| 2020 | 2021 | ||||||

| Price: | 70.54 | EPS | 0 | 0 | |||

| Shares Out. (in M): | 43 | P/E | 0 | 0 | |||

| Market Cap (in $M): | 3,005 | P/FCF | 0 | 0 | |||

| Net Debt (in $M): | 50 | EBIT | 0 | 0 | |||

| TEV (in $M): | 3,055 | TEV/EBIT | 0 | 0 | |||

Sign up for free guest access to view investment idea with a 45 days delay.

- two posts in one day

- None found

Description

Omnicell (NASDAQ: OMCL)

I would like to recommend Omnicell (NASDAQ: OMCL) as a long at the current share price of ~$70. OMCL is a provider of dispensing and medication management services and products to the acute and non-acute healthcare settings. These products are meant to ensure that hospitals operate in an efficient manner that aims to reduce costs and minimize human errors in the dispensing of medication. The current environment with COVID-19 has further highlighted the issues facing the American healthcare system. By implementing products and services that minimize waste and maximize hospital capacity, they can serve a greater portion of the population and improve the quality of the care.

Products/Services and Key Focal Points

The following 3 categories highlight where OMCL operates within the healthcare space.

- Point of Care (refers to where the healthcare services are administered) is where OMCL operates through its dispensing system, and its main product is XT Automated Dispensing Cabinets. The company has mentioned that it is in the early stages of the replacement cycle and remains focused on penetration.

- Central Pharmacy is where OMCL sells its medication management solutions oriented towards acute-care settings (short term settings such as Emergency Rooms and ICU), with it’s two main products IV sterile compounding solutions and XR2 Automated Central Pharmacy system. This segment has opportunities to reduce the burden on administrative staff and maximize efficiency

- Retail, Institutional and Payer refers to non-acute settings (non urgent settings such as clinics) where most drugs are distributed. OMCL’s main products in this segment are its Population Health Solutions portfolio (includes various software products and services) and its medication adherence packaging.

The benefits of the core products, as per OMCL’s website, are:

- XT Automated Dispensing Cabinets

- Reduces medication errors and better care

- Diversion prevention and better medication security

- Increases efficiency of nurses and pharmacy staff

- Improves regulatory compliance, and medication tracking

- Reduced inventory costs and minimizes impact of drug shortages

- XR2 Automated Central Pharmacy System

- Allows staff to focus on clinical tasks, instead of operational task, which leads to better patient outcomes

- Eliminates human error with 100% bar-code scanning

- Improves inventory management

- IV Sterile Compounding Solutions

- Enables best practices by ensuring patients aren’t overdosed or under-dosed

- Improves efficiency of staff and streamlines work-flow

- Ensures compliance standards are met

- Medication Adherence Packaging

- Increases medication adherence rates to 90% as per the studies conducted (currently medication adherence rates in the US are 50%)

- Can reduce blood pressure and HbA1c

- Allows pharmacies to increase their value proposition to customers, and outperform their competitors

Operations Overview

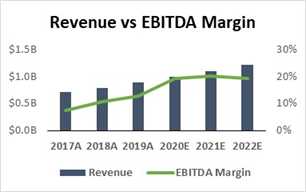

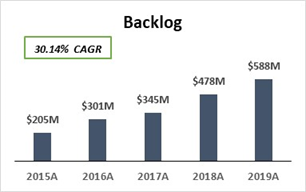

Omnicell has robust fundamentals with strong growth and margin expansion. Strong backlog growth can be used as a proxy for demand and future revenue. It has 90% of its sales generated in the USA, which is the largest healthcare market measured by healthcare spending per capita; no other country generates more than 10% of revenues. The revenue split is into two segments, products (74%) and services (26%), with gross margins of 48% and 51% in 2019, respectively.

Short Seller Troubles

In July of 2019th, GlassHouse Research published a short report which resulted in ~16% drop in the share price in the month of July. GlassHouse accused OMCL of misrepresenting it’s financials statements by prematurely recognizing its revenueand avoiding inventory write offs. Soon after, the SEC launched a probe into the company’s accounting standards. On 13th February 2020, OMCL filed an 8k which stated that the SEC had concluded its investigation into OMCL and did not intend to recommend any enforcement plans. I believe that the SEC’s investigatory findings are enough to absolve OMCL of the accusations levied against it.

Industry Trends

Several issues in the healthcare system are addressed by OMCL’s offerings. Research has shown that automated dispensing system can improve efficiency and can result in more than a 50% reduction in inappropriate drug use and administration. Automated IV compounding reduces error in compounding and allows for better traceability and management. These are some of the products and services that OMCL offers which can reduce health care cost, increase efficiency, and reduce dosage errors. This will ultimately improve the quality of healthcare provided.

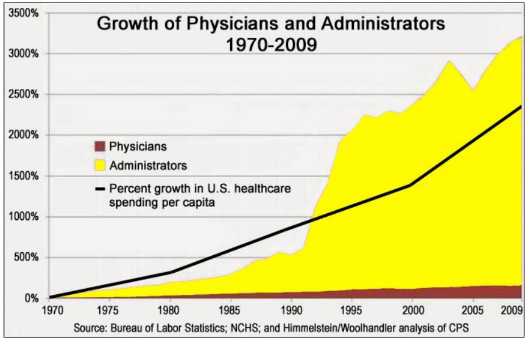

The chart above displays how physician growth is dwarfed by administrator growth which shows the inefficiencies with dealing with administrative functions which need to be automated to prevent errors and improve the efficiency of staff. According to the National Academy of Medicine, in the United States, half of administrative costs are excessive and do not add value. It is estimated that 38% of the cost gap between the US and Canadian healthcare system is attributable to administrative costs.

According to the Journal of Patient Safety, 210,000 to 400,000 deaths occur annually as a result of preventable healthcare mistakes. According to the Risk Management and Healthcare Policy Journal, 3 to 10% of total US healthcare spending is attributable to lack of medication adherence. To put that into perspective, based on the 2019 healthcare spend of $3.6T, lack of medication adherence cost was in the range of $108B to $360B. Furthermore, the WHO states that 50% of patients do not take their medication as prescribed.

A Gallup poll conducted in 2019, showed that 48% of Americans have a “Very/Somewhat Negative” view of the US healthcare system compared to 38% who believed had a “Very/Somewhat Positive” view of the US healthcare system.

All these stats indicate that there is a drastic need for improvement within the healthcare system, including within reducing administrative costs, and improving the process of managing medication administration and adherence. These are areas within which OMCL operates. With the Affordable Care Act (Obamacare), hospitals and healthcare providers are more incentivized to find ways to reduce costs and administer better healthcare. As a result, adoption of products and services such as those offered by OMCL should increase, since OMCL is aided by great secular tailwinds.

Strong Fundamentals

OMCL has been consistently engaging in product diversification to morph itself from a one trick pony to a comprehensive platform. These have been conducted through organic R&D and M&A. The company acquired InPharmics, Ateb and Aesynt. The products and services of these companies were bundled into OMCL’s own solutions, to give it a more comprehensive offering.

Additionally, the company has been working towards increasing its IV compounding solutions, and these efforts are aided by the fact that a competitor in the space, PharMEDium, shut down it’s operations in January 2020. The reason of PharMEDium had nothing to do with the attractiveness of the industry but was because of a Federal injunction issued due to lack of compliance with numerous safety violations. Furthermore, another competitor BDX has suspended shipments till the end of 2020, which gives OMCL an opportunity to capture even more market share. BDX’s decision to suspend shipments was tied with recall issues it had experienced in the prior year, indicating that the product has issues and is inferior to that of OMCL’s, who has not had any such issues. It is approximated that OMCL has 50% market share is expected to continue to gain 1.5-2.0% annually. Duke University Hospital reported that since adopting OMCL’s service, it has been able to increase its dose capacity roughly 3x, and has helped with inventory management. This is a testament to the value that OMCL’s services provide to healthcare providers.

Furthermore, OMCL’s XT Series has been ranked the best Automated Dispensing Cabinets for 13 consecutive years, by Klas Research. OMCL’s XR2 Automated Central Pharmacy system was launched in 2017 and appears to be a market leader in this space with no clear rival. One of the main benefits of the OMCL’s products are that they are customized and therefore customers can choose which specifications suit them based on their budget and needs.

Strong growth is expected in the service business, as the installed base of customers grows as a result of increased product sales. The service business offers a high margin, recurring stream of revenue which increases foreseeability into cash flows and makes the business safer from volatile swings in product demand, despite the product and service being interconnected. Management has been increasing its portion of revenue attributable to services over the past decade. It has not provided exact guidance on what it hopes the split is but has indicated it expects strong growth as it expands its service offerings.

The company has a healthy balance sheet with ample liquidity. OMCL has a non-adjusted Leverage ratio of 0.40x, and an Interest Coverage ratio of 28.4x, compared to its covenants of 3.5x and 3.0x, respectively. These are calculated using the company’s net debt of $50M, unadjusted EBITDA of $124.95M, and net interest expense of $4.4M. The undrawn component of its revolver of $450M and has uncommitted loan facility of up to $250M, which indicates that the business has ample avenues of liquidity.

The company is poised to experience margin expansion, as it introduces more products through a decrease in it SG&A and COGS margin. COGS margin is expected to decline since the economy will be able to achieve economies of scale in its production. Furthermore, the service sector is expected to grow to make up a larger portion of revenue, and is a high margin business than products, which will lead to a further decrease in OMCL’s COGS margin. SG&A margin will reduce because the company can sell multiple products to the same customers.

All these factors indicate that OMCL is a market leader in many of its core product and service lines. Given its ample liquidity, this business seems poised to continue to grow, and is well positioned to capitalize on this growing industry.

What is the Market Missing?

Since March 5th, 2020, the company’s share price has dropped 18.94%, which coincides with a broader market sell off amidst concerns about COVID-19, and the economic implications of a lockdown. General investor sentiment is bearish as credit spreads widening, and large losses for the major indices. This sentiment may be rational for certain businesses but seems unjustified for a business such as OMCL.

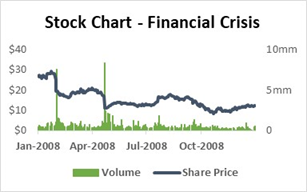

The stock suffered tremendously during the Great Financial Crisis, with it’s share price declining ~55% in 2008. This was attributable towards a delay in orders. However, OMCL is a much different business now with more recurring revenue, with service revenue being only 16.0% in 2008 compared to 26% now. Furthermore, the company has a more diversified product offering now than it did back then. Finally, this crisis is a healthcare crisis which highlights the need for OMCL’s product and services, in providing quality healthcare. Therefore, I would dispute any parallels between the two crises in respect to OMCL.

The main concern is that large orders may be delayed by hospitals who are currently focused on how to cope with the virus. Despite this potentially being true, OMCL has been deemed an essential business and it’s supply chain appears to be fully functional based on this quote from the company’s website “Our manufacturing and supply chain teams have enacted business continuity plans and do not presently anticipate any supply interruption”.

The company, unlike many others, appears to have revenue and demand continue throughout this tumultuous period. According to The Bureau of Investigative Journalism, hospitals are struggling with medication management, and pharmacists are spending a substantial portion of their time managing inventories of medication. As per the Yale School of Medicine, overprescribing medication is becoming an increasingly large issue with COVID-19, and leads to risks of overdoses, as well as shortages. These unfortunate set of circumstances have further highlighted flaws in the medication management industry, which can be addressed through products and services such as OMCL’s.

OMCL has responded to these needs and is trying to contribute to the healthcare efforts by fast tracking delivery of it’s preconfigured XT Automated Dispensing Cabinets to 5-7 days to ship and 3 days to prepare. According to The Guardian, as of 25th March 40,000 healthcare professionals have volunteered to act as a “surge health force”. This heightens training needs, and OMCL has responded by launching an online course, called MyOmnicell, which conducts rapid onboarding.

OMCL is better suited than most businesses to weather this crisis; however, there may be some near-term revenue declines due to some large order delays because of the resource constraints of the healthcare system. There will be continued demand for OMCL’s offerings throughout this crisis, it will just be reduced. Furthermore, in the long run the demand for the product will rise as inefficiencies in the healthcare system are magnified through this crisis and will need to be addressed.

RISK

- The company faces massive operational risks and faces substantial liability if its system has failures. Furthermore, reputation is key in this industry and as a result, an error on a single product could have a ripple effect on OMCL’s ability to continue to win contracts.

- GPO’s can negotiate unfavourable contract terms which can lead to material declines in profitability.

- Delays in the development in new products may result in lost revenues, as customers avoid purchasing existing products and wait for the new products instead.

- Hospital spending budgets and priority vary from year to year and can lead to a material loss and heightened volatility in revenue.

- Any material changes in healthcare regulation can affect the business.

Valuation

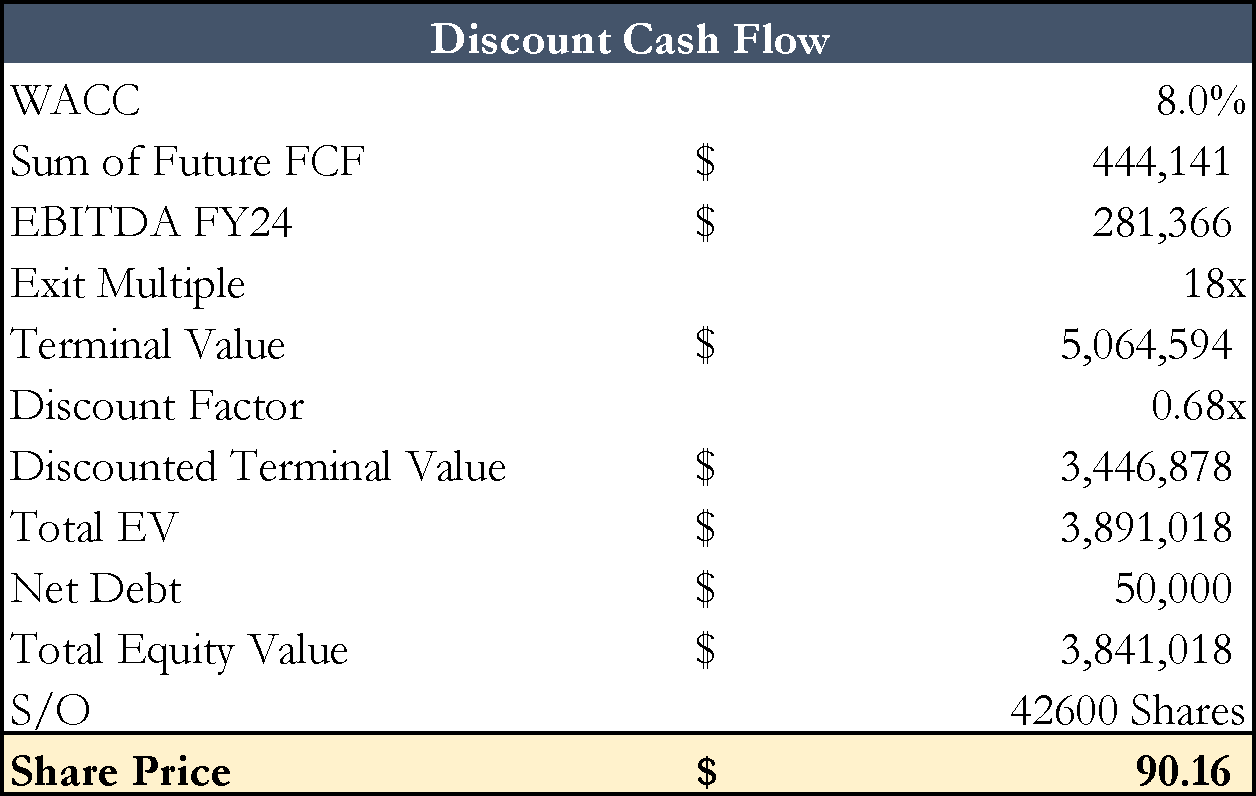

Based on my DCF, the share price of OMCL should be around ~$90 a share, which represents an upside of ~30% over the stock’s current share price of ~$69 a share. I used an exit multiple of 18x, which is less than the company’s 2-year average multiple of 18.4x.

Summary

OMCL is a defensible business, which has a strong financial position, and is a leader in an industry which faces numerous tailwinds. The stock has unjustifiably traded down, due to a provenly inaccurate short report, and broader market sell off. This business is just as relevant during this crisis as it was before.

I and/or others I advise do not hold a material investment in the issuer's securities.

Catalyst

As we exit this crisis, healthcare providers will start to invest more to improve their quality of healthcare and reduce their costs. As a result, revenues should increase for OMCL, and the market should start to value it closer to ~$90 a share, which is what it is truly worth in my opinion.

| show sort by |