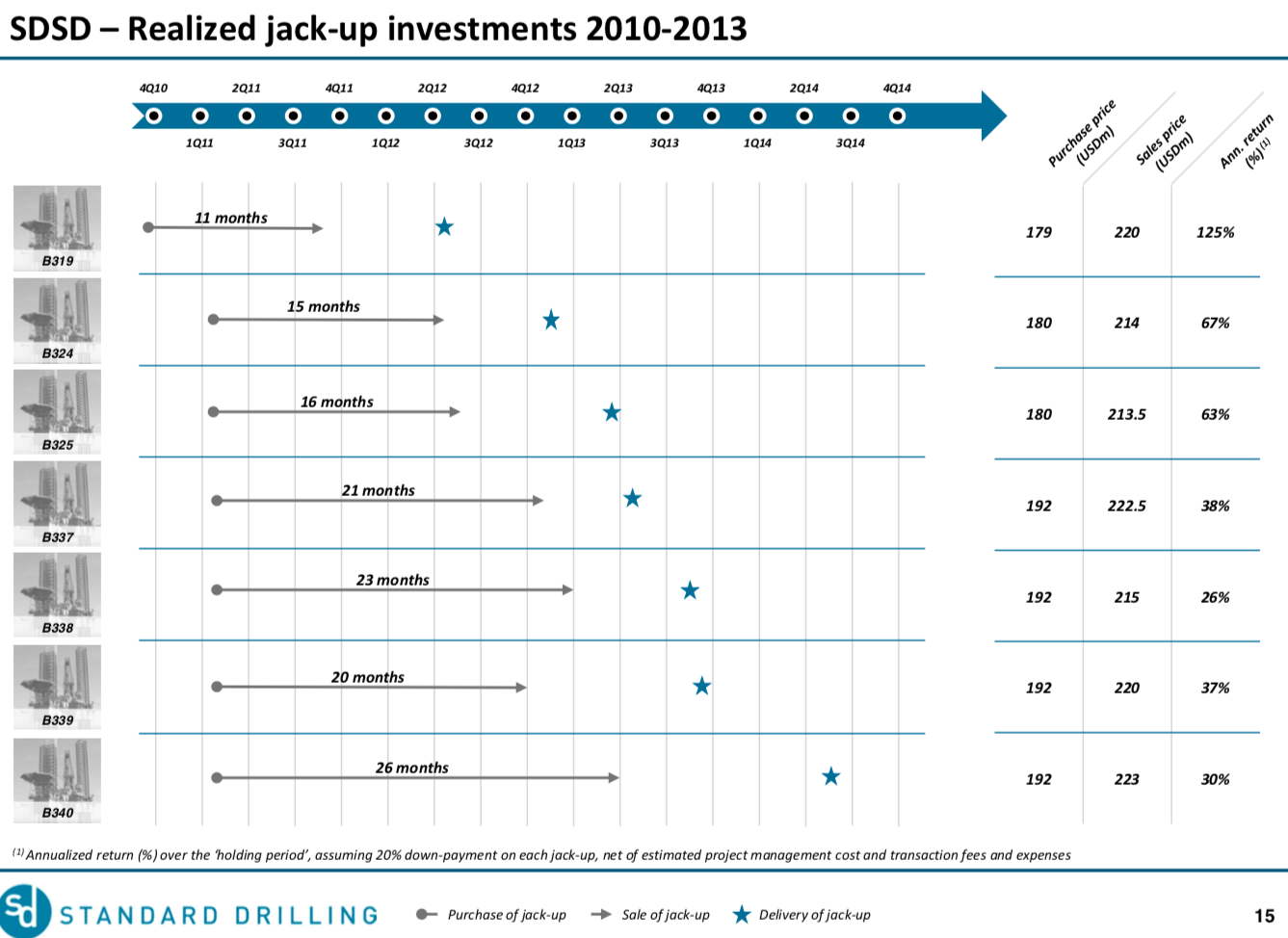

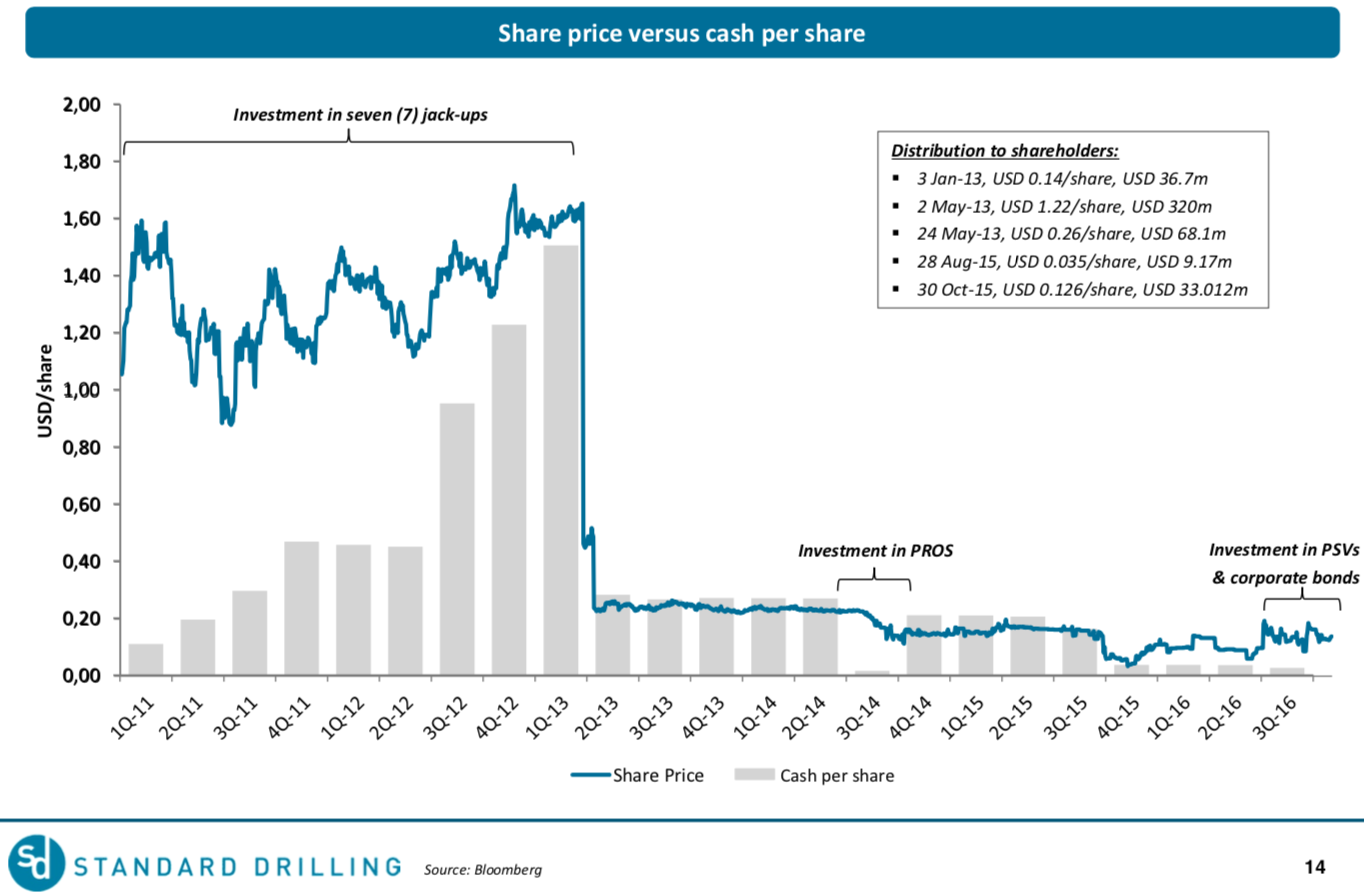

We outline a longer history of Oystein Spetalen’s energy investments in the appendix, but here focus on the two times he has already used SDSD to make investments. The first started in 2011 when the company ordered 7 rigs for down-payments of ~$260mm. All 7 rigs were sold between 2011-13 while still in construction for a profit of $222mm, or a +87% total return. SDSD then payed out $1.62/shr in dividends and the stub traded at $0.25/shr. A shareholder at SDSD’s IPO in 2011 at $1/shr would also have realized a total return of +87%. The S&P GSCI Energy Index returned +8% over the same period.

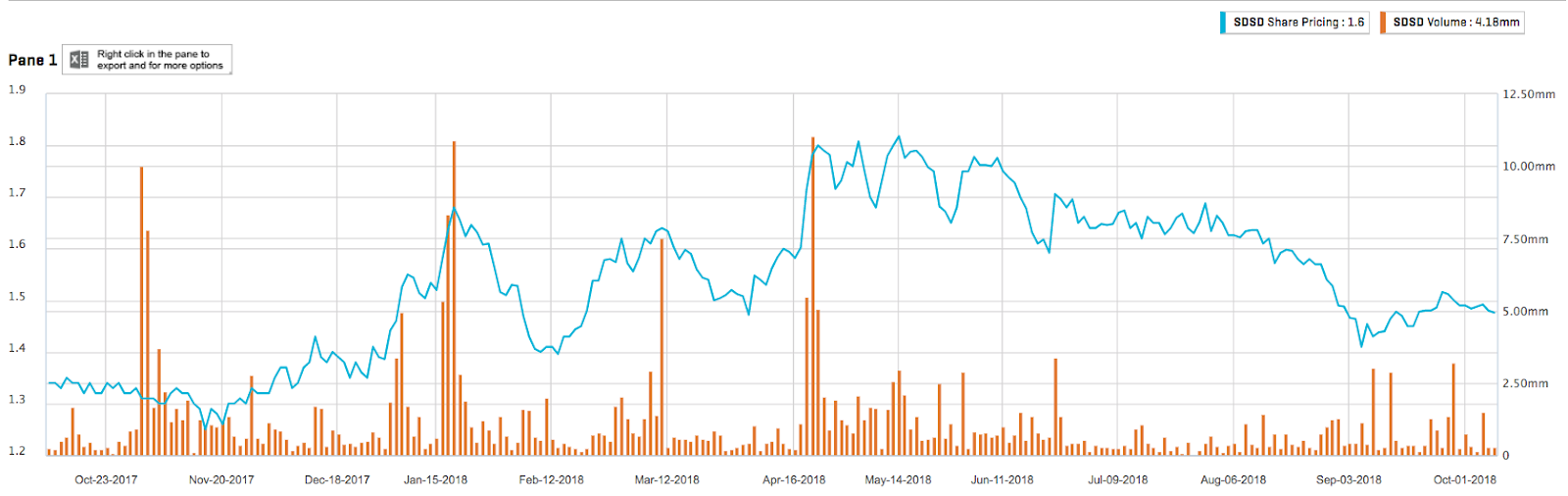

Interestingly, SDSD’s share price had fluctuated from 2011 to mid-2012 with little direction until they started selling the bulk of the rigs, which would have given investors the chance to buy in later and achieve an even better IRR. This looks to be happening again today, with the stock trading ~20% below its peak in May despite no news and Brent oil being up ~15%.

SDSD’s second act started in Sep 2014 when the company acquired a stake in the rig company Prospector Offshore Drilling for $65mm. Spetalen realized this was a mistake as the price of oil crashed and sold the stake just 2 months later for $51mm to Paragon Offshore for a loss of 21%. The S&P GSCI Energy Index fell 27% in this time, and Paragon ultimately went bust 18 months later. This episode actually enhances our view of Spetalen.

SDSD is now in its third act, and this time Spetalen has the tailwind of acquiring the assets at the very bottom of the North Sea cycle. That recovery is now well under way.

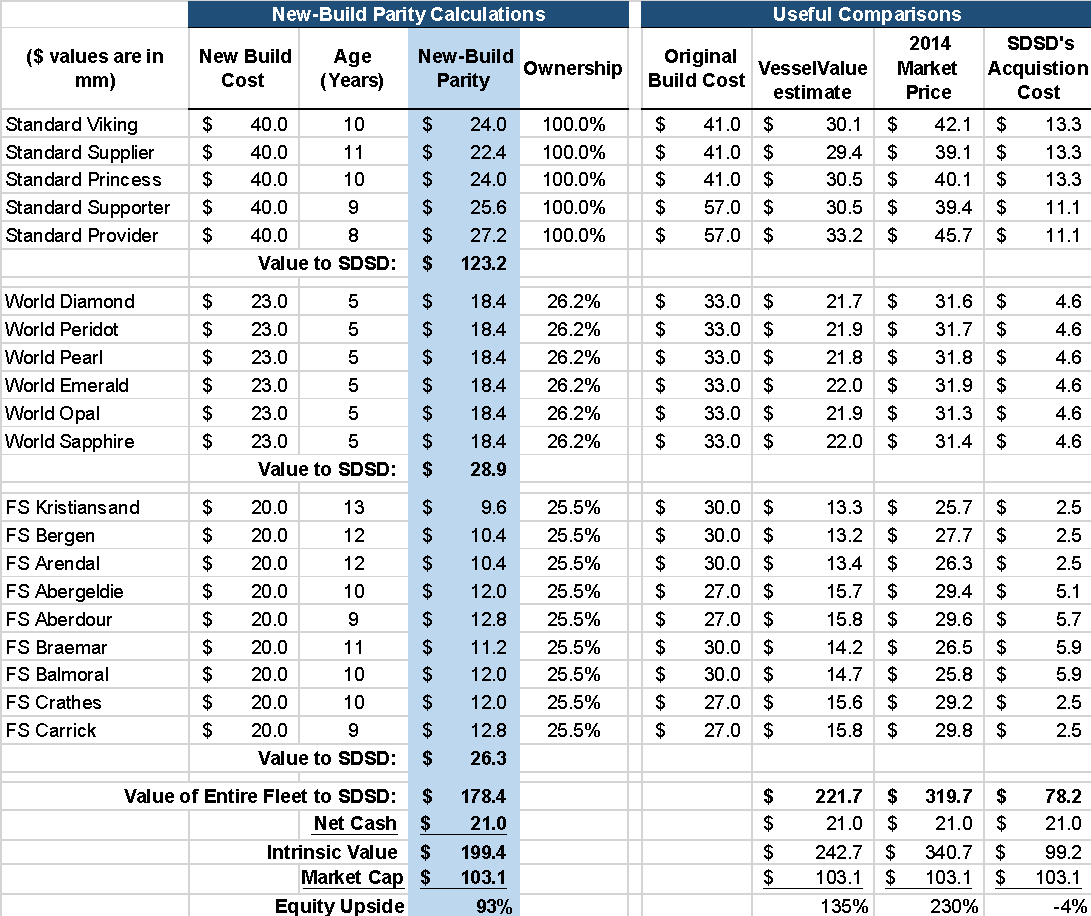

2. SDSD’s vessels are worth NOK 2.6/shr on a new-build parity basis. Adding NOK 0.3/shr of net cash gives an intrinsic value of NOK 2.9/shr and nearly 100% upside.

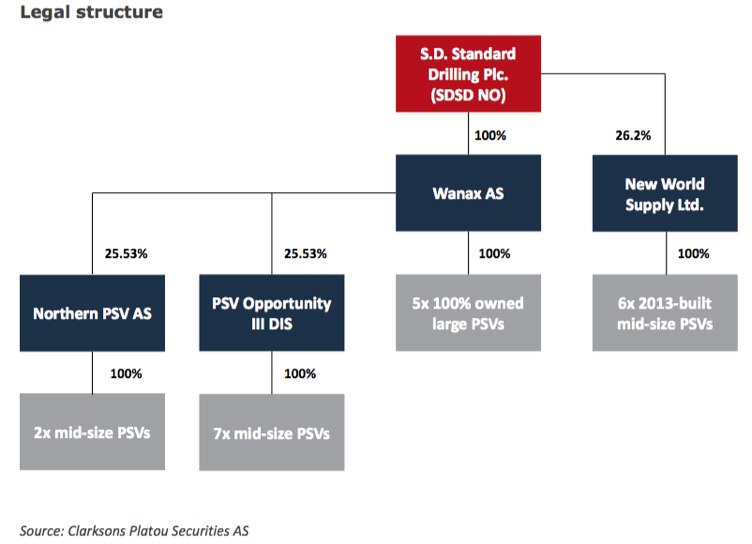

SDSD’s fleet can be split into 3 sections:

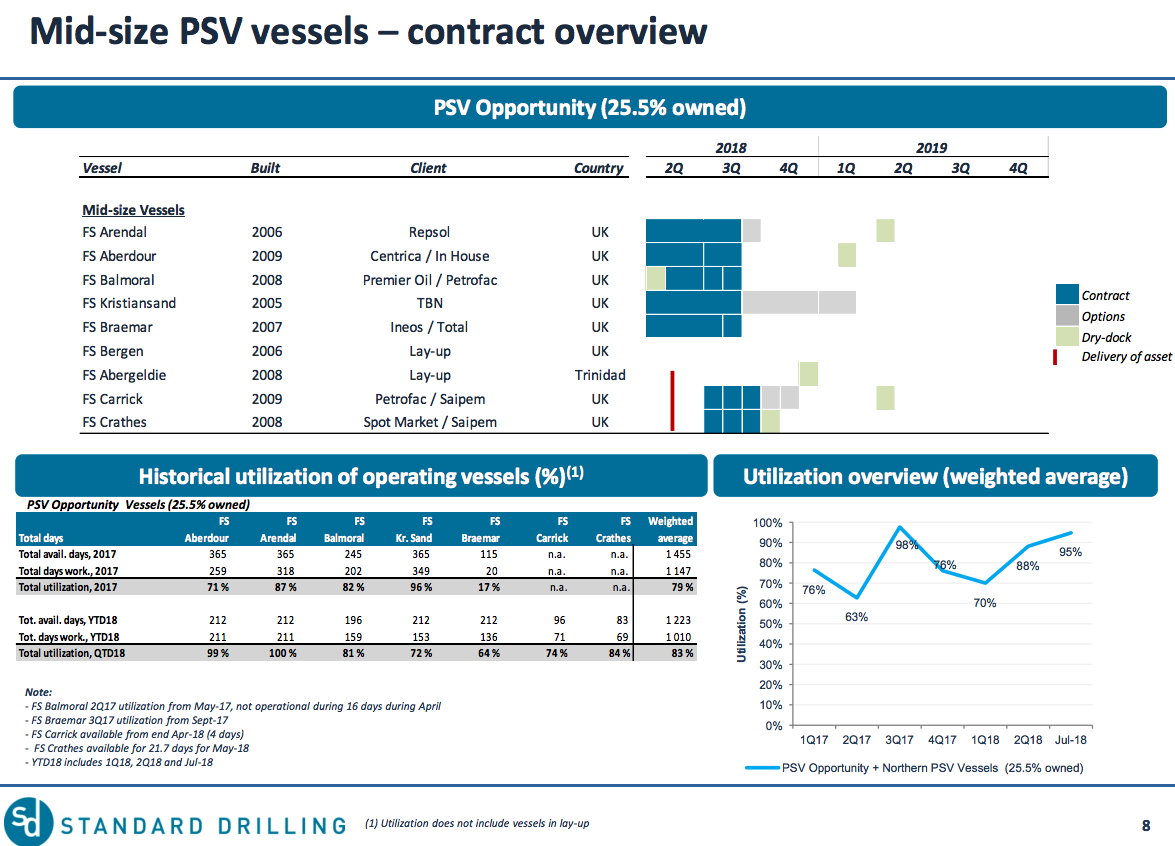

- 5x “Standard” vessels: 100% owned by SDSD. These are high-quality, large, 8-11 years old and have had near 94% utilization in 2018.

- 6x “World” vessels: 26.2% owned. Above-average quality, medium size, 5 years old, currently stacked.

- 9x “FS” vessels: 25.5% owned. Below-average quality, medium size, 9-13 years old, 83% utilization in 2018.

The industry-standard method to value these vessels is to calculate their new-build parity. This is a replacement cost that takes the estimated cost to order the vessel today and depreciates that by the age of the vessel. Having spoken with several shipyards, our calculations suggest the fleet is worth $178mm to SDSD (NOK 2.6/shr). Adding $21mm (NOK 0.3/shr) of net cash gives an intrinsic value of $199m (NOK 2.9/shr), or 93% upside. We think Spetalen will sell the company for this price as the market recovers in the next 1-2 years. For comparison, the valuations of a well-known consultant called VesselsValue suggest 135% upside. 2014 market prices suggest 230%. SDSD’s rock-bottom acquisition prices suggest only 4% downside:

3. Limited downside as stock is trading at SDSD’s acquisition costs. In fact, a slower recovery would create more forced sellers for SDSD to buy from.

As the furthest right column on the table above shows, the market is giving SDSD no premium above the cost it acquired the vessels for. Not only does this not price in the market recovery that is already taking place, our industry calls suggest that the vessels have always been worth more and that SDSD only achieved these prices because it was acquiring from forced sellers:

- ER Offshore (9 vessels) was forced into a bank sale and today has no vessels remaining.

- World Wide Supply ASA (6 vessels) had defaulted and had no vessels operating.

- Volstad Shipping (3 vessels) was forced into a bank sale and has now exited the industry.

- Island Offshore (2 vessels) had breached covenants and was restructuring.

Another downside argument is that the latest data suggests the improvement in day-rates for vessels in the North Sea has slowed because owners are bringing their vessels out of lay-up quicker than expected. Yet we think that this will be negative for SDSD’s Nordic peers but positive for SDSD itself. It means that while the destination of a balanced market hasn’t’ changed, the journey will be tougher because day-rates will recover slowly before spiking when utilizations reach ~80%. SDSD’s Nordic peer group is heavily indebted with an average of 13x ND/EBITDA, and several of them will likely be forced sellers in the next 6 months. At that point, SDSD is the obvious buyer as the only public vessel company with a significant net cash balance. SDSD’s chairman talked in Sep about more deal opportunities in Winter 2018.

We have identified 31 vessels in layup that are higher quality than many of SDSD’s existing vessels and would be suitable acquisitions (see appendix). Our new-build parity valuations above suggest that SDSD has so far acquired vessels for an average of just 43% of their replacement cost and have actually done better in their most recent acquisitions. It is tricky to quantify future acquisitions, but a crude way is to say that if SDSD continue to acquire $1 of vessel value for 44 cents, their $21mm of net cash could end up buying $48mm worth of vessels. Our bull case is that Spetalen sells SDSD in 1-2 years for the $178mm of new-build parity for current vessels + $48mm of future ones = $226mm. That represents 120% upside.

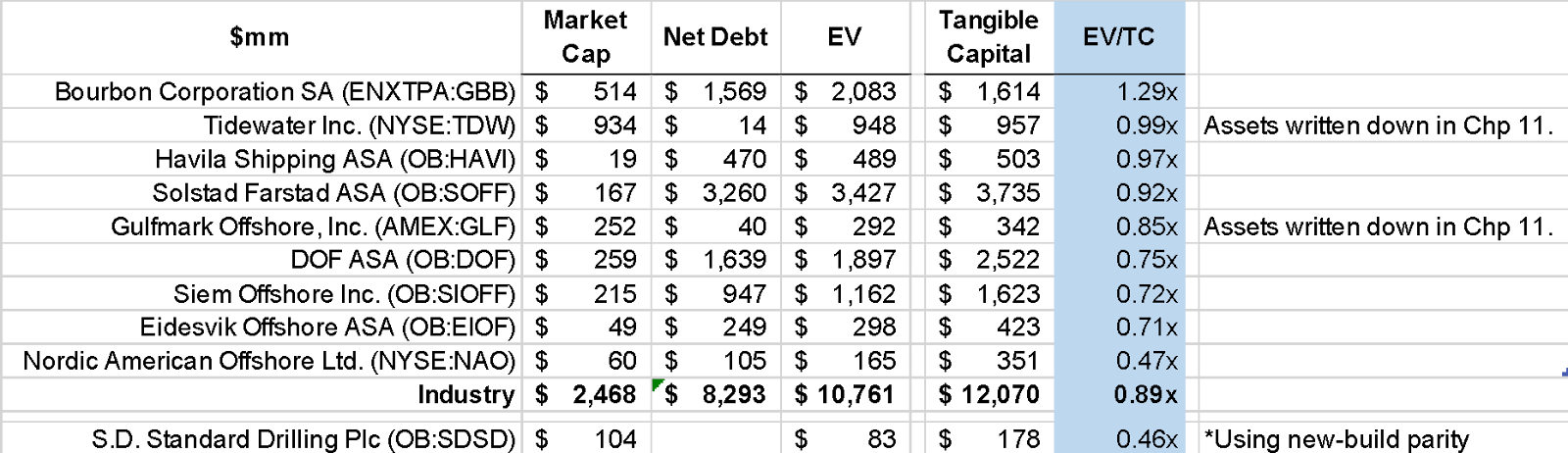

Relative Valuation vs Peers

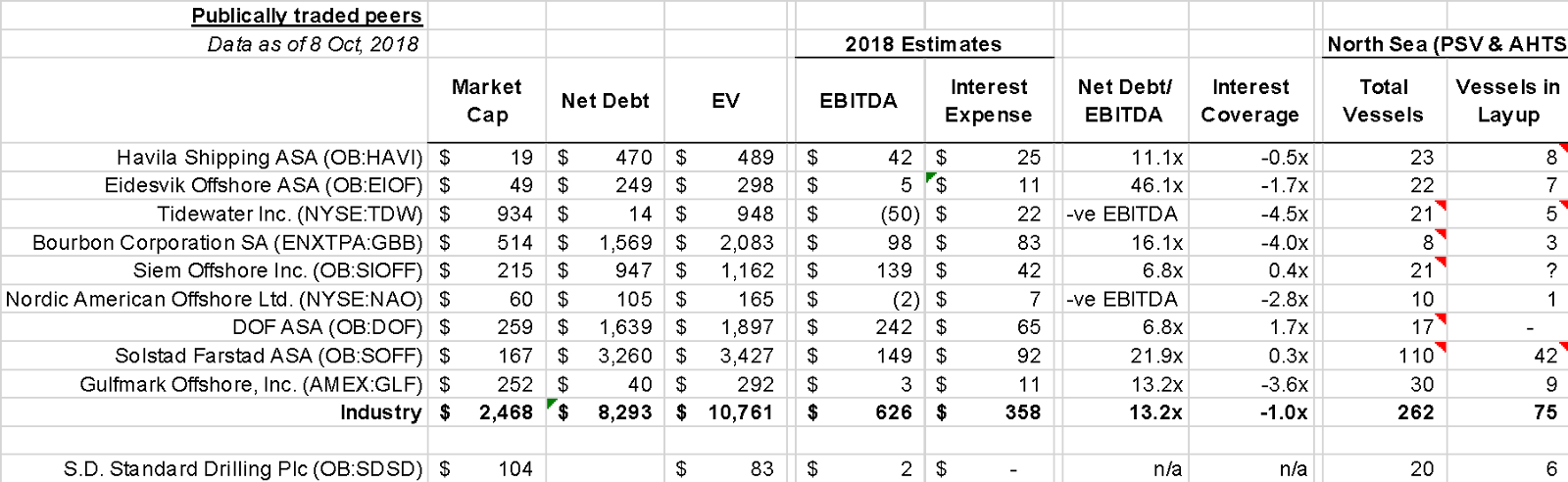

Aside from being the only public company with significant net cash, we like SDSD because it trades at nearly half the multiple of peers. We haven’t calculated new-build parity for every peer, but a good proxy is tangible book value because this typically takes the historic cost of building the vessel depreciated for age. (And will actually be generous as new-build costs today are lower than historically). Adding net debt to tangible book gives us ‘tangible capital’. On EV/TC the peer group is trading at 0.89x versus 0.46x on our new-build parity for SDSD. Historically, these businesses tend to trade at 1x during mid-cycle and above/below during peak/trough cycle. Other than SDSD, we like the US peers TDW and particularly GLF. Both have both been through Chp 11, have limited debt, and had assets heavily written down so their new-build values are significantly higher than tangible capital. (Both have been written up on VIC in the last 12 months)

Key Risks

1. We do not attempt to predict oil prices and instead value assets at today’s prices and require a large margin of safety. Nevertheless, oil falling to $40-50 would require significantly more vessels to be scrapped before the market rebalances. While most of SDSD’s value lies in above-average quality vessels which would not be scrapped, they would continue to depreciate at ~7% a year. A ‘grizzly bear’ scenario where oil were to settle in the $30-40s much of North Sea drilling would become unsustainable. Assuming SDSD’s “World” and “FS” vessels would be worthless and that the high quality “Standard” vessels would only be worth 80% of SDSD’s acquisition cost gives an intrinsic value of $71mm and 32% downside.

2. Management execution. While Spetalen has an excellent record, SDSD could issue equity to acquire. Given the stock’s discount to intrinsic value this could destroy value. SDSD is also just one of several investment vehicles controlled by Spetalen, and so is not his only focus.

-------------------

APPENDICES

------------------

Oystein Spetalen

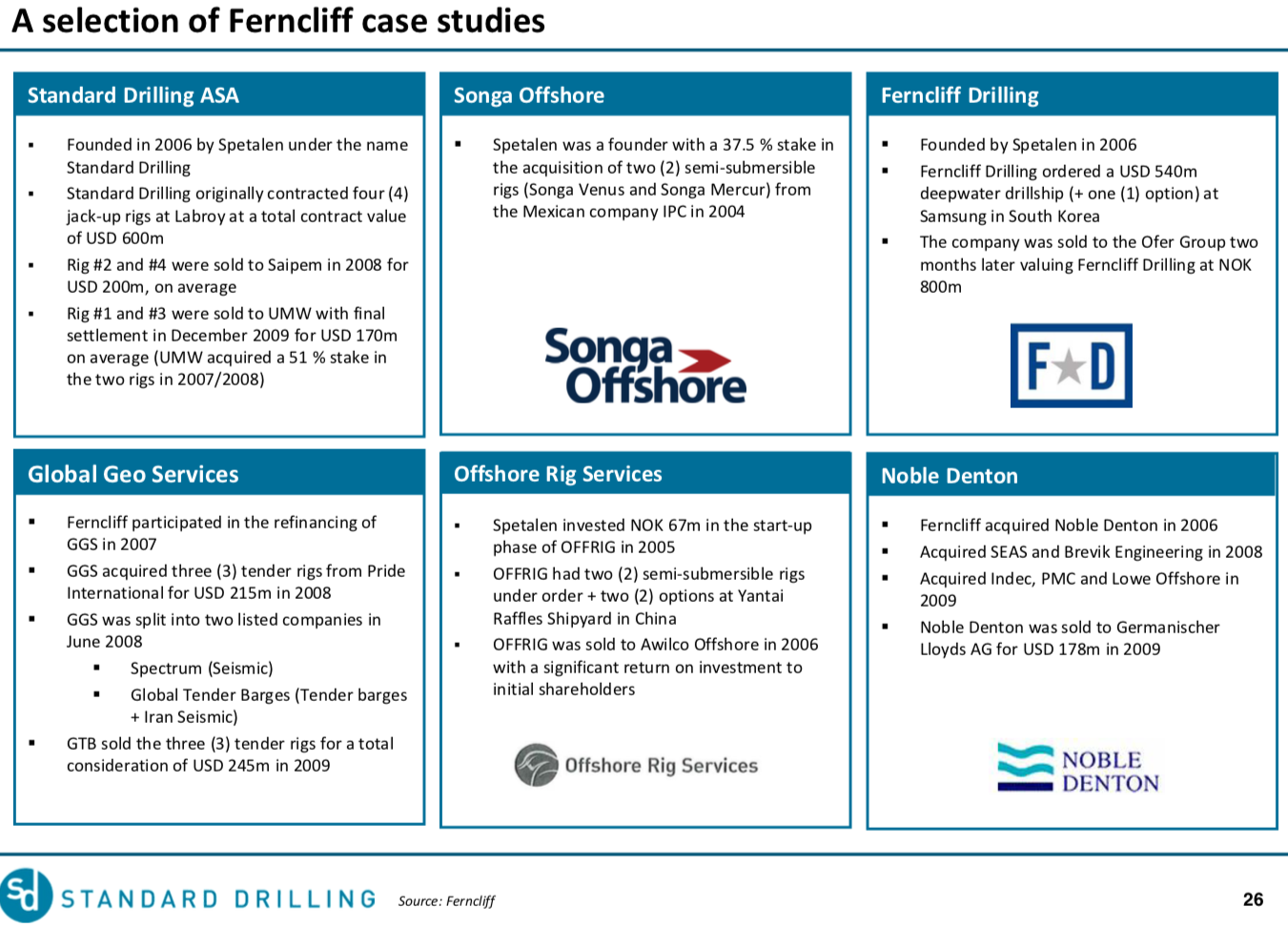

Norwegian investor Oystein Spetalen is the key driver behind the company. He owns several investment vehicles including the Ferncliff group, a private investment fund that has been most active in the Norwegian energy space but has also made investments across TMT, property, and healthcare. Spetalen and Ferncliff together own most of Saga Tankers ASA, which owns ~20% of SDSD’s stock. Spetalen installed Martin Nes as the current chairman, who is the CEO of Ferncliff and also installed as the chairman of Saga Tankers. He owns 2.2mm shares. Spetalen also installed Arne Fredly from Apollo Asset Ltd as an independent director. Fredly is an independent Norwegian investor and has a history of working with Spetalen. Fredly owns 5% of SDSD through Apollo and has stakes in several Spetalen companies. The rest of the company is comprised of a General Manager, CFO, and independent director. Management of the vessels is outsourced to Fletcher Shipping.

In additional to SDSD, Spetalen has an outstanding investment record:

SDSD itself was founded in 2010 by Spetalen, Glen Ole Rodland and Gunnar Hvammen to own and finance 1 jack-up rig to be constructed at the Keppel FELS yard in Singapore. The company raised $372mm in 2010-11 and used this to acquired a further 6 rig contracts, taking the total to 7. These were then sold between 2011-13 and the proceeds paid out in dividends:

Unit Economics/How these businesses make money

The PSV business model is simple: companies order vessels from ship builders typically years in advance of delivery, and lease them to oil companies typically on contracts of 3-12 months. There is also a spot market that is used particularly often when demand for vessels for a long period is low (like now). While the opex of hiring a captain and crew tend to be relatively fixed, the day rates paid by oil companies tends to vary greatly over the course of a cycle:

Utilization of vessels is also very important. This can be as high as 90% for the industry at peak cycle, and 30% at trough cycle as ships get put into lay-up.

Ships usually last for ~25 years. Vessel values are typically determined by the cost and depreciation as they age, but the cyclicality of the industry typically means that companies end up ordering vessels at the top of the cycle, and so vessels often earn lower than normal FCFs in their initial years which means that their PV ends up being below the cost of construction.

An example of the cash flows over remaining life of one of the “Standard” vessels:

The North Sea PSV Market

The North Sea has been a market for offshore oil for nearly a century. Numerous oil companies operate in the region, most notably the majors like Statoil, BP, and Shell, but also many others. The PSV market also consists of many players are barriers to entry are extremely low: it is easy to rent a boat and hire and captain and crew. The biggest players tend to be Norwegian or US companies. On the Norwegian side, these include Solstad/Farstad/Deep Sea Supply (recently merged), DOF, Havila, Eidesvik and many others. On the US side these include Tidewater, Hornbeck, Gulfmark, and SEACOR Marine.

There are ~130 PSVs in the market, of which ~60 are currently in layup. More vessels could come from other markets if conditions improve. The live status of all vessels can be tracked at http://westshore.no/, with live locations at https://theseabay.com/Client/Home#.

All of our sources stated that the current downturn in the North Sea has been worse than 2008, and potentially the worst ever. This has been because (1) the oil price did not recover quickly, (2) companies made large vessel orders right at the top of the cycle, and (3) most/all companies entered the downturn highly levered. As a result, almost all companies have been through some form of bankruptcy or restructuring.

As one oil company said, the North Sea had a “near death experience”. Much of the kit was near it’s end of life. Operating efficiency was awful with lots of downtime and high labor costs. As a result, there were significant redundancies, and this was the bulk of the cost cutting. The businesses have become more efficient with automation and using technology. They think this is structural. The change in prices with service providers is more likely to be cyclical.

As costs fall and oil prices soaring, it is clear that the cycle has turned. As one source said:

“If oil can stay at $60-90 then oil companies will have the confidence to invest in projects so activity will probably be high and the demand for boats will be higher and everything should improve.”

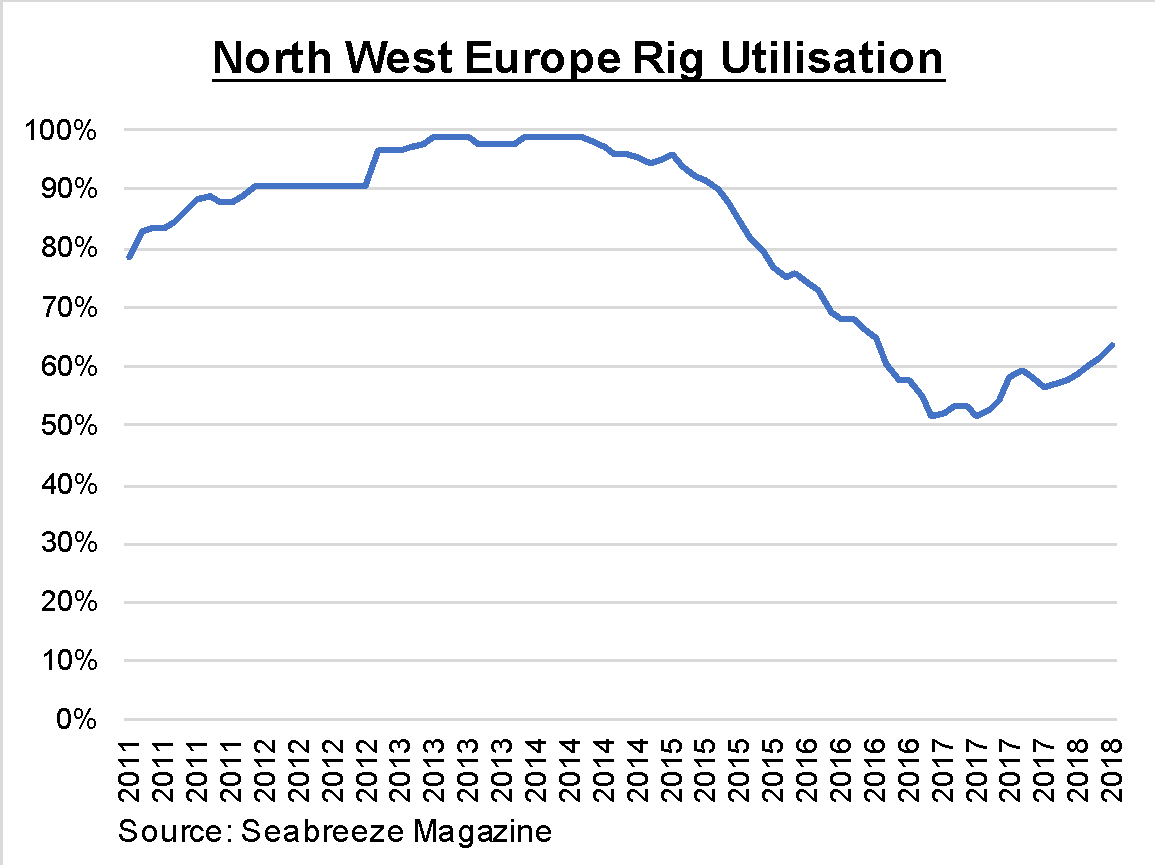

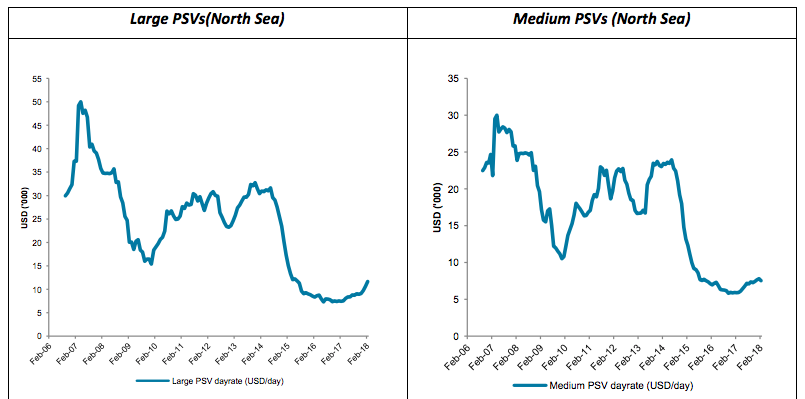

The number of PSV tenders is up ~35% y/y, and the number of rigs is already rising, with utilization up 11% y/y and now at 64%:

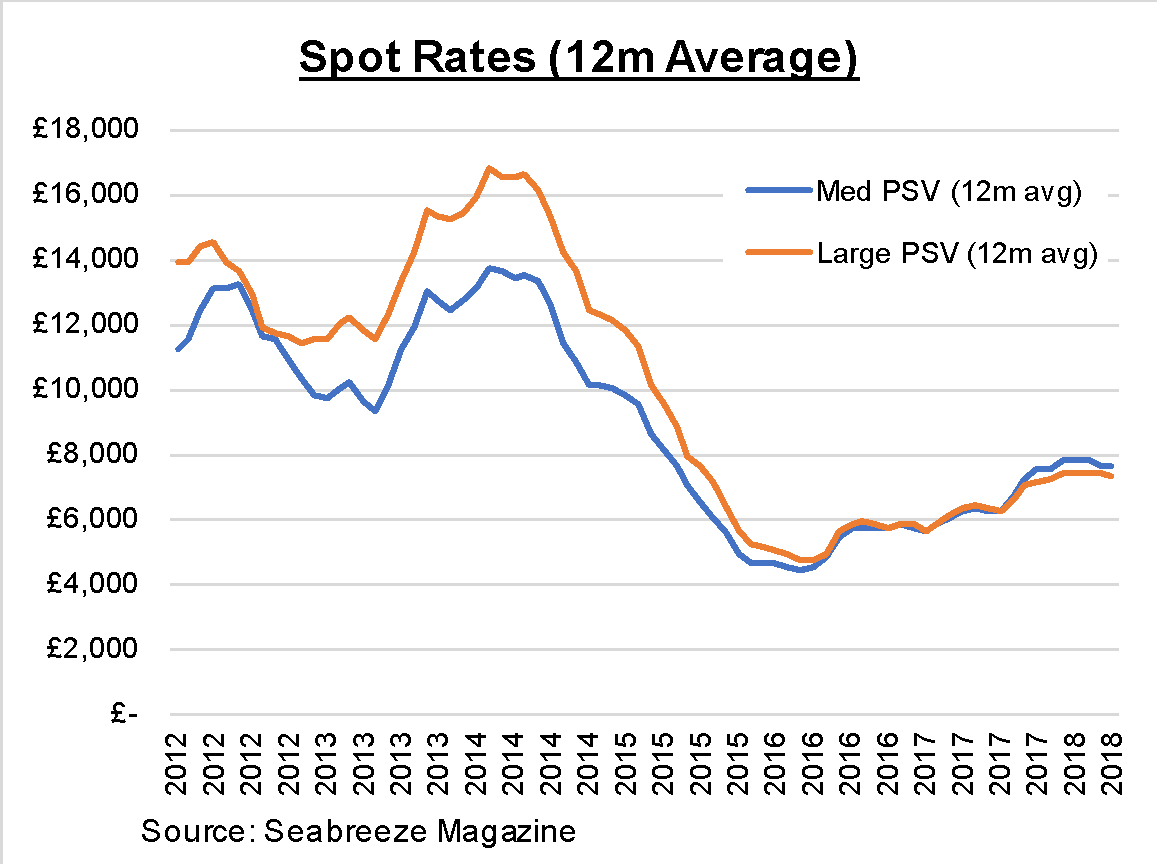

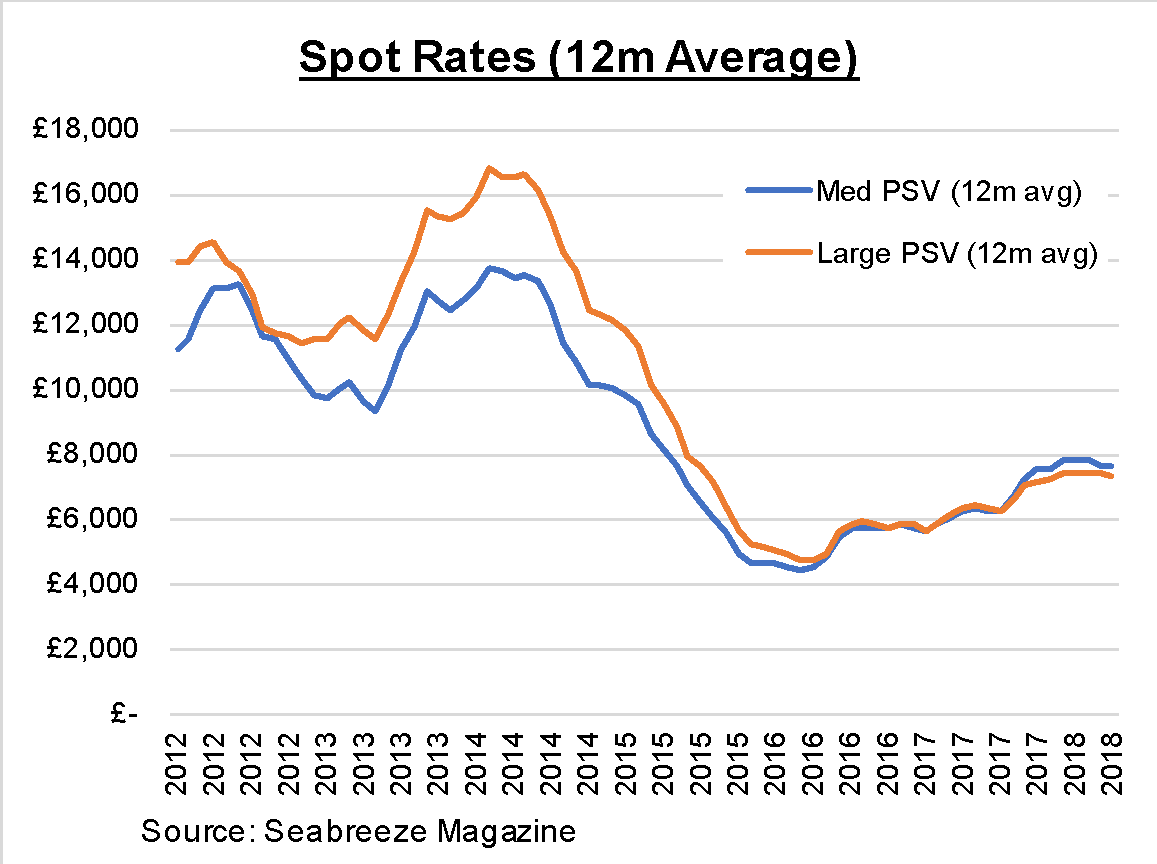

Day rates for vessels are already rising (left chart), but have historically inflected upwards at 75% utilization (right), suggested this is likely to be reached in 1 years’ time:

Source: SDSD’s April 2018 equity issuance docs

Shipbrokers all agree that prices are rising and but there is a range of opinion as to how quickly it will rise. The general consensus on prices today is that they are already around £10k. One said we will probably not get back to £13k in the next 2-3 years and that this would need oil at $100. Clarkson's 18 April 2018 report says that large PSVs are getting $15.5-18.5k for summer 2018. However, another shipbroker told us that day rates may not need to go back to £13k because costs have come down.

A key source of speculation is how many ships in layup will come back to the market. The supply vessel companies say that only 40-50% will, whereas the shipbrokers estimate that 70-80% will. The vessels that will struggle to come back are the older and smaller ones. There are two main reasons for this: First, given the oversupply of boats oil companies can be picky in the ones they choose. Second, as offshore drilling moves increasingly to deeper and harsher waters, higher quality boats are required. Boats over 10 years old are unlikely to come back. As one oil company told us, they are not looking for the lowest price on day-rate drilling - they want the best quality with very low downtime.

As the market turns, so too does the value of the vessels. However, given the number of vessels in layup it is unlikely that the increased theoretical value of the vessels can be realized through asset sales. Instead, they will be realized through higher earnings power. As one source said: “who wants to spend $10mm on a boat in a rubbish market that is trading at a loss?”. In other words, you can’t practically sell them at this point in the cycle for their ‘intrinsic value’.

SDSD’s Fleet

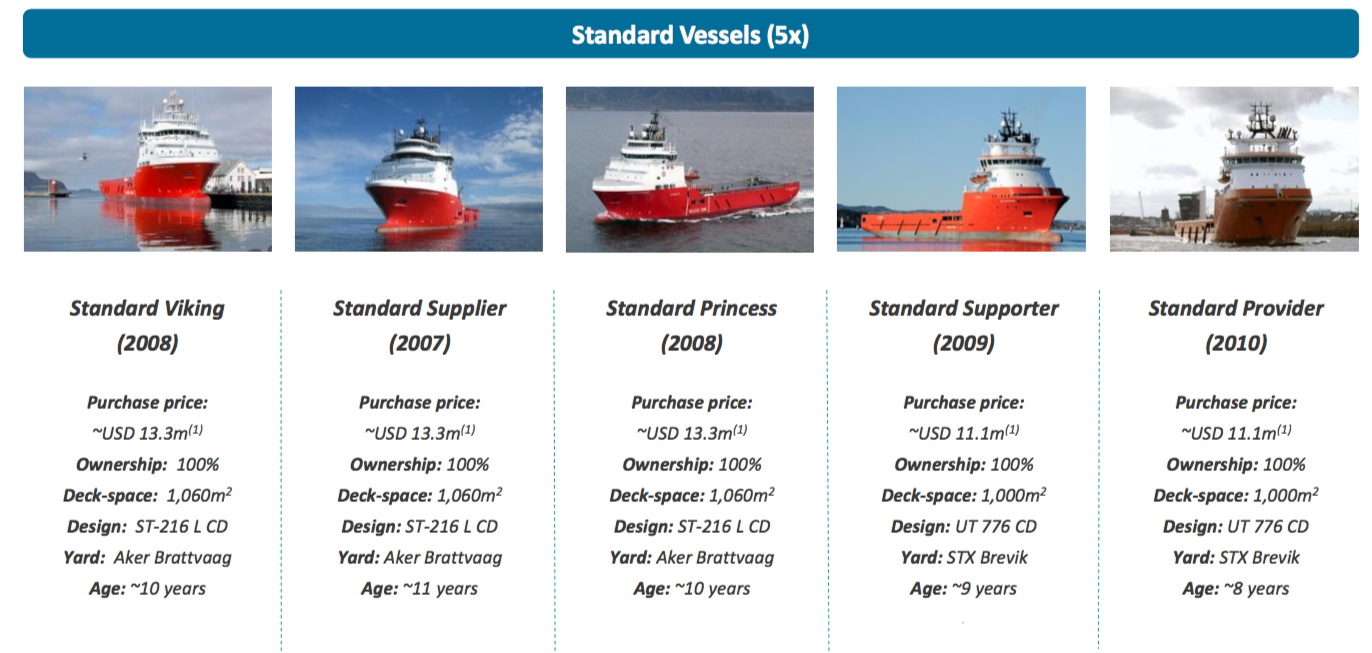

Large vessels

SDSD acquired 5 very large PSVs which are now the core of the company through two transactions in 2017. In January 2017, SDSD bought 3 PSVs from Volstad Shipping for a total price of $40m. These vessels cost ~$41m each to build. In October, the company further acquired 2 very large PSVs from defunct German owner ER Offshore for $11.1m each that originally cost $57m to build. All 5 vessels are amongst the most advanced in the world, which was confirmed through my primary research calls.

Source: Company presentation

These vessels have been highly utilized throughout this downturn:

Source: Company presentation

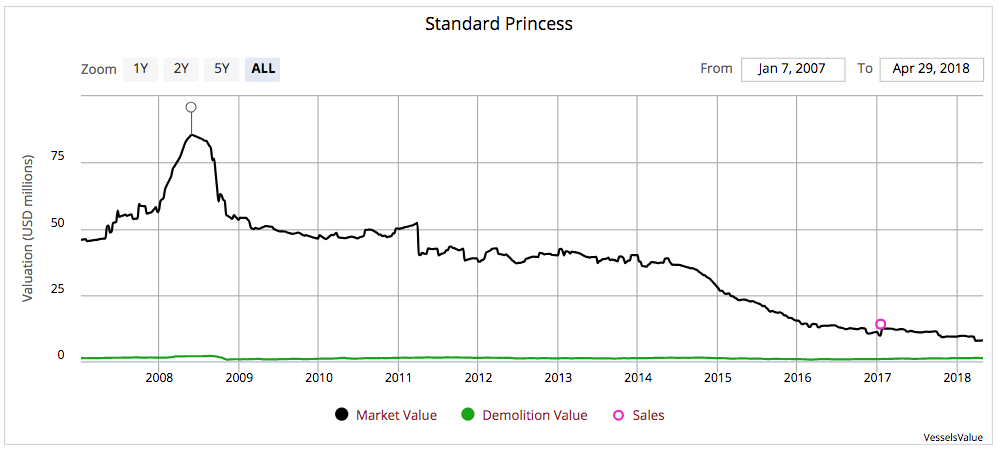

The market value of these vessels over time:

Source: VesselsValue

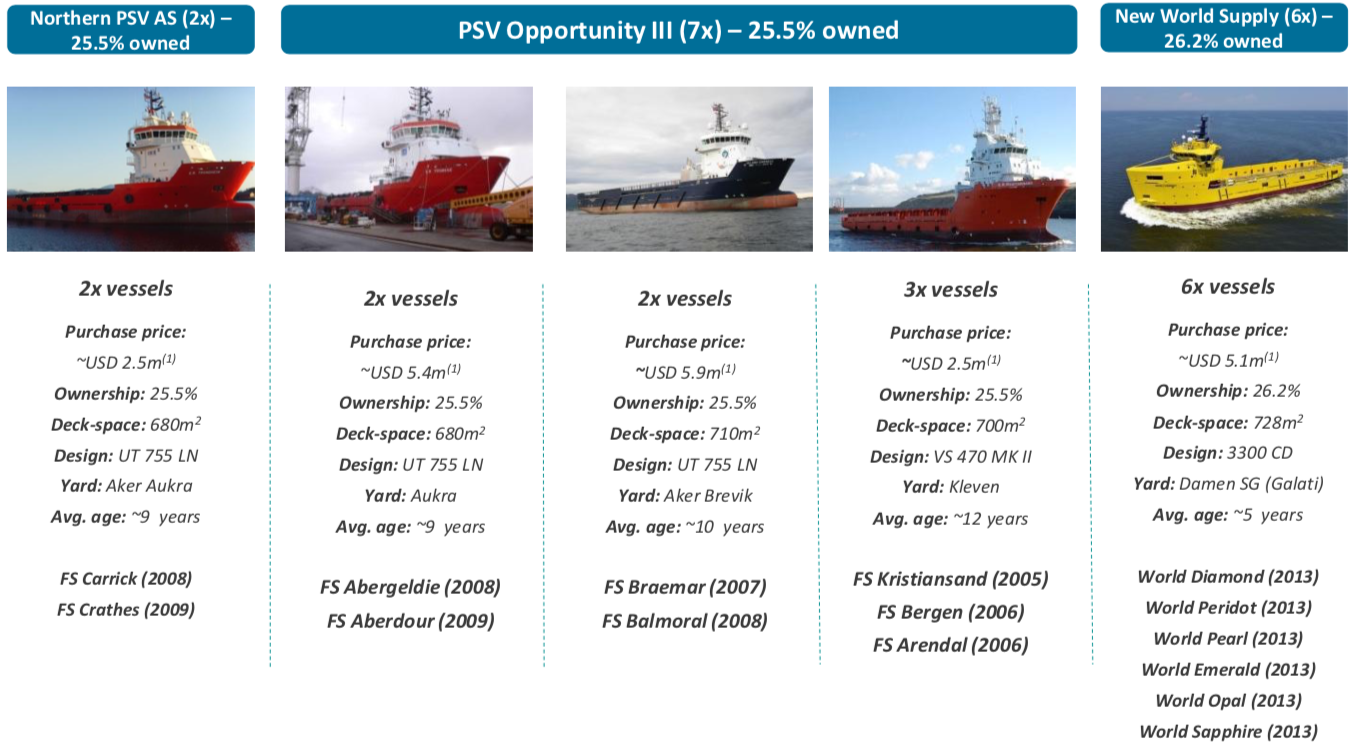

Medium sized vessels

Source: Company presentation

Source: Company presentation

All 6 “World” vessels are currently in layup and are not controlled by SDSD. US multi-billion and multi-strategy hedge fund QVT Financial owns the 73.8% and SDSD 26.2%.

World Emerald and World Sapphire can be found on Tschudi Ship Management’s website: http://www.tschudioffshore.com/page/915/Fleet_List

World Diamond, Perdiot, Pearl and Opal can be found on Remoy Management’s website at: https://remoy-management.no/fleet/offshore-service-vessels.

Distressed sellers

All of SDSD’s vessels were acquired from distressed sellers:

ER Offshore (9 vessels)

Private company that is very difficult to find information about, but they no longer have any ships listed on their website: https://www.er-offshore.com/en/fleet.php

Sources say that they went from ~12 ships to 0. Were forced into sales by German banks.

World Wide Supply ASA (6 vessels)

World Wide Supply (WWS) was a Cayman company. They took on debt to order 6 vessels at the top of the market cycle. These vessels entered long-term contracts with Petrobras in Brazil that were subsequently cancelled in 2016. They then moved to the North Sea to trade on the spot market briefly. By August 2016 (when SDSD acquired its first stake), all 6 vessels were in layup and the company had breached its covenants and defaulted on part of its debt. It had NOK 1257mm of debt, NOK 82mm of unpaid interest and NOK 93mm in additional annual interest. The company was in default by the time of its last public report in Q2 2016.

SDSD acquired first lien bonds in the company in October and November 2016 and in January 2017 all the debt in the company was converted into the equity of a new company called New World Supply Ltd. New World Supply today has no debt. SDSD owns 26.2% of the equity and a US multi-strategy and multi-billion dollar hedge fund called QVT Financial owns the other 73.8%. QVT was founded and is run by Dan Gold. Gold was a trader at Deutsche Bank before founding QVT in 2010, and has since 2010 has also served as a non-executive director on the board of a UK drilling rig company called Awilco Drilling, which QVT has also invested in.

Volstad Shipping (3 vessels)

Was forced into a bank sale and has now exited the industry.

Island Offshore (2 vessels)

Island had also breached covenants and had to sell vessels to raise cash in their restructuring. The CFO of Island told us that:

“The sale of the Express & Earl was definitely influenced by the fact that we have been through a debt restructuring, but the main reason was that we are of the opinion that there will be a significant over-supply of PSV’s in the market in the short to medium term. As a consequence we found it beneficial to dispose of the two oldest and smallest PSV’s in our fleet. In our opinion the PSV’s of UT755 design is “outdated” in the advanced parts of the OSV market - and thus we want to concentrate on larger and slightly more advanced vessels. SDSD paid the going market price at the point in time when they purchased the vessels - whether this is to be considered a “good” or a “fair” deal is up to the eyes looking I guess. It was a historically low price - but I think also that UT755’s has been sold at even lower prices after the purchase of the Express & Earl was concluded.”

M&A Value

SDSD has made 13 acquisitions since 2016 months, all from distressed sellers. Industry sources expect several major restructurings to take place in 2018/19 as debt levels are still extremely high for all publicly listed peers except Tidewater and Gulfmark, which are both US companies and went through Chapter 11. The industry has an interest coverage of -1.0x and Net Debt/EBITDA of 13.2x.

The publicly traded peers alone have 75 vessels in layup, which are the most likely vessels to get sold. This figure includes both PSVs and Anchor Handlers (another type of vessel that companies owning PSVs also typically own). Focusing just on the PSV market and including private peers, shipbrokers show that there are a total of 67 PSVs currently in layup in the North Sea, which demonstrates there are indeed plenty of additional acquisition targets. Of these, 31 vessels are likely to be better quality (larger deck size, younger) than SDSD’s existing World Supply vessels and so be the types of vessels that SDSD will go for:

Source: http://westshore.no/

As examples of why some of these vessels are realistic acquisition targets: (i) 4 of these vessels are owned by Island Offshore, which SDSD has already acquired 2 vessels from as a result of their need to restructure debt. (ii) 2 of these vessels are owned by Bourbon, which is expected to make -$340mm EBIT in 2018 on an EV of $2.1bn and has already stated they want to sell PSVs in a ‘strategic’ shift.

SDSD’s commentary on acquisitions (from a May article on Tradewinds): SD Standard Drilling chairman Martin Nes. “We would like to increase the fleet but by buying at the right price for us, as buyers — and that’s not so easy now because you see that the market has moved a bit," Nes said. "You see that the rates in the North Sea, where we operate, have increased quite a lot actually from the rock bottom back in January 2017.

Company Structure

SDSD has effective control of the vessels in its stakes in Northern PSV AS and PSV Opportunity III due to the fact that Norwegian DIS structures typically have a ‘trigger clause’ of 15% ownership. This ‘trigger clause’ means that other shareholders have to sell or buy out SDSD at the equivalent price of any offer from a third party to buy the vessels. The vessels are also managed by Fletcher Shipping, which SDSD outsources it’s operations to. SDSD does not have control over the 6 vessels owned by New World Supply. These are operated by Tschudi Ship Management and Remoy Management.

Management of Ships is Outsourced

Management of ships is outsourced primarily to Fletcher Shipping, who receive a management fee per day per vessel in operation and compensation for the vessels hired. No fees are accrued for vessels in layup. Fletcher was established in 2007 and is responsible for seeking and negotiating employment for the vessels in addition to the daily running of the vessels either in lay-up or when on charter. Fletcher provides commercial, technical, and corporate services, including vessel maintenance, crewing, purchasing, shipyard supervision, insurance and financial service in addition to being responsible for the equipment used for the vessels’ safe operation. See more at: https://www.fletcher-group.com/about-us

Remøy Management is the manager for the vessels World Diamond, World Perdiot, World Pearl and World Opal. The four vessels are currently in layup in Ålesund, Norway. The Vessels World Emerald and World Sapphire are managed by Tschudi Ship Management. The two vessels are currently in layup in Cadiz, Spain. Tschudi Ship Management is located in Estonia and is a wholly owned subsidiary of the Tschudi Shipping Company.

Stock Price Chart

Financials

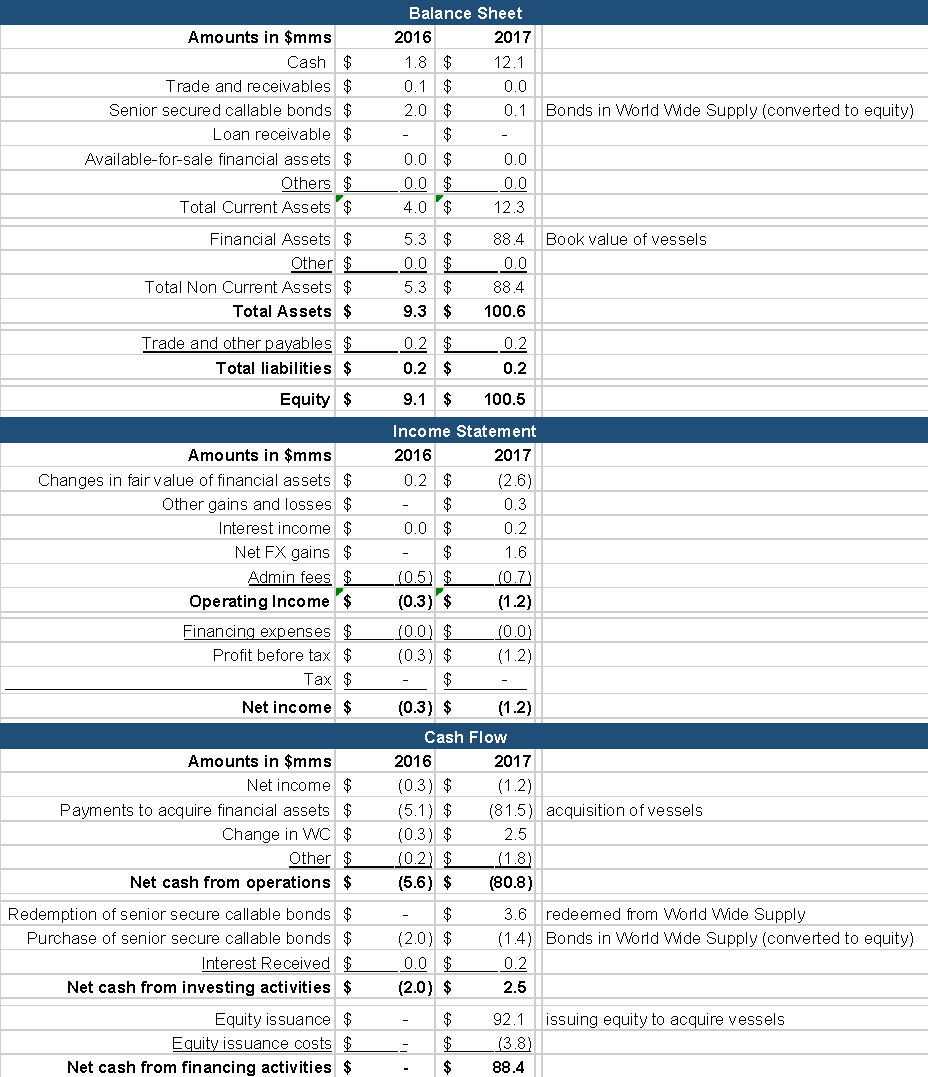

Note: historic financials are not particularly useful given that most of the vessels were only acquired recently and are equity investments rather than operated by SDSD. The most important item is the book value of the vessels on the balance sheet. These were listed at $88.4mm at the end of 2017, and revised up to $91.9mm at Q1 2018. The book value is the average of valuations from two independent valuers. The valuers consider these to be distressed values, and calculate it by estimating fair market value for today and applying a discount. If SDSD had reported the estimated fair market value rather than distressed market value, the book value of the vessels at the end of Q1 would have been $131.6mm rather than $91.9mm. Taking this $131.6mm and adding the $21mm of net cash at the end of Q1 would give SDSD an intrinsic value of $152.6mm. The current market cap $103mm.

I and/or others I advise do not hold a material investment in the issuer's securities.

Catalyst

- Spetalen selling the company or individual vessels

- Recovering North Sea market, particularly day-rates for vessels

| show sort by |