| 2024 | 2025 | ||||||

| Price: | 20.00 | EPS | 0 | 0 | |||

| Shares Out. (in M): | 35 | P/E | 0 | 0 | |||

| Market Cap (in $M): | 686 | P/FCF | 0 | 0 | |||

| Net Debt (in $M): | 261 | EBIT | 0 | 0 | |||

| TEV (in $M): | 1,032 | TEV/EBIT | 0 | 0 | |||

Sign up for free guest access to view investment idea with a 45 days delay.

Description

Summary

New to VIC, Park Lawn Corporation (PLC) is a TSX-listed rollup of funeral homes and cemeteries. The only Canadian-listed player of its type, PLC can be considered a US-business operationally, with ~90% of revenues and locations based in the US.

Imagine the following situation: You are looking at a rollup business that until recently, held a mixed bag of assets between low margin/growth legacy businesses acquired nearly a decade ago, and newer higher quality acquisitions that are seeing results dragged down on a consolidated basis. Current (experienced) management, which joined during peak-COVID and thus has only just now had the opportunity to lead on a normalized basis, has also signaled a similar shift in strategy towards a greater focus on margins and operations. The business aims to generate 70% of its growth through M&A completed at reasonable multiples.

Yet, despite these facts, we see the following:

-

Consensus estimates have failed to incorporate margin uplifts that have already occurred, essentially assuming very recently divested legacy businesses will continue to drag on profitability

-

Consensus does not appear to capitalize value creation through M&A in a business which has targeted 70% of future growth being ascribed to rollups

-

Linked to the above points, new management is experienced and leading PLC through a turning point with a focus on higher margin and quality acquisitions, which we believe may be obfuscated due to their untimely tenure beginning during peak-COVID

Business Overview

While PLC has not been written on before in VIC, its deathcare rollup peers Service Corp International (SCI) and Carriage Services Inc (CSV) have been. To be brief then, in one sentence, PLC’s modus operandi is essentially identical to its peers: PLC focuses primarily on rolling up independent funeral homes and cemetery properties at (hopefully) reasonable multiples, then improving operations and performance on a roof-by-roof basis. Due to the importance of heritage in these businesses, acquired assets of PLC and peers also retain their original name and branding. Some more unique details on the company are as follows:

PLC began in 1915, and operated as a single cemetery for around 87 years. Then, in 2002, it purchased 5 cemeteries in Toronto. It was then stagnant until 2014, when it finally purchased Tubman Funeral Home, after which it began a consolidation journey led by the new CEO at the time, Andrew Clark. Since then, growth has been exponential, with the company turning from a single funeral home in 2014 to now being the second largest funeral home and cemetery consolidator in the industry (after SCI), holding 147 stand-alone funeral homes, 109 stand-alone cemeteries, and 36 on-sites (funeral home located on a cemetery). This has translated to a ~40% revenue CAGR from 2014 to 2022 (currency-adjusted).

In this sense, PLC is actually a very new player in the industry: SCI’s consolidation model is now 61 years in the making, and CSV is 32 years old. The focus on growth in the past 8 years, while having benefits on scale, has led to a different financial picture than peers, primarily on margin: On adjusted EBITDA margins, CSV is at 29.7%, SCI at 30.8%, while PLC is only at 22.5%. We believe this rests on 2 primary reasons:

-

PLC’s business mix is still overweight cemetery, which generally have lower EBITDA margins (e.g. PLC is ~42% cemetery revenues vs SCI at ~43% and CSV at ~16%. But, SCI’s figure also impacted by significantly more on-sites). Our discussions with industry holds cemeteries at ~15% EBITDA margins vs funeral services (burials) at ~30% EBITDA margins.

-

Past 8 years’ focus on growth inevitably comes at the expense of operational focus and better “integration” of new acquisitions. For instance, until recent release of ERP system FaCTS, management had limited disclosure on roof-by-roof performance metrics and wasn’t even able to disclose funeral vs cemetery operations. This translates to significantly worse management of field overhead. For instance, field level (separate from corporate) G&A at CSV is ~40% of sales vs SCI at ~25% (CSV lacks comparable disclosure).

On capital structure, PLC is the most conservatively financed, currently at ~2.2x EBITDA. This is significantly less levered than peers SCI at 3.3x and CSV at 5.5x and provides for good balance sheet flexibility going forward.

Industry Overview

While some previous writeups have already touched on the industry, we rehash the main relevant points here:

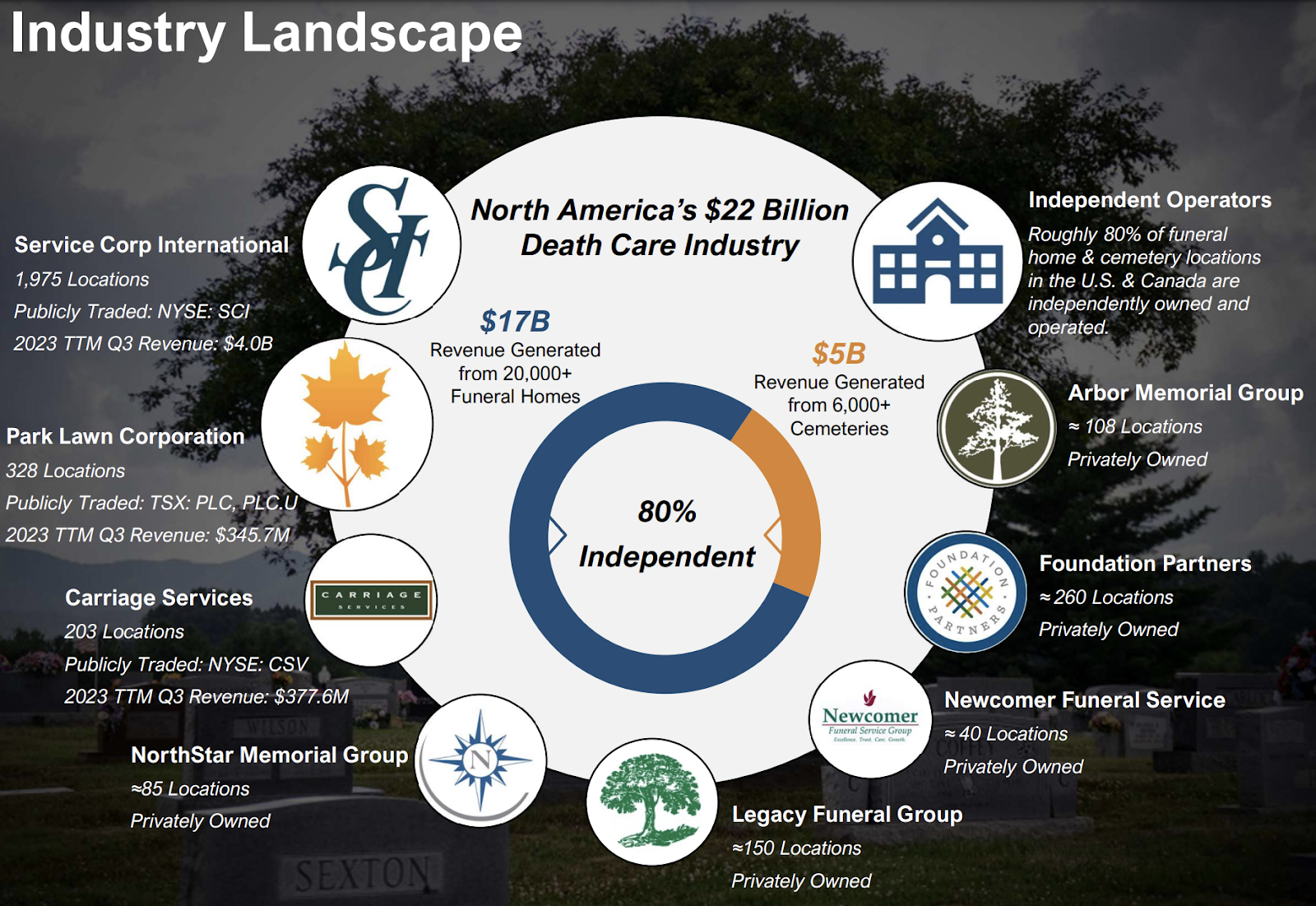

The aggregate deathcare industry in North America is worth $22b, with $17b from 20,000+ funeral homes and $5b from 6,000+ cemeteries. SCI is by far the largest player, with 1,975 locations and TTM revenues of ~$4.0b. PLC is the second largest by locations, with 328 locations and TTM revenues of $345.7m. CSV is next, with 203 locations and TTM revenues of $377.6m. Following these players are several large private consolidators (e.g. NorthStar Memorial Group with ~85 locations), but primarily independent mom-and-pop players with limited scale and local focus. These players provide a long runway ahead for consolidation, as 80% of the industry remains independent.

Source: PLC filings

A primary tailwind of revenue in coming years is the unprecedently aging population. This is a well-known driver at this point which has led to phenomenal growth in the long-term care and retirement residence sectors, but appears a bit more obtuse in deathcare: In Canada, the 60–79 bracket has more than doubled since 1980 and is projected to make up almost a quarter of the population by 2060. In the US, the 60–79 age bracket is expected to grow from 13% to 21% from 1980 to 2060 (~90 million people) while the 80+ age bracket quadruples (~35 million people). Never in history has the size of these 2 population groups been so large. With death rates having grown at ~1% annually in both Canada and the US over the past 35 years and a fairly consistent mortality rate of ~7%, this provides a floor rate on volume growth (sorry to be dark) before factoring in the now rapidly aging population and any pricing.

The main threat to this revenue growth is the increasing cremation rate due to cost-efficiency, which has shifted from 26% in 2000 to ~58% now in the US. However, while burials are pricier, cremation revenues may not be as low as one expects, with full-service cremations running ~$6,250 vs burials at ~$8,755 according to industry experts, with similar margins. On the cemetery side they come with significantly higher EBITDA margins (~50%) vs traditional cemetery services (~15%), though also significantly lower average revenues ($660 vs $4000). Overall, however, we believe the consistent MSD organic growth demonstrated by peers over the past 2 decades has shown relative resilience to this headwind (e.g. SCI cited in 2018 already facing >50% direct cremation of all cremation), and firms are working on mitigating the risk. Some initiatives by PLC include capitalizing on cremation through memorialization sales (~30% adoption and increasing), addressing outsourced cremation by owning ~40 crematoria (#1 in Toronto with >50% of cremations), and increasing associated niche sales (~20% adoption). We also observe that nearly 55% of PLC’s sites are located in the Southwest/Southeast US regions, where high religiosity has meant a lower cremation rate of ~48%.

Investment Theses

Our theses on PLC are relatively straightforward:

-

Consensus fails to incorporate margin uplifts that have already occurred, ignoring the recent divestments of legacy businesses on margins.

-

Consensus fails to capitalize value generation through M&A in a business which has targeted 70% of future growth being ascribed to rollups, erroneously relying on current market multiples to ascribe value instead.

-

New management is leading PLC through a turning point focused on higher margin and quality acquisitions, which may have been obfuscated due to management’s untimely tenure beginning during peak-COVID.

THESIS 1: Market has ignored margin uplifts that have already occurred

The margin uplift here is very straightforward but appears to be missed: On October 17th, 2023, PLC announced the divestiture of 72 cemeteries and 11 funeral homes for a deal worth $70m, at an 8x EBITDA multiple. Disclosure on exact normalized margins of these businesses and revenue mixes are limited, but past discussion on some assets contained within offer some clues to back-solve for more information: “In MMG … we would expect on—our plan for that business is to get it to mid-teens.” (Q3 2018). Taking a 15% adjusted EBITDA margin, this implies on a EBITDA-loss base of $8.75m a negative revenue impact of ~$60m which we incorporate into go-forward sales forecasts.

Perhaps it was because this is the first time in PLC’s history of any notable divestment, or more likely, because it was on page 77 of the 84 page release, but consensus appears to have missed the following crucial information: “Excluding the Disposed Businesses from the Company’s cemetery and funeral operations, the Adjusted Field EBITDA Margin would increase by approximately 340 bps and 350 bps for the three month and nine month periods ended September 30, 2023, respectively.” With PLC currently operating at ~22.5% adjusted EBITDA margins, this would imply at least (before factoring lowered corporate overhead) ~26% adjusted EBITDA margins post-divestment. Where is sell-side consensus modelling at for the coming years? ~24.5% flat. Again, we highlight that these are field EBITDA margin impacts and therefore should flow directly down to the margin upon divestment.

Source: PLC filings

Another area of potential margin improvement comes with the fact that management has explicitly guided towards improved corporate G&A scaling, guiding to 8% by 2024 end. Management has also noted that the divestment will hold an associated proportional impact on corporate G&A spend, furthering confidence that such margin targets are achievable.

We value Thesis 1 entirely organically, on existing portfolio assets as of 2023 end. Our valuation thus incorporates a 26% field adjusted EBITDA margin in 2024E driven by divestment mix benefits (3.5% higher than current). We conservatively also project an 8.5% corporate G&A spend on revenue in 2024E (below target reduction), which reaches to 8% thereafter. We also factor in associated revenue losses from the divestments of $60m. Combined with conservative organic growth assumptions of 2.5% going forward (vs SCI target 5-7%, CSV mix-adjusted target ~4%, and management guidance at 3-4%), this leads to a ~20% upside. This translates to a terminal multiple of ~10.5x EBITDA, far below the average ~15x pre-COVID and closer to recent lows of ~9x.

We also highlight that we do not give any additional credit to improved margins going forward from any other sources, despite operating leverage and management guiding to future focus on “higher growth potential, higher-margin businesses, things that we can really go in and improve” (discussed later in Thesis 3). With divested assets comprising of smaller businesses relying heavily on at-need vs backlogged sales, the portfolio will also see less revenue variability going forward.

In summary, basically all you have to believe for ~20% upside through this thesis is that the recent disclosure of a 350bp margin uptick is legitimate, and that divested assets are likely to also lower corporate overhead. These aren’t big leaps if you ask us.

THESIS 2: Consensus fails to properly incorporate value generation through M&A in a business which has targeted 70% of future growth being ascribed to rollups

Call us crazy, but we think that if management believes 70% of go-forward growth will be achieved through M&A, it’s important to value this piece of the business independently. Yet, after recent tough quarters, not once have we seen sell-side correctly modelling this aspect of the business separately from the organic story of PLC, or even acknowledging its existence at all.

In fact, a curious situation occurs: Say you had a stock trading at ~13x EBITDA, which buys companies at below 8x EBITDA. Sell-side models in a ~5x multiple arbitrage as value from M&A accordingly. 4 years later, stock now trades at 8x EBITDA (with no deterioration in actual business quality), and sell side now models in 0 M&A value.

The above appears to be how sell-side thinks about PLC as it currently stands—relying entirely on Mr. Market to describe whether M&A value exists in a business that guides to 70% on M&A for long-term growth. For example, one analyst in late 2019 wrote, “We estimate that PLC has created ~$300 million of value (or $10 per share) from M&A over this time period”, relying on the multiple arbitrage argument described earlier. Then, following tough quarters recently due to normalization of death rates post-COVID, this same analyst notes, “Our estimates do not reflect M&A, which could comfortably add 15%+ upside to our NTM adj. EBITDA numbers”.

So, what is a back of the envelope way to approach valuing PLC’s M&A strategy? Firstly, PLC targets acquisition at a multiple range of 4-8x EBITDA, depending primarily on acquisition size premiums. This compares to a deathcare M&A market which typically transacts at a 4-10x multiple range depending also on size and asset types. Encouragingly, PLC does appear to take its target range seriously—of its 19 previous acquisitions, just 1 exceeded the range as “slightly greater” due to size. We believe that this consistency to target ranges greatly reduces the odds of significantly overpaying like the industry saw in the 1990s.

With this, a quick back of the envelope way to account for value creation through M&A is to determine the capitalized value in the difference between an assumed purchase multiple and a reasonable intrinsic multiple post-integration (which can be very different than current trading multiples). For the former, we assume that PLC completes acquisitions at an average multiple of 7x (conservative as closer to upper limit of 8x). For the intrinsic post-integration multiple, we note again that the recent divestment was completed at 8x, with divested businesses comprised of low margin (we estimate ~15% EBITDA margins), low growth assets. We believe that factoring in overhead scaling and organic growth initiatives (where management targets ~20% IRRs) on acquired assets, it is not unreasonable to assume BotE an intrinsic multiple on these assets of 8.5x upon integration. Another way to get there is observing that SCI, which follows a similar M&A playbook and business mix (albeit at far larger scale) has disclosed comfortability with acquisitions at a 7-9x multiple, implying that an 8.5x multiple post-integration is not overly ambitious especially as PLC continues to scale overhead.

Simple BotE valuation of M&A value via multiple capitalization. Assuming constant FCF conversion from EBITDA.

With these multiple assumptions, and an assumed integration period of ~1 year (in-line with historical management discussion), we get to a BotE ~15% IRR on M&A deals. Assuming ~$75m of acquisition spend per year (lower end of $75-$125m range in guidance), this is another ~16% upside in the stock. We note again that this formula of acquiring and integrating is the industry standard playbook which has seen clear success by players like SCI, and as PLC scales, returns on such deals will only increase due to better economies of scale and organic initiatives like on-site construction. Further, we highlight again that Thesis 2 is valued independent of Thesis 1, which was done on a purely organic basis with the portfolio as of 2023 end.

THESIS 3: Management is leading PLC through a turning point towards higher margin and operational focus, which has been obfuscated due to management’s untimely tenure beginning during peak-COVID

Our third investment thesis is not modelled into valuation out of conservatism, but serves to offer support on the achievability of our earlier theses. Simply put, we believe PLC’s current management, which took the helm during peak-COVID, is fit to lead PLC away from a legacy of lackluster operational focus from earlier exponential growth, and reprioritize profitability and sustainable growth. As the deathcare industry has slowly begun to normalize in previous quarters post-COVID, we’ve seen hints of this through more careful capex decisions by management. For example, in the recent quarter, management decided to cancel a group order worth $1.1m related to a cemetery project acquired in New Jersey in 2018 as “capital costs required … would not justify the potential return on investment”. Never in our observation has prior management been willing to harm top-line in exchange for better investment decisions. The small sized impact in our view also points to a management more in tune with operations on a local level, likely due to the recent integration of ERP system FaCTS which has finally led to roof-by-roof performance metrics being visible to management.

Why do we think this management team can change PLC’s portfolio quality better than prior management? Current management notes that prior management never intended to remain as long-term operators of PLC, which explains the existing portfolio of lower quality assets acquired in a period which prioritized growth over all else. He notes, “Before I became the CEO … the concept, no matter what [you all were] being told wasn't to keep this as a company that was going to be long term, right? That wasn't the goal. It is the goal now.” We are inclined to believe this, considering the backdrop: Andrew Clark, the prior CEO, led a group of investors in 2011 who acquired ~15% of PLC shares, which then led to Clark becoming the CEO starting in 2013. Before PLC, Clark had never worked in the deathcare industry. His departure also raised additional questions on his interests as CEO: Buried in page 30 of Q1 2020’s report, we have a “payment of approximately $93,000 in legal expenses incurred by Mr. Clark in connection with his departure”. This ties into allegations in lawsuits that Clark had allegedly violated fiduciary duties and misused trust fund assets for his own benefit during his tenure. More recently, PLC also sued Clark for allegedly violating non-competes in relation to FaCTS at his new helm at PlotBox, a vertical SaaS business for deathcare operations. Whatever the outcomes of these lawsuits, such a complicated history doesn’t exactly pass our sniff test of a prior management team necessarily well-aligned with the long-term interests of PLC.

Source: CanLii, Park Lawn Corporation v. Kahu Capital Partners Ltd., 2023 ONCA 129 (CanLII)

After Clark’s resignation and a reshuffling of executives, current management is led by CEO Brad Green and CFO Jay Dodds since 2020 with over 16 and 40 years of experience respectively in deathcare. Prior to PLC, Green and Dodds founded Signature, which they grew in 6.5 years from 8 funeral homes and 3 cemeteries funded by their own money to 21 funeral homes and 9 cemeteries before being acquired by PLC in 2018 for C$165m. Of the 10 on the executive team currently, 8 have worked together for over a decade in similar capacities and most have been running funeral homes and cemeteries since 2006.

We believe that management with Green at the helm is qualified and able to take the company on its current turning point towards improved profitability and growth, and our conversations with industry reflect positively on the team. As Green noted, “We're focused on making sure that we're buying the assets that the Signature Group would have bought, prior to us joining Park Lawn.” Looking at when PLC acquired Signature Group, the 180bp gross margin uptick implied a gross margin ~4.5% higher for Signature’s portfolio than prior PLC, and EBITDA margins of ~29% (higher than current PLC). This gives us confidence that management is not simply uttering false promises when they note a focus on operational excellence and profitability going forward. They appear to simply be refocusing back to the types of businesses they’re used to owning. Management compensation is 50% stock-based.

Valuation

We valued Thesis 1 and Thesis 2 impacts separately, with each respectively leading to ~20% and ~16% upside independently. To rehash core assumptions for each supported by an intrinsic valuation:

THESIS 1:

We value Thesis 1 entirely organically, on existing portfolio assets as of 2023 end. On margins, we assume 3.5% EBITDA margin uplifts resulting from divested asset mix benefits and a conservative ~0.5% downtick in corporate G&A % of revenues (below target) leading to 26% adjusted EBITDA margins in 2024. We then have 26.5% adjusted EBITDA margins going forward to account for full target achievement of run-rate corporate costs at 8% of revenue.

We account for the divested asset mix through removal from balance sheets (disclosed held-for-sale assets/liabilities) and associated ~$60m decline in revenue going-forward, assuming a 15% EBITDA margin on divested assets. We conservatively flatline organic growth on remaining assets at 2.5% which is moderately below both peer and management targets, and historical averages at ~3.6% pre-COVID. These assumptions imply ~$48m in FCF generation in 2026. Our base case takes 6.9% cost of capital accounting for leverage, and translates to an exit multiple at ~10.5x EV/EBITDA. This compares to the average ~15x pre-COVID and closer to recent lows of ~9x. Peers SCI are also trading lower at 11.5x (historically ~0.5x premium vs PLC), and CSV at 9.18x (though CSV is ~85% funeral homes, which normally sell ~2x lower than cemetery assets). Our look into 15 past M&A transactions lead us to comparably-sized firms to PLC being acquired at ~12x multiples. The recent divestment of lower quality assets at ~8x also creates a sensible valuation floor.

These assumptions imply a fair share price of ~$C23.80, or ~20% upside.

THESIS 2:

Our BotE valuation assumes that PLC completes acquisitions at an average multiple of 7x (conservative as closer to upper limit of 8x). We assume an intrinsic multiple on these assets of 8.5x upon integration. We believe these to be reasonable considering the recent divestments offering a floor at ~8x, consideration of targeted ~20% IRR organic initiatives, and SCI’s target multiples of 7-9x implying comfortability with value creation even at higher purchase multiples. We also do not account for operating leverage generating additional returns on M&A for PLC going forward. We conservatively also assume no growth in spend, and no value generated until full-integration from purchase.

With $75m acquisition spend assumed going forward (low end of guided $75-125m) which we model as funded through FCF and debt, at a 6.9% leveraged discount rate, we get an additional ~16% upside in PLC, independent of Thesis 1.

GENERAL:

Beyond the theses-specific assumptions discussed above, our key long term assumptions are (i) terminal growth rate at 2.5%, (ii) adjusted EBITDA margins staying at 26.5%, (iii) capex at 3.5% of revenues, (iv) investment assumptions leading to ~60% FCF conversion (excluding acquisitions) going forward.

We believe these are reasonable or conservative as (i) 2.5% is considerably below historical and peer/management long-term guidance discussed earlier, (ii) we underwrite 0 operating leverage going forward, (iii) mid-point of guidance, (iv) excluding acquisitions FCF conversions have been ~50-70% historically.

Valuation summary

Risks and Mitigants

The main 2 risks we consider are management execution risk on M&A and growth sustainability risk from cremation. We believe in other areas like cost scaling we have been conservative so as to maintain a margin of safety (e.g. no credit to operating leverage on margins going forward).

Management fails to generate positive NPV acquisitions going forward: Mitigated by independent valuation that still implies ~20% upside from essentially realized margin uplifts without any value attributed to M&A going forward.

Cremation adoption leads to lower average revenues per call: Our organic growth forecasts of 2.5% are already moderately below peer and management forecasts, all of which account for cremation risk. We also see this as easily offset considering historical ~1% volume growth due to mortality rates which will increase in coming years due to aging of baby-boomers, and therefore needing <1.5% pricing to be underwritten. Historical growth rates imply ~2.6% pricing yearly, and also factors in cremation.

I and/or others I advise do not hold a material investment in the issuer's securities.

Catalyst

Earnings: We anticipate margins to be properly underwritten by consensus when released for Q4 2023. We also anticipate lower earnings variability to be appreciated due to divestments of these smaller assets reliant on at-need vs backlog.

Buybacks: Management has indicated openness to buybacks, noting, “When our company is trading at a multiple, that is at … what we just divested those assets for, it definitely begs the question of utilizing capital for additional buybacks.” PLC on August 10, 2023 renewed its NCIB, which allows for the repurchasing of up to 10% of public float. It has ~9% available to repurchase by August 16, 2024. The Chair has also bought ~$C120k in stock since mid-November.

| show sort by |