| 2024 | 2025 | ||||||

| Price: | 8.47 | EPS | 0 | 0 | |||

| Shares Out. (in M): | 270 | P/E | 0 | 0 | |||

| Market Cap (in $M): | 2,287 | P/FCF | 0 | 0 | |||

| Net Debt (in $M): | 2,485 | EBIT | 0 | 0 | |||

| TEV (in $M): | 4,772 | TEV/EBIT | 0 | 0 | |||

Sign up for free guest access to view investment idea with a 45 days delay.

Description

Overview:

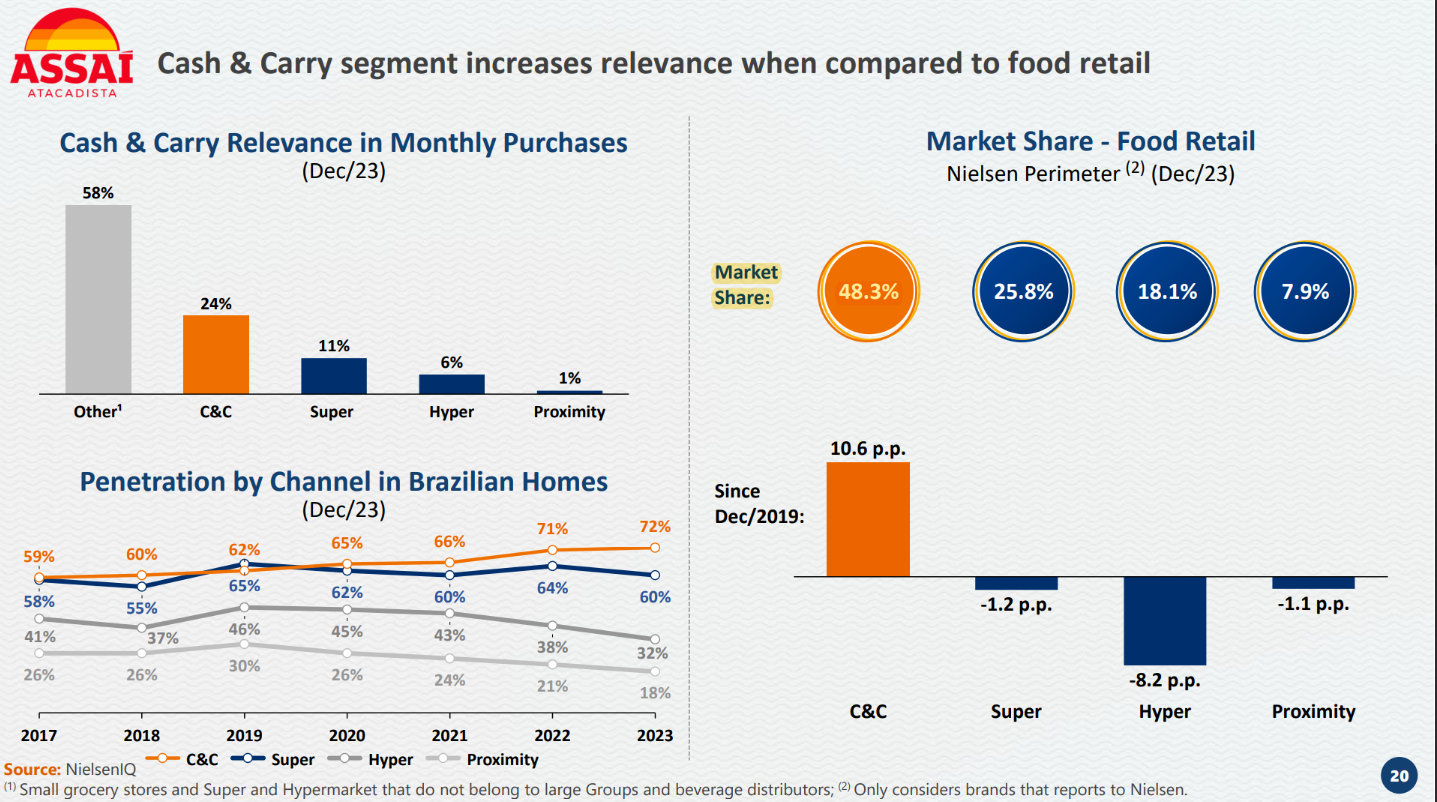

Assai Atacadista is the second largest operator of cash and carry stores (i.e. wholesale grocery) in Brazil with 293 locations. The company was formerly a subsidiary of GPA, a large Latam supermarket operator controlled by Casino Group, but separated into a standalone company to go public in March 2021 at $15.13 per share. Casino Group has since fully exited its 40.90% ownership. Both the cash and carry format, and Assai’s dominance in the market have grown exponentially over the last decade. Since 2011, the group has increased its unit count by 5x and increased its gross sales by nearly 20x, or a ~27% revenue CAGR in Reais (~16% USD CAGR). Today, Assai has an~11% market share of the R$700 billion Brazilian food retail market, and a 30% market share of the cash and carry segment. Atacadao, owned by Carrefour, is the largest cash and carry operator in Brazil with a 35% market share.

Extra Hiper Acquisition:

In October 2021, Assai announced that it had reached an agreement to acquire ~70 Extra Hiper hypermarkets from GPA for R$4.0 billion. This was a highly material transaction. Assai had previously completed >20 hypermarket conversions as a subsidiary of GPA, and it felt it had a strong grasp on the economics of a cash and carry conversion. These ~70 stores collectively produced R$ 8.7 billion in sales, and the company’s track record of conversions indicated a ~3x uplift in gross sales, and adj. EBITDA margins that are 25% higher than a typical Assai store given the locations are generally in more densely populated areas. The group budgeted R$ 45 million per store in capex for the conversion, so all in approximately R$ 7.2 billion in capex for post conversion economics of R$ 25 billion in sales and R$ 1.9 billion in adj. EBITDA. This is both highly attractive in absolute terms, and compared to the unit economics of a new Assai store that cost R$ 70 million to build and ramps to R$ 270 million in sales with R$ 16 million in adj. EBITDA. Assai expected that a conversion unit would reach maturity by the end of year 2, whereas greenfield units require 5 years to mature.

This conversion project created a very elevated period of capex, and while the group incurred a significant amount of leverage up front, the growth in EBITDA is just beginning to flow through. Today, the hypermarket conversion project is finished, and the cohort of 47 conversions that were completed in 2022 are now in their second year of maturing. These stores are currently operating at a monthly sales run rate of R$ 26 million, which is a 2.6x increase from pre-conversion. In addition, they are operating in line with the company average adj. EBITDA margin of 5.5%. As these units continue to mature, as well as the 17 conversions that occurred in 2023 and the ~60 greenfield Assai stores built over the last 3 years, the group should benefit from significant embedded growth. Consider that over the last 3 years Assai has spent nearly R$ 11 billion to build ~120 stores. On a run rate basis, assuming a normalized growth of 20 stores per year, capex inclusive of maintenance capex should be at a level of R$ 1.5-2.0 billion per annum, or roughly half the level of the last 3 years.

Growth / Unit Economics:

As touched on briefly above, Assai has grown with highly attractive unit economics. The average Assai store costs R$ 70 million to build, and ramps to $R 270 million in sales with R$ 16 million in EBITDA, or a pretax ROIC in excess of 20%. Moreover, while Assai already holds 30% market share of the cash and carry market, there is still significant room for growth. Consider that there are 91 cities in Brazil in excess of 150K in population that do not yet have an Assai store. In addition, Atacadao, which is currently at 371 locations, is still planning to grow by 15+ units per year and plans to reach 470 units in time. This growth is supported by the growing adoption of the cash and carry format, which has risen to the top for consumers as the format of choice given that prices are often ~15% cheaper than a supermarket. Beyond that, there are 2,000+ existing smaller cash and carry stores throughout Brazil where Assai and Atacadao are likely to continue outcompeting and gaining share as they have significant relative procurement advantages.

Management Incentives:

Assai has been led by Belmiro Gomes since 2011. Prior to joining Assai, Belmiro was the commercial director at Atacadao for 22 years. Given that Assai was a subsidiary of GPA, the company had a long way to come in aligning its executives, which were long tenured but owned very little shares, with that of the new shareholders. On that front, earlier this year Assai passed a management compensation scheme which I believe is highly attractive, and gives shareholders a good sense of management’s own internal views on the growth potential of Assai. The program was granted to the CEO, as well as the two VPs of Operations and Commercial & Logistics, who had been with the company for more than 12 years each. The program consisted of a one off share grant of up to 2% of the outstanding common stock. 0.4% of the grant is for executive retention, of which 30% vests over 5 years, and the remaining 70% vests in 7 years. 1.6% of the grant is performance based, where the executives only begin receiving shares if EPS grows at a minimum of inflation + 20% p.a., and they receive ~14bps for each 1% CAGR in excess of the minimum threshold. In other words, to receive the maxim of 1.6% performance shares, Assai must compound EPS at nearly 40% p.a. (IPCA + 20% p.a. + 12%).

Valuation:

Assai is trading at a highly attractive valuation on today’s run rate metrics, and is exceptionally attractive when considering how economics are likely to evolve over the coming three years.

FY2024

Gross Revenue R$ 85,000

Net Revenue R$ 77,350

EBITDA R$ 4,254

Interest Cost (R$ 1,750)

Mtn CAPEX (R$ 600)

Tax (R$ 665)

FCF R$ 1,238

Thus, against the current $2.3bn USD market cap, Assai currently generates ~$225m USD in FCF, or nearly a 10% yield using very conservative assumptions. For instance management estimates that maintenance capex per unit is ~R$ 1m and I assume double that above.

Here is what economics could look like in 3-4 years time given the maturation of the ~120 recently built units, including conversions, normalization of organic grow rates, and utilization of excess FCF to pay down debt

FY2027

Gross Revenue R$ 119,500

Net Revenue R$ 108,745

EBITDA R$ 6,524

Interest Cost (R$ 1,350)

Mtn CAPEX (R$ 740)

Tax (R$ 1,551)

FCF R$ 2,882

It of course depends on how exchange rates evolve over this time, but at prevailing rates I believe there is a clear path to reaching a ~20% FCF yield in the next several years with significant growth remaining thereafter. This also implies that Assai reaches < 2x net debt to EBITDA by 2027.

Risks:

Beyond operating in Brazil, the primary risk here is that the business is quite levered. As part of the spinoff, GPA gave Assai the generous gift of assuming ~R$ 9 billion in debt. Then to add to this, the leverage incurred for the Extra Hiper acquisition and conversion project has brought Assai to ~R$15 billion in gross debt. While high, I believe this is very manageable given the embedded economic growth from maturing stores. If the company needed to stop building new organic units, it could start chipping away 10-15% of its debt load each year fairly quickly.

I and/or others I advise do not hold a material investment in the issuer's securities.

Catalyst

- deleveraging

| show sort by |

| # | AUTHOR DATE SUBJECT |

|---|---|

| 8 | |

Different sector and different era, but IOT is giving me major FIO vibes with the aggressive insider selling and promotional narrative around what is essentially a commoditized core offering. FIO was the public darling of the flash memory space at a time when they were the "pure play" and a lot of the competitors that ended up eating their lunch were private or divisions of large flash memory companies. They had an awesome sales and marketing organization but no ability to build a real moat, and a hyper promotional management team that ignored competition and live in an imagined reality on investor calls. That was a lumpy whale driven business, so different. In this business, IOT loses the whale RFPs (Amazon, USPS to Geotab, FedEx recently to Motive https://www.linkedin.com/posts/motive-inc_we-are-proud-to-announce-fedex-freight-as-activity-7234991679009615872-vMRz/). I respect that these guys built Meraki but that was a very different sector. There are so many red flags here and I think we know how the story will end. | |

| 7 | |

What is the 5-10 year terminal value of the business when OEM integration / autonomous really strikes? The downtick in net retention this quarter shows the market is tough enough competing against other aftermarket players. Really struggling to see how the stock can work higher intraquarter before addressing the Q4 guide and 2026, which we do not believe management has room to walk up.

| |

| 6 | |

The quarter was pretty clean, but the beat and raise by 3.5% was not much greater than last quarter's 3.1% despite a lot of hype intraquarter. $1m of ACV from AirTags is ho hum. Net dollar retention also dipped to 117% from 119% likely reflecting some of the churn we picked up on in our checks. New sales activity remains very healthy though, and likely benefitted from the customer and analyst event in late June. Still, this is a rapid implied decel (22% growth in Q4) and FCF margin in H1 was ~5% despite all the stock based compensation. So it's barely a rule of 40 company now and will be not even close soon yet sells at 15x revs. Motive is putting on a hurt on these guys, as is Geotab, and they are both building healthier businesses (we think).

| |

| 5 | |

The sell side has been very bulled up on Samsara since its analyst day in June. The sell side is very excited about the ruggedized AirTag product and several analysts are triangulating a significant revenue beat based on app download activity as a proxy for new customer installs. Conversely, we are more excited about the short than when we wrote it up given news of several high and low profile customer defections or RFP losses and more confirmatory checks as to market saturation and an inevitable growth deceleration. We will see which view wins out in the short term tonight (we expect to hear a whole lot of AirTag hype), but in the long-term feeling comfortable whether or not this quarter shows cracks in the facade. | |

| 4 | |

Really clean post integration results from Powerfleet / AIOT this morning. Despite our bearishness on the sector taking a top down view, the long thesis here has real credibility and if they can keep taking Samsara accounts as they did with IMC Logistics, this will be a great pair trade. | |

| 3 | |

Appreciate that liverpool. PWFL (which upgraded its ticker to AIOT yday) could be a very attractive long and I've been spending a lot of time on it lately. At these prices the fact that MIXT was fundamentally undervalued and undermanaged gives you a nice margin of safety if the team can execute. You can paint a picture of a $10+ stock if things go right. Obviously integrating a company with significant South African, Israeli and US operations is not a layup, and the macro could be more of a headwind than is appreciated for core PWFL. Competitive landscape also is tough but PWFL benefits from playing in niche markets that others are not chasing as aggressively. It's actually a very good sign to me that management is not targeting aggressive top line growth and is focusing more on margins. As far as topline goes, the fact that Samsara is decel'ing while spending 50% on S&M should be a cautionary signal that PWFL is not going to magically accelerate to a double digit grower overnight. I'm not yet long PWFL but working on it and would definitely own it if I felt I needed a bit of a hedge on this market performing better than I expect. No doubt there is some value to the single pane of glass vision Samsara portrays. I believe they will struggle to be best in breed in the adjacent markets. For example, in site surveillance, there are some really strong, well run and profitable competitors with incumbency. Some of these markets like the ruggedized airtag are POC phase and probably years away from material revenue if they ever get there. In fleet, Samsara delivers a nice holistic solution, but it's ultimately a commodity and they don't have any durable moats. The installed base has stickiness as you note but any company with reasonably mature processes is issuing periodic RFPs and managing vendors. It's a pain to retrofit but to get refreshed hardware and save 20% on MRR you would probably do it. One of the issues here like with any commodity market is that while the headline ROI delivered from implementing the technology is really good, that is the case for all the vendors so you can't manifest that customer ROI into an attractive margin structure as easily as one would think.

| |

| 2 | |

Interesting write-up, no doubt they shouldn’t be trading at their current valuation. Thoughts on them only selling their whole service offering as opposed to peers that let companies mix and match different needs with different providers. I’m also looking into PWFL as a long and seems pretty undervalued especially given strong revenue retention characteristics of the business. I guess the business has a moat due to the pain of equipping a fleet with completely new telematics equipment and associates software but the valuation is still very unreasonable IMO. Thoughts on PWFL as a long? | |

| 1 | |

https://investors.samsara.com/events-and-presentations/samsara-investor-day-2024/ Recommend watching. Samsara's two reference customers largely highlight commoditized features offered by all major telematics vendors. The Airtag product launch is also a big red flag for a "SaaS" company. The fact that Samsara continues to try to pivot to new / adjacent markets that are going to be even more capital intensive with long paybacks is a red flag and a tell on the tapped-out growth in its existing fleet telematics market. | |