| 2019 | 2020 | ||||||

| Price: | 22.30 | EPS | 0 | 0 | |||

| Shares Out. (in M): | 2,559 | P/E | 0 | 0 | |||

| Market Cap (in $M): | 7,294 | P/FCF | 0 | 0 | |||

| Net Debt (in $M): | 182 | EBIT | 0 | 0 | |||

| TEV (in $M): | 7,476 | TEV/EBIT | 0 | 0 | |||

Sign up for free guest access to view investment idea with a 45 days delay.

Description

Prada 1913 HK

Summary: We think an investment in Prada (HK: 1913) offers an attractive opportunity to invest behind an enduring brand at a price that offers a compelling risk/reward as a result of the false start in its turnaround over the last year that has frustrated investors and led to very low expectations. We see 50% upside in a base case scenario with potential for more if the turnaround gains more momentum.

|

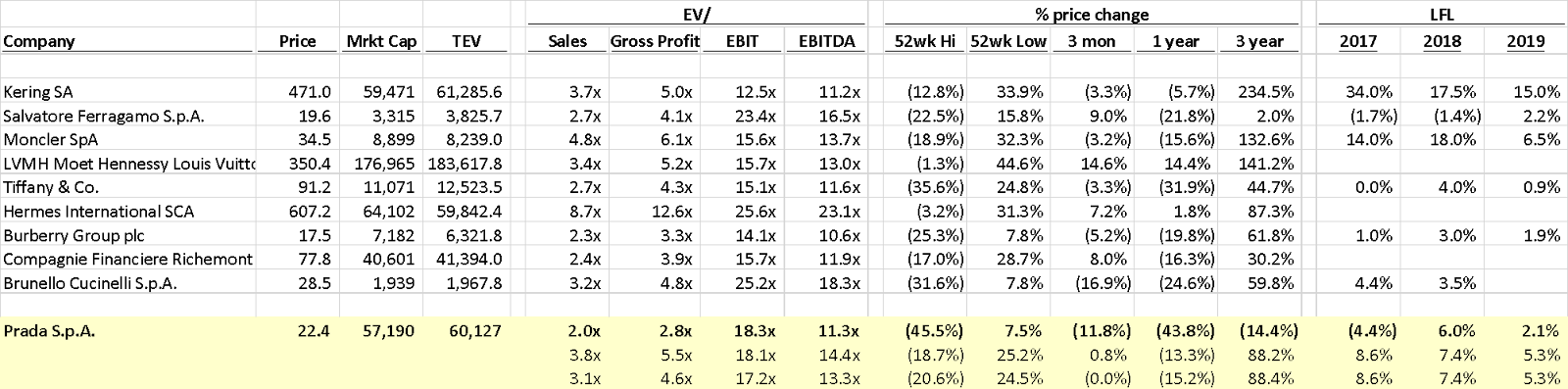

Comparable Companies |

|

|

Background: Prada was founded in 1913 and has been viewed as one of the world’s top luxury brands alongside Gucci, and Louis Vuitton. The Prada brand accounts for 80% of Prada Group’s sales and with the remaining 20% generated by MiuMiu, Car Shoe, and Car Shoe. Prada listed in Hong Kong in 2011. The Prada Family maintains 80% ownership in the company and full control with only 20% in free float.

The company’s plan after its IPO was to de-emphasize its entry price offer to increase average sale price in an attempt to move upmarket and compete directly with LV, Chanel and Hermes. The execution was poor however, and the move up market failed, causing Prada’s business to contract and significantly underperform peers. Additionally, Prada raced to shift distribution to retail in line with luxury peers, which has led to significant capital expenditures and resulting depreciation. The impact has been significant. Prada’s EBIT to fall from over 900mn euros in 2013 to just over 300mn in 2018. Shares of Prada have declined 60% from its post-IPO highs, underperforming nearly all-listed luxury goods peers over that timeframe. Prada unveiled a transformation program in 2017 to turn the business around focused on investing in digital, reducing wholesale distribution, and optimizing pricing and assortment.

This turnaround plan showed some promise in early 2018. Like for like growth improved to high single digits, driving operating leverage in the business. Investors took notice and shares increased to the upper 30s/low 40s. However, after reporting weaker than expected results for the second half and announcing additional investments, shares have fallen to new lows. Management called out a weaker macro and protests in France, but a poor marketing strategy that was called out as racist likely also compounded problems (https://www.washingtonpost.com/arts-entertainment/2018/12/15/seriously-prada-what-were-you-thinking-why-fashion-industry-keeps-bumbling-into-racist-imagery/?utm_term=.7d1eed7df3b3). Further pressure has been added during the quarter when Prada announced a plan in late May to exit lower quality wholesale doors, which will likely further pressure near term sales and profitability. Prada stock now trades at 2x forward revenues, which is a discount to all other luxury goods peers (ex-Hermes which trades at a significant premium to the sector) of 3.1x and Burberry / Ferragamo at 2.4x. Prada sales mix drives relatively high gross profit margins, driving an even wider gap with peers on an EV/gross profit basis: Prada currently has a discount of 40% below luxury goods peers ex-RMS and 25% below Ferragamo and Burberry.

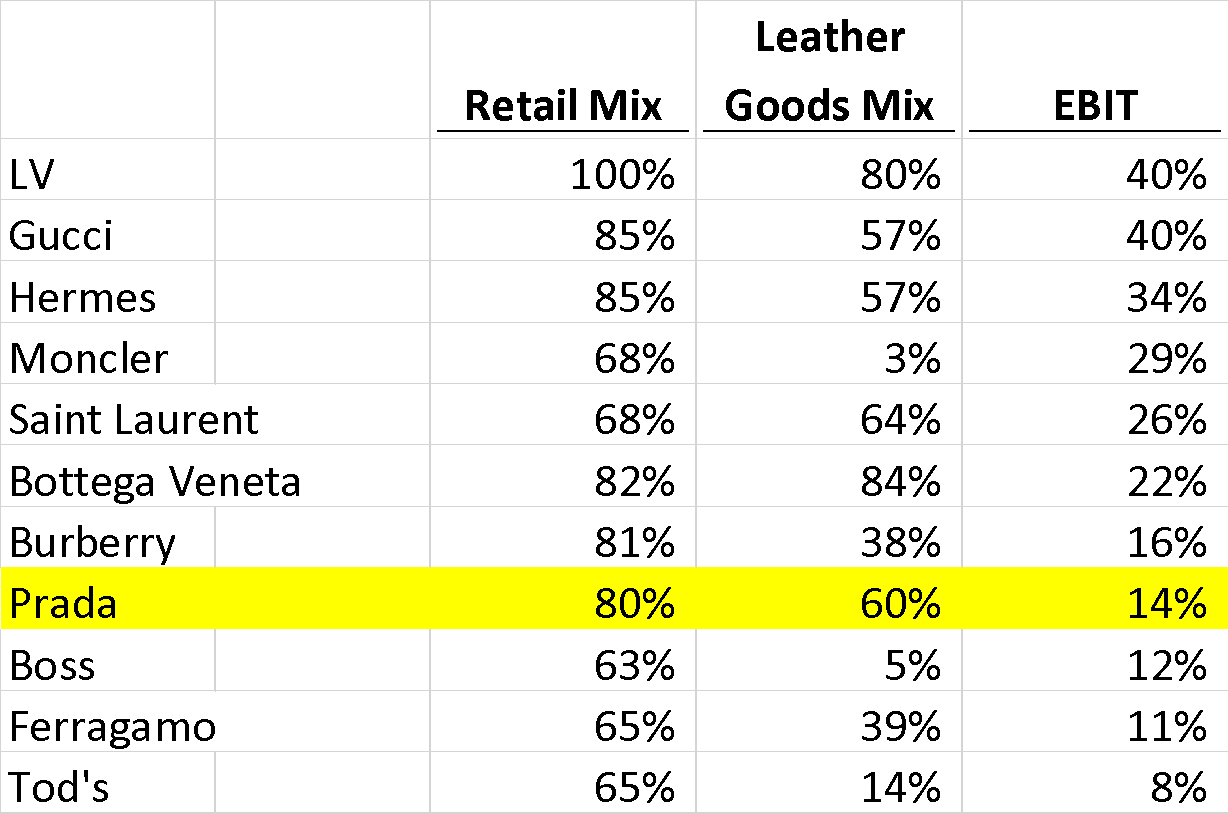

Thesis: We believe the Prada has not impaired its brand equity and is making the right changes to improve performance. Recent brand building initiatives drive near term margin compression but support Prada’s brand equity and will result in the reacceleration of growth in 2020. As growth improves, Prada’s operating margin should approach 20% in line with peers with similar leather goods mix, distribution mix, and scale.

1. Enduring brand benefiting from growth in global wealth, and status signaling

Prada has built its brand over the last century. The brand is positioned firmly in the luxury category with less mass relevance / exposure than some other luxury stocks (Burberry, Ferragamo, etc.) that are used as peers. We believe luxury goods, particularly handbags, are attractive investments because of status signaling and long product lifecycles – iconic designs like Prada’s Galleria, Hermes Birkin, Gucci’s Bamboo were all designed decades ago. These products driven the majority of gross profit dollars and are augmented by new products that drive a halo around the brand.

The market for luxury accessories has enjoyed a 9% CAGR since 2008 principally driven by China but ultimately supported by Global GDP growth. We believe that as developing markets continue to develop, other markets will continue to drive luxury spending. Younger demographics are driving the spending growth, Bain reported that Gen Y/Z now comprise 47% of luxury good consumers and 33% of sales.

2. Turnaround plan launched in 2017 has focused on the right issues

We believe Prada is making the right changes to support long term brand equity, drive growth, and improve profitability. Prada has made transformative changes across its entire business, including product, channel strategy, and customer engagement.

Products: increased accessibility and tapping into the millennial consumer demographic.

-

Prada has launched several new leather handbag lines focused on the 1,200-2,000 price point, where Prada under indexed in its move upmarket

-

Brought back Nylon products, which were discontinued in 2010 due to their price points, which are lower than Prada’s leather goods

-

Re-launched its athletic wear sub-brand, Linea Rossa in September 2018

-

Expanded its shoe offering to include sneakers, which have been strong sellers amongst luxury peers

-

Launching exclusive capsules to increase newness and better segmenting products

Distribution: Improving quality of channel partners, which will cause near term pain but supports brand longer term, and expanding presence in ecommerce

-

Rationalizing its wholesale network to remove lower quality partners. Wholesale is currently 18% of revenues, and the rationalization is focused on Italian and European wholesale partners with an estimated ~1/3 to be impacted

-

Prada should be able to recapture a portion of these sales through its retail stores, ecommerce, and existing online partnerships

-

Better controlling its partners should allow the company to better control pricing

-

Expanding reorienting wholesale to online partners including Farfetch, and HighSnobiety, a streetwear focused publication.

-

Launched brand store on Instagram with checkout feature

-

Relaunched ecommerce capabilities, including a new ecommerce platform in 2017

-

Rolling out country-specific websites on an ongoing basis and is expected to achieve global coverage by 2020.

Engagement: Increasing digital engagement to capture younger customer, and build data-driven view of customer

-

Total digital as a % of A&P spend has increased from 10% in 2016 to 40% in 2018 and is expected to surpass 50% in 2019

-

Rolling out pop-up stores and hosting more than 700 promotional events in 2017

-

Creating experiences for customers across Prada and MiuMiu

-

Becoming the title and presenting sponsor for the America’s Cup (replacing Louis Vuitton), and launching a Luna Rossa challenger boat

-

Building infrastructure for data-driven view of the customer, recently partnering with Adobe, Oracle and Microsoft across these efforts

3. Green shoots of turnaround are present but are masked by further investment, sales rationalization and FX

Despite the worse than expected reported results in the recent quarter, we see evidence that the turnaround is trending positively.

-

Sales grew year over year across all product categories in 2018 with notable growth in ready to wear and leather goods after experiencing like for like declines from 2014-2017

-

Sales density bottomed in 2017 and increased y/y in 2018 and management highlighted LSD comp store growth to start the year in 2019

-

FX impacts both sales and profits: reported profits declined 10% y/y while constant currency EBIT was flat y/y; FX is expected to be a tailwind in 2019

-

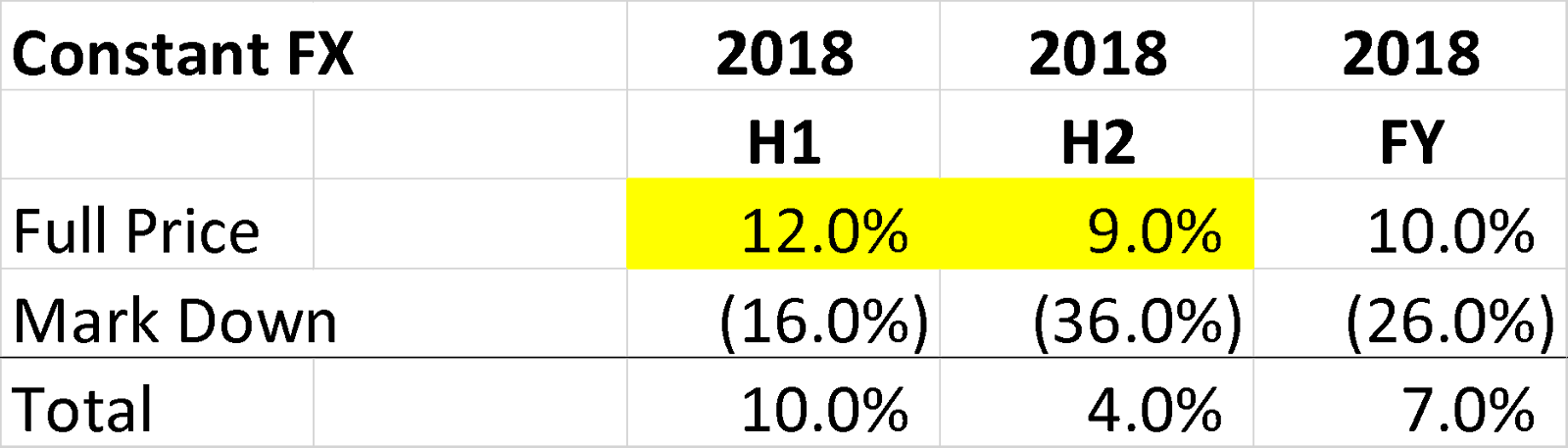

Full priced product sales grew 10% in 2018 with slower deceleration between H1 and H2 than mark down sales. Impact of reduced mark-downs should abate in 2020

|

Full price sales were more consistent in H2 than mark downs |

|

|

-

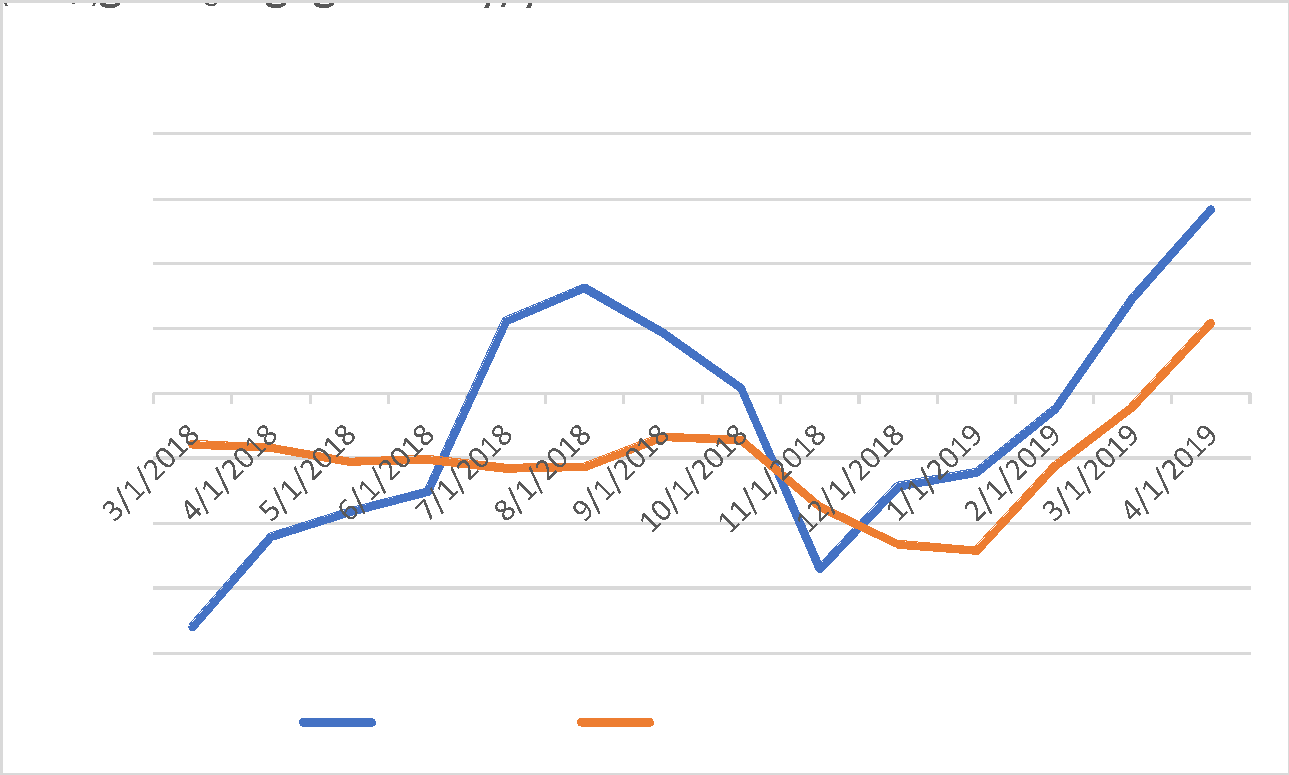

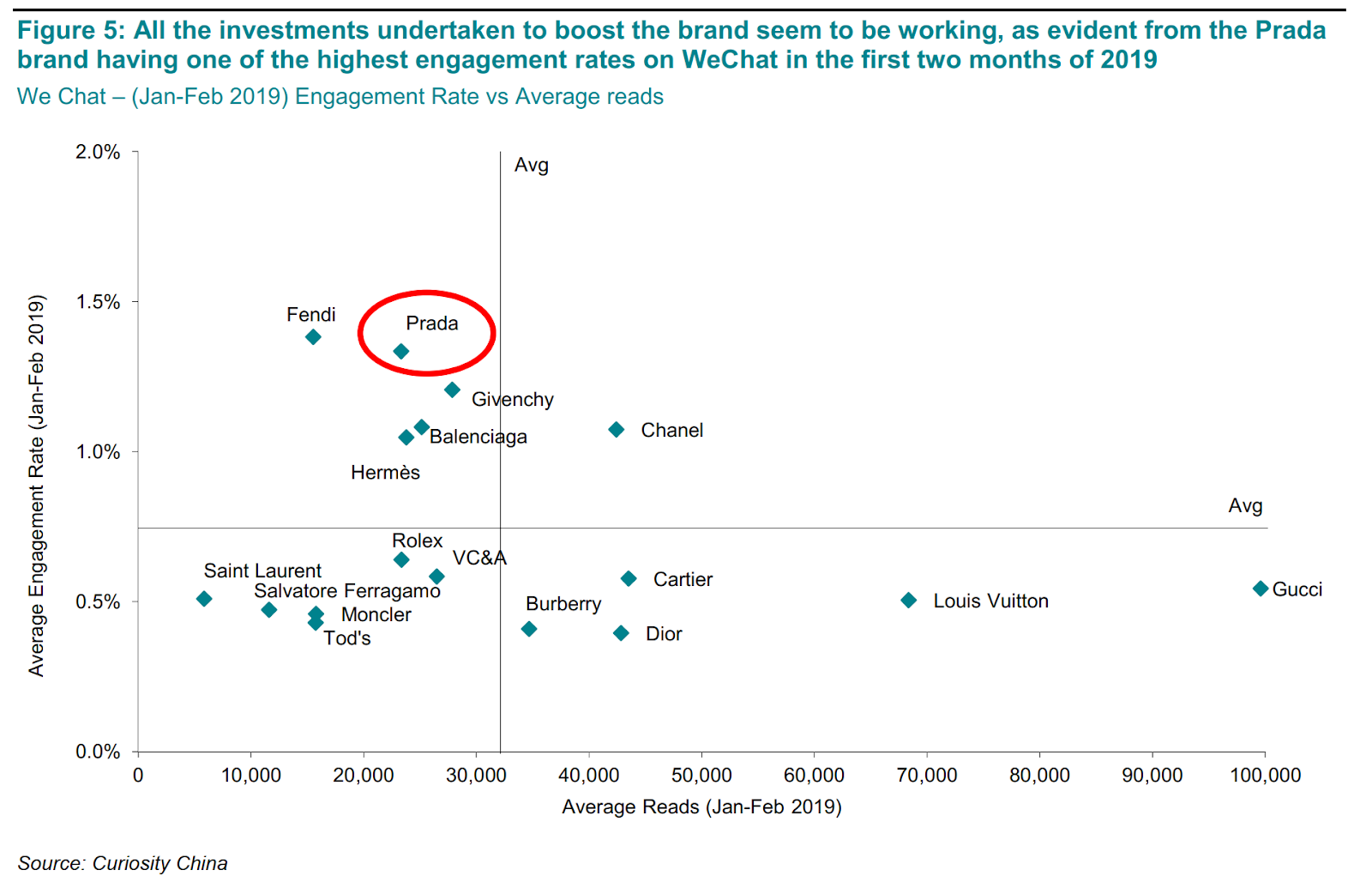

Social media engagement has been improving in Instagram and WeChat channels as well as reported “brand heat” from Lyst.com

|

Prada’s Social Media Engagement is Improving |

|

|

|

|

|

|

4. Expectations embedded in the current valuation and consensus are now really low

-

Consensus now expects just 13% margins in 2021, which are significantly below Prada’s long term average and peers with similar sales mix, despite tailwinds to margins from lower mark downs and wholesale normalization

-

Sales densities are at 1/3 of peak levels (2012) despite benefits from inflation and significant luxury spending growth in China and are not expected to reach the past peak until 2024

-

Capex is expected to increase continuously despite slowing new store growth from double-digit annual openings to one per year

-

Estimates currently assume a gradual recovery of mid-single digit comps, which lags the overall luxury market despite a tailwind to retail from wholesale closures and FX

-

Gross margins are expected to modestly rise over time by 20-30 bps per year despite

-

Long dated sell side models assume EBIT margins don’t exceed 15% by 2025

-

Valuation: Shares are just 4% above their 52 week low and the company’s EV/sales is ~2x just above its low since listing of 1.8x in January 2016, while peers average ~2.5-3x+

-

Reverse DCF of current prices implies EBIT margins never reach 20%

-

As Prada’s turnaround progresses we expect significant operating leverage that will ultimately drive EBIT margins over 20% vs. group margins that are expected to be ~10% in 2019.

|

Retail and leather goods mix supports 20%+ margins |

|

|

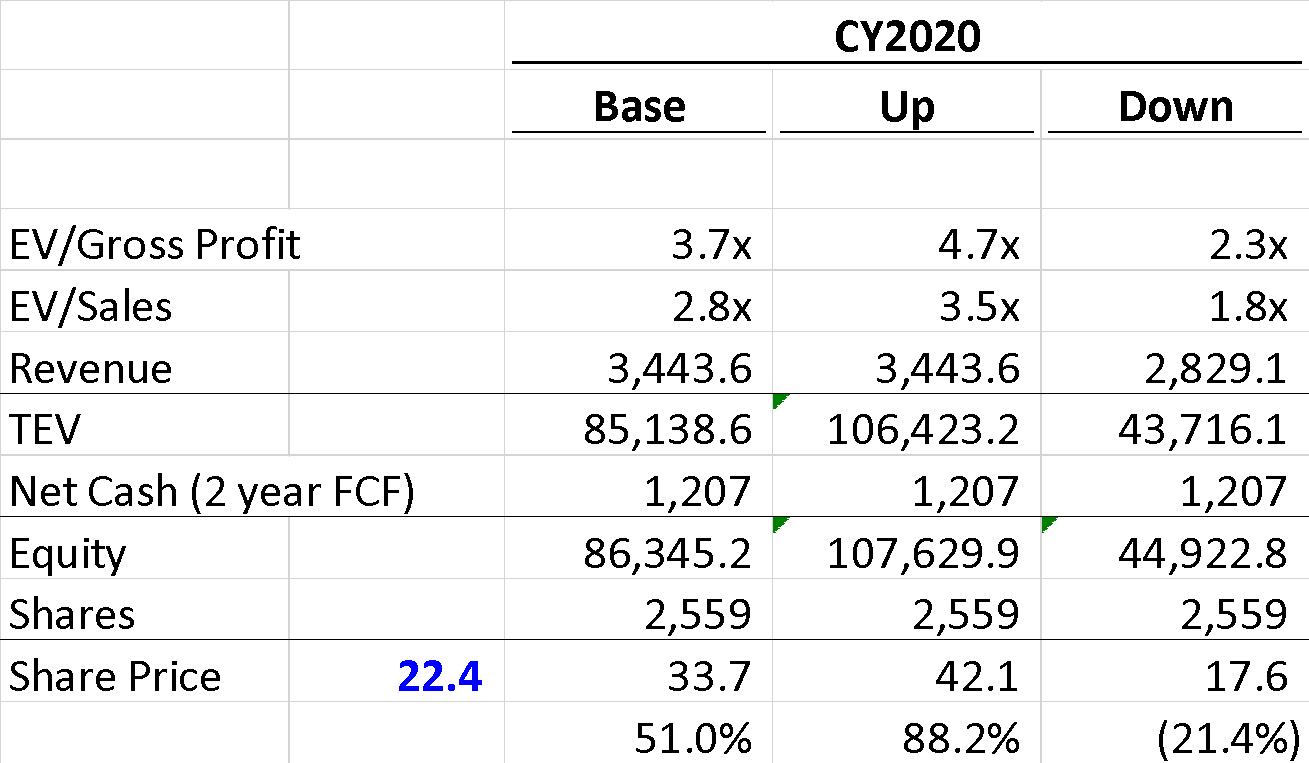

5. Attractive risk reward at current share price despite limited earnings assuming limited impact of the transformation program

|

Compelling potential returns and risk/reward |

|

|

We believe Prada should trade at a premium to Ferragamo, which is family controlled and undergoing a turnaround, due to Prada’s higher-margin product mix, declining like for likes at Ferragamo in 2018 (vs. Prada’s positive comps), and smaller scale. Ferragamo trades for 2.6x sales, a 30% premium to Prada on an ev/sales basis.

Downside: We think the Prada Group trading down in line with Tapestry on an EV/Gross profit, while retail sales / store and wholesale sales falling 20% is a conservative downside scenario, which would result in a share price ~20-25% below current levels.

Transactions: Versace was the most recent large fashion house to be acquired. The brand was sold for 2.7x sales to Capri Holdings in September 2018. The sale price is a notable premium to Prada, particularly given Prada’s better brand health and higher gross margin product mix. While we don’t think Prada will sell, we believe there is a put to sell the company above the current share price to either LV/Kering or PE which has had strong results from acquiring luxury brands (Moncler/Canada Goose).

Optionality:

-

New external CEO with significant luxury goods experiences joins group prior to Lorenzo Bertelli taking over as CEO given Lorenzo’s limited experience

-

Rationalization of non-earning or under-earning brands: MiuMiu and Churchs. We believe these brands are at best a distraction and at worst a drain on profits

Downside risks / negatives

-

China Exposure: The trade war and other issues could drive weakness in Chinese consumer spending. 35% of Prada’s sales are in China and Chinese tourists benefit spending in other geographies. We believe this exposure can be hedged by shorting other luxury goods companies with similar exposure to China.

-

Limited M&A potential: While there is considerable demand for luxury goods assets and Co-CEOs and husband/wife duo Miucci Prada and Patrizio Bertelli are over 70 years old, we don’t believe that Prada will sell in the near or medium term. Bertelli’s son Lorenzo Bertilli appears to being groomed to be CEO and Patrizio has commented in interviews that he will have the option to run Prada one day if he wants the position.

I and/or others I advise hold a material investment in the issuer's securities.

Catalyst

-

Green shoots seen across the company’s transformation, which are most importantly positive LFL trend in full price retail sales, increasing gross margins, and bottom line profitability

| show sort by |