| 2018 | 2019 | ||||||

| Price: | 28.58 | EPS | -4.00 | -2.00 | |||

| Shares Out. (in M): | 21 | P/E | 0 | 0 | |||

| Market Cap (in $M): | 609 | P/FCF | 0 | 0 | |||

| Net Debt (in $M): | -96 | EBIT | -60 | -40 | |||

| TEV (in $M): | 513 | TEV/EBIT | 0 | 0 | |||

| Borrow Cost: | Tight 15-50% cost | ||||||

Sign up for free guest access to view investment idea with a 45 days delay.

- Barry Honig

- Why is this even allowed to trade?

- More of an art than a science

- “Your Director of Quality has stated the process ‘is more of an art than a science’”.

- None found

Description

Thesis

PolarityTE (COOL) is a $600 million market cap, low float stock promotion scam created by notorious Boca Raton stock promoters Barry Honig and Michael Brauser. COOL claims it is a “commercial stage” regenerative medicine company even though the company has no products that have ever been approved by the FDA, the company has never conducted a clinical trial, the company has never published research papers demonstrating its technology works, the company has no safety or efficacy data that proves its product is safe or works, and the company has de minimus revenues. COOL claims to have patented intellectual property but no patent has ever been awarded to COOL or its CEO Dr. Denver Lough. In fact any patent awarded to Dr. Lough would likely be rightfully owned by Southern Illinois and John Hopkins Universities, where Dr. Lough did the research that formed the basis for COOL’s patent applications prior to founding the entity that ultimately was reverse merged into COOL. With de minimus revenue, no proprietary intellectual property, and a roughly $10 million quarterly cash burn rate, we believe COOL shares have little intrinsic value beyond the company’s roughly $4.50/share in net cash. COOL shares are likely to be revalued down materially over the remainder of the year as over half of the company’s shares will exit lock-up agreements by October 9th. While COOL’s stock is relatively expensive to borrow, the stock does have a fairly liquid options market. We recommend buying put options.

Capital Structure

|

Share Price |

$28.58 |

|

Shares Outstanding |

21.3 |

|

Market Cap |

608.8 |

|

Cash |

95.8 |

|

Debt |

0 |

|

Net Debt |

-95.8 |

|

Enterprise Value |

513.0 |

On April 12, 2018 the company completed a public offering providing for the issuance and sale of 2,335,937 shares at an offering price of $16.00/share. Cantor Fitzgerald acted as the underwriter for this offering.

On June 7, 2018 the company completed an underwritten offering with Cantor Fitzgerald providing for the issuance and sale of 2,455,882 shares at an offering price of $23.65/share.Interestingly, Cantor’s research analyst cut his price target on the company from $70 to $65 five days after this offering was completed.

Company Overview

PolarityTE is a biotechnology and “regenerative biomaterials” company seeking to commercialize an alternative to traditional skin grafts called SkinTE.

PolarityTE went public through a reverse merger of an entity called Polarity NV into Majesco, a publicly traded video game company controlled by Barry Honig. The reverse merger was announced in December 2016 and closed in April 2017. The gaming assets of Majesco were sold in June 2017. PolarityTE is headquartered in Salt Lake City, UT and has a small office in Hazlet, NJ.

In conjunction with the announcement of the reverse merger, COOL hired Dr. Denver Lough as its CEO and Dr. Edward “Ned” Swanson as its COO. Until their respective appointments, both doctors were associated with John Hopkins University as full time residents. According to the company on December 1, 2016, Dr. Lough assigned the patent application as well as all related intellectual property to PolarityTE Inc. On April 7th, 2017 the company issued preferred stock convertible into 7,050,000 shares of the company’s common stock to Dr. Lough for the purchase of Polarity NV’s assets. Dr. Lough’s shares were converted into common stock on March 6, 2018. Dr. Lough’s shares are under a lock-up that expires on October 9, 2018.

Conceptually, SkinTE begins with a small piece of the patient’s own healthy skin tissue. From this small piece of skin tissue, SkinTE tries to self propagate the sample in an effort to stimulate the patient’s own cells to regenerate the target tissues. The doctor takes the skin sample, sends it to PolarityTE and receives it back in a couple of days. The final product is a paste that is applied to wounds and burns.

You can watch a fancy Fox Business interview with Dr. Lough which explains the basics of the process here https://www.youtube.com/watch?v=iPduIQ8gips

SkinTE is not approved by the FDA and has never been reviewed by the FDA

According to the company’s SEC filings, SkinTE is registered with the United States Food and Drug Administration (“FDA”) pursuant to the regulatory pathway for human cells, tissues, and cellular and tissue-based products (“HCT/Ps”) regulated solely under Section 361 of the Public Health Service Act (“361 HCT/Ps”), which permits qualifying products to be marketed without first obtaining FDA marketing authorization or approval, and is commercially available for the repair, reconstruction, replacement and regeneration of skin (i.e., homologous uses) for patients who have suffered from wounds, burns or injuries that require skin coverage over both small and large areas of their body.

It’s not abundantly clear that SkinTE qualifies for the Section 361 exemption. The SkinTE process outlined by COOL in its patent applications seems to be inconsistent with the FDA’s December 2017 guidance for the section 361 exemption (https://www.fda.gov/downloads/BiologicsBloodVaccines/GuidanceComplianceRegulatoryInformation/Guidances/CellularandGeneTherapy/UCM585403.pdf ). A series of seeking alpha posts by user “Research Noir” does a pretty good job outlining the reasons why SkinTE likely would not qualify for such an exemption.

The biggest bombshell from Research Noir’s articles is the disclosure of an FDA FOIA request that reveals that the FDA has never inspected or investigated PolarityTE.

Source: Research Noir â„… Seeking Alpha

According to the company’s SEC filings, the company began clinical trials of SkinTE in 2018 at “multiple centers” comparing the product to split-thickness skin grafts, the current standard of care. There is no evidence of such a clinical trial on clinicaltrials.gov.

In addition, COOL believes that its product has applications in the regrowth of skin, bone, cartilage, fat, muscle, blood vessels, neural elements, as well as solid and hollow organ composite tissue systems.

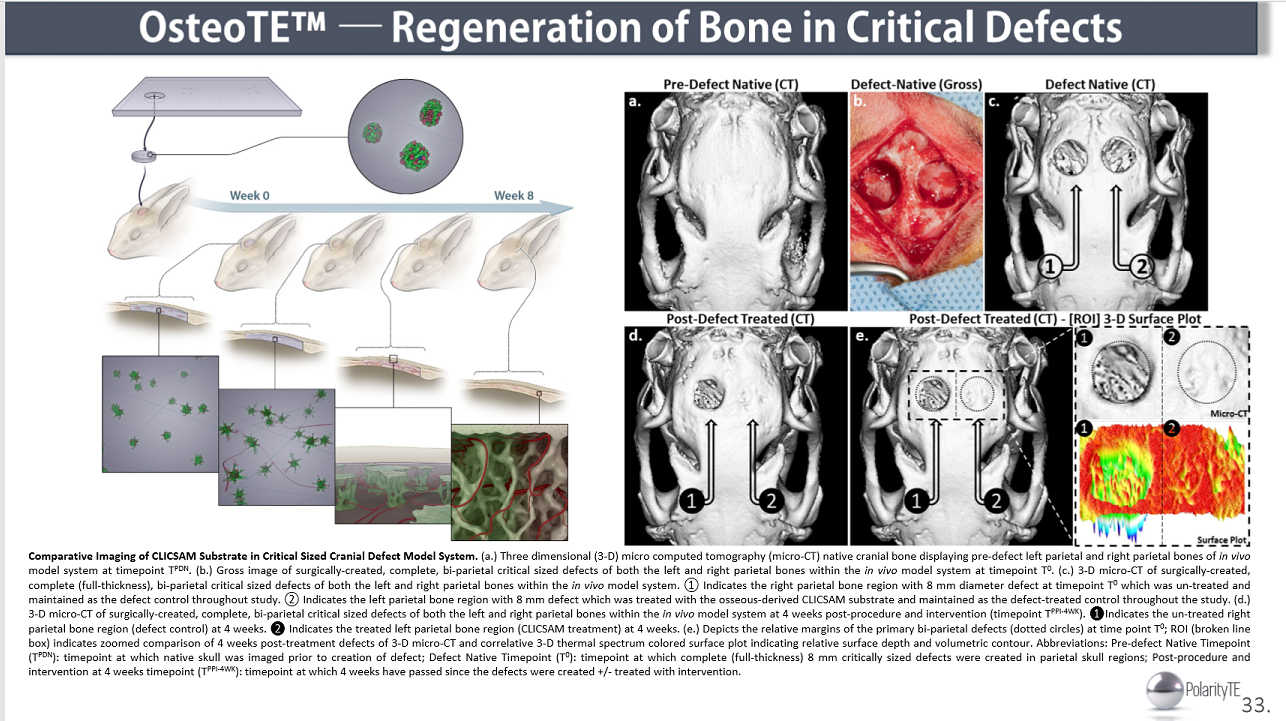

The company claims that it will be launching a new product called “OsteoTE” in late 2018. This product would in theory be able to regenerate bone. So far COOL has only completed preclinical validation studies for the product yet it claims that it will be commercializing the product later this year. Basically, the company has done some tests on some rabbits; this seems pretty far removed from having a product that is ready to be commercially sold to humans.

Seeking Alpha user Research Noir did a pretty good analysis ( https://seekingalpha.com/instablog/49608862-research-noir/5192848-osteote-skull-switcheroo

) of the rabbit x-rays included in slide 33 of the company’s current presentation ( https://d1io3yog0oux5.cloudfront.net/_df258990c899c5a921a08b47919775c3/polarityte/db/270/1647/pdf/PolarityTE_iDECK_7.13.18.pdf ) pointing out that they are almost certainly from different rabbits. Needless to say, x-rays from different rabbits would not be evidence that bone is being regenerated in one of the rabbits.

Commercialization Strategy

The initial “commercialization” of SkinTE was targeted for the treatment of up to 50 patients in the U.S. at roughly 30 different health care centers. SkinTE was targeted for patients with complex wounds including burn patients, acute trauma, chronic wounds, diabetic foot ulcers, and an epidermolysis bullosa patient.

In 2018, PolarityTE applied for an HCPCS code for the SkinTE tissue product from CMS and according to the company’s recently filed 2017 annual report, it received a recommendation for a SkinTE specific product code to be initiated in January 2019.

On July 25th, the company issued a press release stating in part that SkinTE has “transitioned into Stage 2 of commercialization” and that “the company has begun generating revenues while improving the lives of patients.” The company indicated that “all hospitals, clinics, and practices that have completed their evaluations of the product have initiated purchase agreements with the company.” In addition, the company indicated that the company “continues to grow revenues and now expects to exceed both internal and Bloomberg consensus 3Q revenue estimates.” Given estimates for Q3 revenues were roughly $300k, this isn’t exactly a particularly meaningful disclosure as it would imply the company had roughly 40 patients in the July quarter (SkinTE is estimated to have a treatment cost of $7,300.)

Recent Events

On March 2nd 2018, PolarityTE acquired a Utah based pre-clinical GLP Contract Research Organization named Ibex Group LLC for $1.6 million in cash which has been renamed PolarityRD. PolarityRD, a service-based research and development arm seeks to improve, enhance, support, and drive forward promising research with customers, industry partners and academic institutions by leveraging the extraordinary human capital and equipment that PolarityTE has acquired since its inception. COOL has a subsidiary PolarityIS, a corporate development arm, which aims to seek out new and novel growth strategies involving M&A, licensure and partnerships related to PolarityTE technologies, products and services.

On June 20th, COOL hired Paul Mann as its CFO replacing John Stetson who was reassigned to become the company’s Chief Investment Officer and President of the company’s strategic development office. One wonders why a clinical stage “regenerative medicine” company needs a chief investment officer. Mr. Mann was a healthcare portfolio manager at Highbridge for about a year and a half after a 2.5 year stint as an analyst at Soros Fund Management, and a several year stint as a portfolio manager for Lodestone Natural Resources. Before Lodestone, Mr. Mann was a sell-side equity research analyst focusing on the chemicals sector for Morgan Stanley. Note: Lodestone Natural Resources was shut down after two of its senior executives were arrested and charged with insider trading. (https://www.barrons.com/articles/BL-FUNDSB-12069 )

On June 25th, COOL hosted a key opinion leaders summit. In addition on that same day COOL was added to the Russell 2000 and Citron posted a short report on the company. The Citron report can be found here https://citronresearch.com/wp-content/uploads/2018/06/Citron-Exposes-History-of-FRAUD-Behind-PolarityTE.pdf

In the July 25th press release, the company included the following statement: “Despite the success observed with the initial roll out of SkinTE, there have been unsubstantiated rumors regarding the company and its lead product, SkinTE, by short sellers and competitors. While the company does not ordinarily comment on rumors and speculation, when these rumors start to affect SkinTE patients, their families, and their caregivers, we feel obligated to correct such misinformation. Individuals and/or groups on certain social media websites have recently engaged in deplorable attacks directed towards SkinTE patients and caregivers, and the Company condemns such disgusting and unacceptable bullying.

The Company is not a “fraud,” as known short sellers have claimed recently, and will not let these misrepresentations affect patients whose lives are at risk. There are many examples of patients whose lives have been positively affected by SkinTE, several of which were presented during the June 25, 2018 KOL summit in New York City.“

When companies feel the need to state that they are not a fraud, that usually is a pretty good sign that the company is not completely on the up and up.

Recent Financial results

In FQ2 2018 (quarter ended April 30, 2018), COOL had revenues from product sales of $3,000. This was a decline from the $13,000 in revenues the company had in FQ1 2018.

COOL lost $11 million in Q2 on an operating basis with expenses roughly evenly split between G&A and product research and development. COOL lost $18 million in Q1 on an operating basis. The company burned $14.5 million in the first six months of fiscal 2018. With the company ramping up its headcount, the cash burn is likely closer to a $10 million a quarter run rate at present.

Since the completion of the reverse merger into Majesco in April 2017 through the end of April 2018, PolarityTE has spent $19.3 million cumulatively on research and development. In that same time period the company spent roughly $30 million on general and administrative expenses.

Intellectual Property

While COOL has filed three patent applications to protect its intellectual property, to date none of these patents have been issued.

In the company’s 2017 annual report in the section on IP, the company states the following:

Continued Development of Intellectual Property: Twelve of the Company’s U.S. trademark applications have been allowed and the Company is now in the active prosecution phase with all three of its U.S. non-provisional patent applications: U.S. Application No. 14/954,335 published as US 2016/0151540; U.S. Application No. 15/650,656 published as US 2018/0154043; and U.S. Application No. 15/650,659 published as US 2018/0154044. The Company continues to actively file patent and trademark applications to protect its intellectual property and build out its patent portfolio as it relates to core cell-tissue biotechnologies and advanced related technology derivates (RTDs).

You can find links to each of these patent applications here:

https://patents.google.com/patent/US20180154043A1/en?oq=15%2f650%2c656

https://patents.google.com/patent/US20180154044A1/en?oq=15%2f650%2c659

https://patents.google.com/patent/US20160151540A1/en

In the company’s 2017 Annual report, it claims “Dr. Lough is the named inventor under a pending patent application for a novel regenerative medicine and tissue engineering platform filed in the United States and elsewhere. The Company believes that its future success depends significantly on its ability to protect its inventions and technology. Prior to December 1, 2016, no employees, consultants or partners engaged in any business activity related to the patent application and no licenses or contracts were granted related to the patent application, other than professional services related to preparation and filing of the patent.“

Likewise, in a February 2017 correspondence with the SEC, COOL writes: “On December 1, 2016 we hired Dr. Denver Lough as Chief Executive Officer, Chief Scientific Officer and Chairman of our Board of Directors and Dr. Ned Swanson as Chief Operating Officer of the Company. Until their hiring both doctors were associated with Johns Hopkins University, Baltimore, Maryland, as full time residents.

The doctors lead the Company’s current efforts focused on scientific research and development and in this regard on December 1, 2016, the Company leased laboratory space and purchased laboratory equipment in Salt Lake City, Utah. Subsequent expenditures during January 2017 include $1.25 million for the purchase of microscopes for high end real-time imaging of cells and tissues required for tissue engineering and regenerative medicine research. The Company has added additional facilities, and established university and scientific relationships and collaborations in order to pursue its business. None of these activities were performed by Dr. Lough or Swanson prior to December 1, 2016 in connection with their university positions or privately.”

What makes this disclosure quite interesting is each of these patent applications were started in December 2014. Since Dr. Lough was an employee of John Hopkins at the time, if these patents were ever granted, the patent would likely end up being owned not by COOL but by John Hopkins.

In fact, the research papers that appear to form the basis of Dr. Lough’s patent application (subsequently placed into COOL) are from 2014 referencing a collaboration between John Hopkins University and Southern Illinois University. Both Universities likely have a valid claim to ownership over the intellectual property should it prove to be valuable.

https://www.ncbi.nlm.nih.gov/pubmed/24572851

https://www.ncbi.nlm.nih.gov/pubmed/26818284

In a risk factor included in the company’s 2017 10-K and 2018 Q1 10-Q (but not the 2018 Q2 10-Q or the prospectuses for the April 2018 or June 2018 secondaries) the company claims that its IP was developed outside of “any institution.” Given Dr. Lough and Dr. Swanson were employed at the time by John Hopkins and the papers that form the basis of their patent applications were funded by Southern Illinois University and John Hopkins, the claim that their technology was developed “outside of any institutions” is almost certainly false.

There can be no assurance that a third party, including but not limited to a university or other research institution that our founders were associated with in the past, will not make claims to ownership or other claims related to our technology.

There can be no assurance that a third party, including but not limited to a university or other research institution that our founders were associated with in the past, will not make claims to ownership or other claims related to our technology. We believe we have developed our technology outside of any institutions, but we cannot guarantee such institutions would not assert a claim to the contrary. Even if successful, litigation to enforce or defend our intellectual property rights could be expensive and time consuming, and could divert our management’s attention. Further, bringing litigation to enforce our future patent(s) subjects us to the potential for counterclaims. In the event that one or more of our future patents is challenged in U.S. and/or foreign courts or the United States Patent and Trademark Office (“USPTO”) and/or foreign patent offices, the patent(s) may be found invalid and/or unenforceable, which could harm our competitive position. If any court or any patent office ultimately cancels or narrows the claims in any of our future patents through any pre- or post-grant patent proceedings, such an outcome could prevent or hinder us from being able to enforce the patent against competitors. Such adverse decisions could negatively affect our future, expected revenue.

Seeking Alpha user Research Noir does a pretty good job going into more detail on how COOL’s patents are almost certainly the property of John Hopkins and Southern Illinois University in an article you can find here: https://seekingalpha.com/instablog/49608862-research-noir/5199983-polarityte-develop-intellectual-property

Tightly Controlled Float

COOL’s float is tightly held with insiders and stock promoters Barry Honig and Michael Brauser collectively controlling 59% of the shares outstanding.

Sharesleuth has done a pretty good expose on the history of shady stock dealings by Barry Honig and Michael Brauser in the past couple of years. You can find their work here (http://sharesleuth.com/investigations/2018/07/cool-mara-riot-the-big-money-bitcoin-biotech-daisy-chain )

In addition, Sharesleuth does a good job outlining the numerous SEC investigations into Honig related entities writing:

Honig figures into at least three SEC investigations involving other companies he helped create:. They are MGT Capital Investments Inc. (OTC: MGTI); Cocrystal Pharma Inc. (Nasdaq: COCP); and Mabvax Therapeutics Holdings Inc. (Nasdaq: MBVX). Subpoenas issued in the MGT Capital and Cocrystal cases sought information about Honig, Stetson, O’Rourke, Groussman, Brauser and certain investment vehicles and charitable foundations they control.

Riot Blockchain disclosed in May that it, too, was the subject of an SEC investigation. It is unclear from the company’s description of that probe whether it extends to Honig and his associates.

Mabvax said in a filing last month that it appeared the SEC was investigating “potential violations by multiple holders of our preferred stock,” including the circumstances under which they invested, whether they acted as an group, and whether they sought to control or influence the company and its management. Mabvax also said that its financial statements from 2014 to the present should no longer be relied upon.

Mabvax’s stock was delisted from the Nasdaq yesterday, and now trades on the Over the Counter Market.

Registration statements from last fall show that the biggest holders of Mabvax’s preferred stock were Honig, Stetson, Brauser and Dr. Philip Frost, chairman and chief executive of Opko Health Inc. (Nasdaq: OPK). Opko, a Miami-based medical products company, also was a large holder.

SEC filings show that three of those same investors — Honig, Brauser and Frost — were the biggest holders of Majesco’s preferred stock prior to the merger with PolarityTE. They ranked second, third and fourth afterward. Groussman ranked as the fifth-biggest holder, owning five different classes of PolarityTE’s preferred stock.

Frost has invested in dozens of the companies that Honig has helped bring public, including Marathon Patent and Cocrystal, previously known as BioZone Pharmaceuticals Inc.

Our analysis found that Frost sold more than $6 million in PolarityTE stock last year. Those sales were properly disclosed, through an annual update to his original Form 13G filing.

Sharesleuth showed in a report earlier this year how a network of writers, some real and some fake, systematically posted nearly 600 bullish stories about Honig-backed companies on various financial sites.

Those “stealth promotion” articles included at least 90 pieces on PolarityTE, Marathon Patent, Riot Blockchain, Mabvax and the two other companies that now are involved in SEC investigations. That touting went as far back as 2013.

Many of those stories coincided with paid promotional campaigns, capital raises, mergers and acquisitions and other potential market-moving events. Those tout stories have ceased since we published our findings.

Pretty much every company Honig and Brauser have been involved with has seen its share collapse over time. The Citron report has a good table detailing the failure of the Honig cabal’s companies.

Source: Citron Research

The WSJ earlier this year wrote an expose on Barry Honig. The article does a good job of going through Mr. Honig’s background and his incredible knack for dumping shares of companies he is involved in right before their share prices collapse. I imagine owning a stock transfer company is quite helpful in timing exits in these types of stocks. The article also touches on SEC investigations into Mr. Honig’s companies and the SEC’s specific requests in these investigations for documents “relating to Mr. Honig and other investors.” (https://www.wsj.com/articles/investor-who-rode-pivot-from-biotech-to-bitcoin-sells-big-stake-1517403600 )

COOL’s officers and directors outside of Dr. Lough are subject to a share lock-up agreement which expires on September 4, 2018. Dr. Lough’s lockup agreement expires on October 9, 2018. The parties to the lockup agreement are:

2,356,806 shares will unlock on September 4th 2018. Dr. Lough’s 8,133,333 shares will unlock on October 9th 2018.

In addition to their share ownership, Dr. Lough and Dr. Swanson have significant in the money stock options, many of which are exercisable.

Share based awards under the company’s existing and proposed share compensation plans would increase the share count by 53% if fully utilized.

Other

-

COOL’s auditors are EisnerAmper LLP out of Iselin New Jersey. Why a company headquartered in Salt Lake City is being audited from NJ is a good question.

-

On August 9th 2018, COOL added David Seaburg to its board. Mr. Seaburg is a managing director and head of sales trading at Cowen & Company. He is also a CNBC Fast Money contributor. Mr. Seaburg is not an expert in biotechnology or health care and is not an investment banker. Mr. Seaburg’s addition to the board appears to be a clear attempt to attract retail investors into the company’s common stock.

-

COOL will be hosting its first earnings call when it announces results on September 12th

-

COOL will be presenting “clinical outcomes of SkinTE” as part of the scientific program at the annual meeting of the American Society of Plastic Surgeons in Chicago (Sept 28 to October 1 2018.) The company will host an investor webcast for this event. What a great opportunity to pump the company’s stock right before Dr. Lough’s lock-up expires.

-

COOL has material weaknesses in its internal controls. COOL expects to remedy these weaknesses by the end of 2018

-

Dr. Lough controls the proxy for 797,296 shares held by “certain of our other shareholders.” By virtue of this, Dr. Lough controls 41% of the outstanding voting capital of the company.

-

COOL’s investor relations guy Rich Haerle was most recently the director of healthcare specialty sales at Deutsche Bank. Interestingly, according to his LinkedIn profile, Mr. Haerle is still employed by Deutsche Bank and lives in New York City. He previously was an executive director in Healthcare Specialty sales at Morgan Stanley. One wonders why a clinical stage regenerative medicine company needs so many executives and board members with Wall Street experience and particularly equity sales and trading experience.

-

Jeff Dyer, a member of COOL’s board of directors, wrote an article in Forbes in August 2017. The article was such a blatant stock promotion (especially since it was released a few weeks after the company filed a registration statement for a stock offering and around the same time the company engaged Cantor Fitzgerald for that potential stock offering) that it even drew the attention of the SEC. https://www.forbes.com/sites/innovatorsdna/2017/08/08/polarityte-will-this-biotech-be-the-next-amazon-or-tesla/#3c340a95363a https://www.sec.gov/Archives/edgar/data/1076682/000149315217009535/filename1.htm

-

COOL has real well funded competitors in this space including Acelity, Medline, and Integra. These company have actually conducted real clinical trials to prove the efficacy of their products. They also have large sales forces and established relationships with healthcare providers and payers.

-

Barry Honig’s longtime securities lawyer Harvey Kesner is retiring from Sichenzia Ross Ference and Kesner LLP (as an aside they are Longfin’s external counsel) on September 5th. http://www.teribuhl.com/2018/08/29/kesners-out-why-is-barry-honigs-securities-lawyer-retiring/

-

COOL Received a going concern from its auditors in its 2017 audit.

Appendix

Here is Cantor Fitzgerald’s most recent model for the company. Needless to say, there is a lot of hope and flawless execution built into these estimates.

I and/or others I advise do not hold a material investment in the issuer's securities.

Catalyst

Catalyst

The share float frees up as insider lock-up agreements expire and the insiders dump their shares.

A potential investigation by the SEC into the company given they are investigating most if not all other companies Honig and Brauser are involved in.

The US Patent and Trade Office refuses to issue COOL a patent, or John Hopkins and Southern Illinois sue COOL to obtain ownership of the patents if they are issued by the USPTO.

The FDA rules that the company does not qualify for the section 361 exemption.

| show sort by |