| 2023 | 2024 | ||||||

| Price: | 10.38 | EPS | 0 | 0 | |||

| Shares Out. (in M): | 36 | P/E | 0 | 0 | |||

| Market Cap (in $M): | 456 | P/FCF | 14.2 | 0 | |||

| Net Debt (in $M): | -68 | EBIT | 31 | 0 | |||

| TEV (in $M): | 388 | TEV/EBIT | 12.5 | 0 | |||

Sign up for free guest access to view investment idea with a 45 days delay.

Description

Valuation

14.9x P/FCF 2022 with an additional 15% of market cap in net cash is too cheap for a storied branded beverage business that requires just $36 million of operating capital to produce $30 million of free cash flow.

Nichols plc is listed on London's AIM market under ticker NICL.L

Product description

“Vimto, the iconic refreshingly different soft drink that has it all. Created in Manchester in 1908 by John Noel Nichols, Vimto was originally designed as a herbal tonic to give its drinkers ‘Vim and Vigour’. For over 100 years, we have been mixing our secret recipe – a blend of fruits, herbs and spices – to produce a unique and irresistible range of drinks.

Today, we’re the 9th most chosen beverage brand in the UK, and enjoy a Global footprint consumed by consumers in 73 countries around the world. Our Vimto range includes squash, carbonates, still drinks, flavoured water and frozen. With a choice of unique flavours and Original and No Added Sugar options, there are lots of ways to enjoy Vimto. This also includes our extensive range of licensed products – from pancake mixes and home baking kits, to desserts and confectionery.”

Source: 2021 Annual Report

Glossary

Squash - juice drink from concentrate (not necessarily 100% fruit juice) diluted with water at point of serving. A staple in many British homes, especially ones with kids.

Cordial - sweeter and more concentrated squash; non-alchoholic.

4 businesses: 1 terrible, 1 good, 1 great, 1 growth opportunity

Since 2010, management has only segmented financials by Still and Carbonate; a useless prism for investors to understand profitability, but understandable for competitive reasons. If Middle East sales are pure royalty income based on a century-old recipe from Manchester, UK which gets manufactured, distributed and marketed from Dammam, Saudi Arabia, earning super high operating margins, both competitors and shareholders are none the wiser.

This month management split out the Out of Home (“OoH”) division in its 2022 results, demonstrating the difference between this and the “Packaged” segments by geography. The former is capital heavy and commoditized. Packaged segments are capital light and deliver returns in line with a quality brand:

Source: March 2023 investor presentation

Non-UK profitability will likely remain confidential. UK packaged is fundamentally different to the Middle East business, however, and I have always viewed Nichols Plc as 4 distinct businesses, of greatly varying quality and therefore valuation:

Great: Middle East (7% of sales). Many Muslims who fast during the daylight hours of the month of Ramadan break their fast at sunset with a glass of Vimto during the daily Iftar communal meal. This product is very different to UK Vimto. It is a double concentrated cordial (originally to reduce shipping volume from the UK); much sweeter; manufactured and premium packaged in glass bottles in Saudi Arabia by Aujan, Vimto’s Saudi bottling partner since 1928. Typical retail price of $3-4 for this non-alcoholic beverage in a wine-sized bottle, 25 million bottles are sold in the Middle East during the 4 weeks prior to and during the 4 weeks of Ramadan, representing 80% of Vimto’s Middle East sales. Market shares in Saudi Arabia and UAE are above 40%. Sheikh Adel Aujan, the grandson of the founder of Aujan Industries, became a billionaire by building a valuable beverage business around Vimto. After studying in the US he returned to Saudi Arabia in 1968, cemented Vimto’s tradition during Ramadan, localized production in the 1980s, and sold a 49% stake to Coca Cola in 2011 for $980 million, before his death in 2017.

Negatives of this business: though hard to verify, I suspect that the terms of the exclusive license to the region in 1928 for a then 20-year old Vimto, might have been too generous to Aujan, just like many of Coca Cola’s early deals. Also, since Coca Cola’s 2011 investment, Vimto’s Middle East sales have flatlined. The Saudi 2020 Sweetened Beverage Tax increased retail prices by up to 50%, without reformulation options which existed in other geographies like the UK whose government introduced a similar health levy.

Competitive advantages: brand power and history, high switching costs (premium but affordable product consumed during traditional family occasions).

Growth opportunity: Africa (11% of sales). For a consumer beverage business, African demographics are more favorable than any region in the world. Africa’s population will likely double between 2020-2050 to 2.5 billion, at a median age of 19 years (compared to 32 for Latin America and Asia; 39 North America; 43 Europe)[1]. Fast-growing populations with children representing 50%, in hot countries, with significant Ramadan participation - this is a good Vimto market. Present in many African countries for decades, the business model is to seed a territory with imported cans, and as critical mass is achieved to seek a local bottler partner. Vimto then launches new flavors that appeal to local tastes.

Negatives of this business: Africa is a hard place to do business. But what restrains competition can also raise returns. 4th generation Matt Nichols (now 41 years old) spent his thirties as African Area Manager 2011-2021, during which time this business grew spectacularly:

This is an example of one advantage of family ownership, with long-term brand-building requiring the quality which the famous investor Thomas Russo looks for:

"Africa represents a great opportunity for patient firms...I like family ownership because it gives a management team the 'capacity to suffer.'”[2]

Good: UK “Packaged” (50% sales). After 115 years of advertising and promoting the Vimto brand in the UK, there is a lot of latent value not showing on the balance sheet. Buffett teaches on the wisdom of owning brands (see appendix), especially during inflation due to the similarity to a royalty business. Vimto’s “packaged” business has outsourced all manufacturing to co-packers, dramatically improving returns on capital and reducing the employee base to just sales, marketing, and corporate. Group unlevered ROE 20%+ and ROA 12%+ since 2006 (except for pandemic years 2020-21 but resumed in 2022) I think demonstrates that this is a good business.

Negatives of this business: constantly changing consumer preferences mean this will never be a pure royalty check collecting business – instead requiring innovation and development of new flavors, products and packaging; 2016 Soft Drinks Industry Levy resulting in reformulation to lower added sugar; constant competition: Vimto has #2, 13% market share in UK squash, behind #1 Robinson’s 37% (Owned by Britvic, partner with PepsiCo) and ahead of #3 Ribena’s 7% (Suntory), and a large 30% private label, according to Nielsen data.

Terrible: UK Out of Home (“OoH”) (27% of sales). Zero positives to say about this.

Negatives of this business: Growing sales without regard for profit or capital is obviously foolish. So it was a terrible strategic decision to enter the business of bottling and distributing mainly non-Vimto brands (both owned and licensed) in pubs, bars, amusement parks and cinemas, requiring the current footprint of 16 depots and 1 factory – after the Group had realized after 100 years that its most valuable brand was made more valuable by leaving this hard, underpaid work to others! No further words should be necessary to describe how terrible this business is, and how much better the group would be without it - or anything like it - forever, by pasting the last two years' investor presentations which show some of the numbers which lay hidden in Group accounts, flattered by profits from decent businesses elsewhere:

Source: March 2022 investor presentation

Source: March 2023 investor presentation

Investing £54m – more than the operating capital required by the entirety of the three good to great businesses described above – to make losses is bad business.

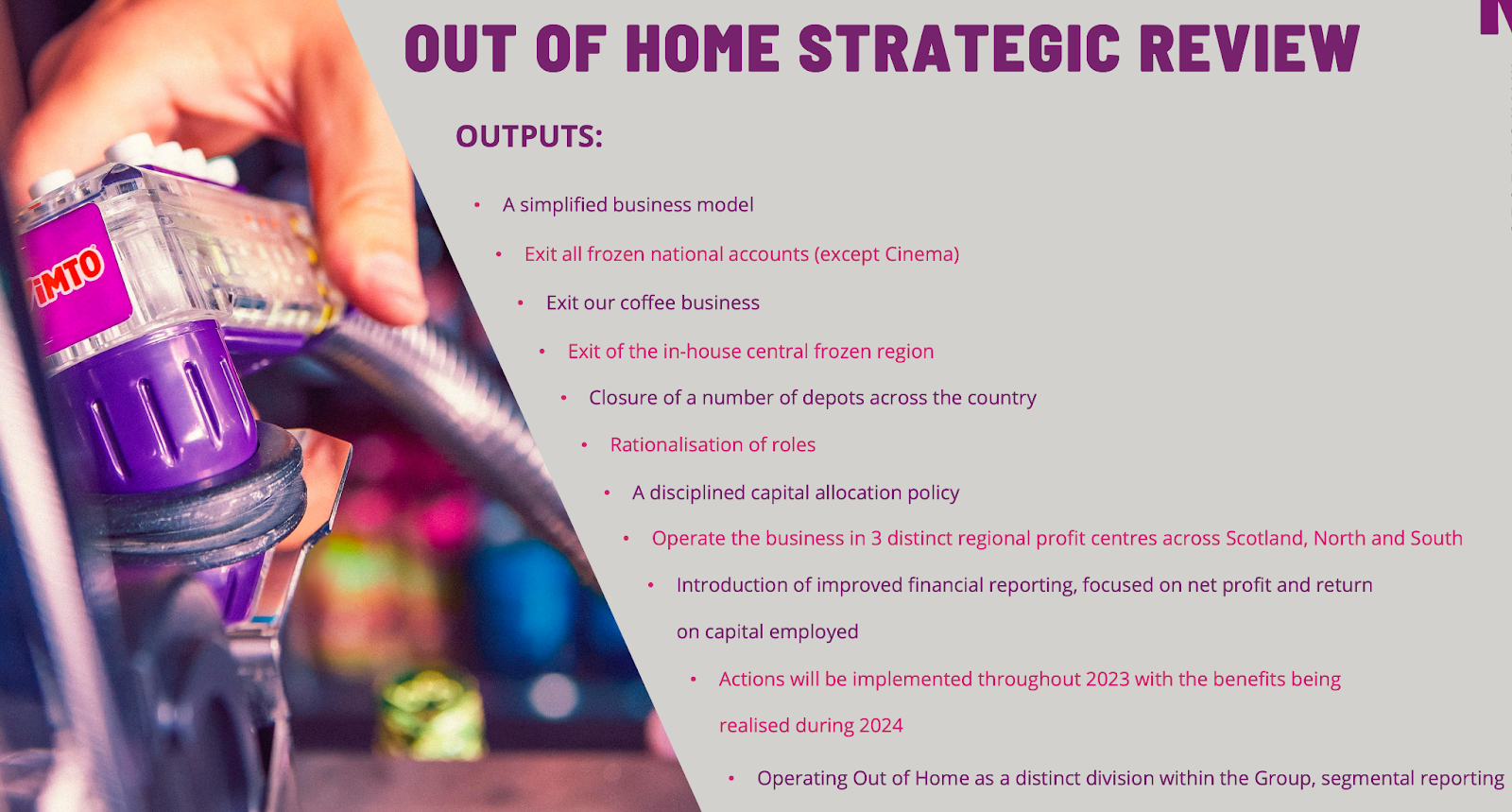

After the 2022 strategic review, it seems like management gets it:

Source: March 2023 investor presentation

My concern would be that they might not be ruthless enough in their actions. Segment reporting will change with the publication of the 2022 annual report shortly, as OoH gets reported for the first time. But why did it take 10 years and a pandemic to get here?

Management and the Board

I would not say that they are the best. They could be. But as a small, family business without access to the best strategic management brains which might be considered table stakes in US companies, management has blown hot and cold strategically over its long history. Brand quality has always been the north star, which is why it has survived. But a culture of constantly migrating to the highest economic value creation has been lacking.

How they deal with the OoH business now it has become clear how mistaken that strategy was, should I think be a good predictor of the likely quality of future decisions.

Though both the CEO and CFO from 2013-21 are no longer at the company, that CEO hired current CEO Andrew Milne as COO in 2013 from Coca Cola Enterprises (Northern UK). He has served on the Board since 2016. So now he needs to demonstrate an economic backbone.

CFO David Rattigan is new though, joining in March 2020, and so far, I have found him to be a rational financial strategist.

The best periods historically seem to have paired a strategically strong CFO with a CEO who understands the power of building the brand. For example, the 2002-2012 period of Brendan Hynes (CFO and later CEO) with John Nichols (executive, then non-executive chairman; founder’s grandson), when the company transitioned to an asset-light business model by outsourcing production to co-packers.

I am concerned about the board, especially since James Nichols (43 years old) was for several years a commercial director of OoH. That the two 4th generation brothers with long career runways ahead of them were simultaneously investing themselves in such radically different long-term value creation potentials (OoH and Africa), whilst their father John (who knows the business inside out after a half century there) continues as a non-executive director, is a bad sign to me. This is potentially an example of the downsides of family management: patchy talent, uneconomic thinking, inadequately reported results, lack of objective rigor.

Nevertheless, multi-generational family businesses bring both strengths and weaknesses. A long-term perspective to building valuable consumer brands is the key strength, which is supplied by the extended family’s 36% ownership of the stock - substantial these 115 years after founding. That ownership has endured despite all the changes seen in the business during this time: product composition, packaging, route to market, customer preferences, government influence. The one unchanging nature of the business, and what I consider its core skill, is marketing.

The marketing power of imprinting

Note: Impatient readers skip to paragraph beginning “Generations of Muslims…”

As sinister as it can appear, good marketers often use deep psychological techniques.

“Imprinting occurs when an animal forms an attachment to the first thing it sees upon hatching. (In the 1930s, the Nobel prize-winning Austrian zoologist Konrad) Lorenz discovered that newly hatched goslings would follow the first moving object they saw — often Lorenz himself. As a result, he was often trailed by a half-dozen waddling geese as he tended the grounds of his Austrian estate.”

Source: American Psychological Association, December 2011, Vol 42, No. 11[3]

In 1999 French conservationist Christian Moullec used Lorenz’s imprinting techniques to reintroduce dwarf geese into the wild by getting newly hatched birds to attach to him and his microlight aircraft:

“33 dwarf geese followed us on a long journey from Scandinavia to southwest Germany, where they wintered safely. They followed us and memorized a new route with us and replicated it the following year. They then went on this trip every year and taught it to their goslings.”

Teaching and bonding with goslings

https://www.youtube.com/watch?v=mrO4dvUest4

The Birdman - the man who flies with birds

https://youtu.be/ri7IDNT8vI0?t=85

The marketer’s job has less altruistic motives perhaps, but the same aims: to change behavior, and to make it habitual, even generational.

Coca Cola understands the power of imprinting, as anyone knows who has been offered a free cold one as a marketing promotion right at the point of entering a sports stadium or music concert. Consider: you have just battled through traffic and parking or crowded mass transit, you finally arrive at the arena and the moment of peak anticipation. A Coca Cola person hands you a free gift of a cold can, which they insist on opening for you as they hand it to you. Immediate consumption is assured by the opened can, not resealable bottle, right as you take those last few steps into the atmosphere of the stadium. Coca Cola has figured out that by linking your physical sensory and emotional memories in this way they can imprint a searing taste memory. Years later when you selected Coca Cola from an airport or gas station vending machine, who knew that you were trying to relive the emotional high of that night.

Generations of Muslims have been imprinted with the Vimto taste as it has become tradition to break the daily fast during the month of Ramadan with a drink of its sweet cordial. Hard to imagine for non-observers, the challenge of complete abstinence from all drink and food for the hours between sunrise and sunset for about 30 consecutive days leads to a powerful physical experience at the first drink of Vimto each evening.

This daily ritual imprints the taste even more strongly by combining the physical with emotional memories created by typically breaking fast as a family or community. Just as Coca Cola around the world intensifies its marketing around holidays such as Thanksgiving and Christmas, driving brand association with what are meant to be happy memories, similarly Vimto marketing in the Middle East maximizes the opportunity of what represents 30 consecutive Thanksgiving meals:

https://www.youtube.com/watch?v=3HBL4lkoVfo

In the company’s home market of the UK, Vimto has no huge marketing window to match Ramadan. But still their marketing skills are evident, as British kids attach to the Vimto taste through Vimto branded confectionary. Introduced in 2005 as brand extensions produced under license and at affordable retail prices, Vimto uses them not for profits but to “increase Vimto’s brand awareness among its core target audience”, i.e. children and young people.

In conclusion this is a marketing company. It has adapted over more than a century to numerous challenges yet keeps its products and most importantly its message relevant to the consumer. Current shareholders benefit from all the company’s past efforts to imprint its message on consumers, who might even teach their offspring the taste for Vimto for years to come.

Why is it cheap?

The bonfire of shareholder capital that was the 2013-21 OoH strategy, followed by a pandemic, should take some time, and demonstration of disciplined capital allocation, to woo shareholders back.

Appendix

Below are some further examples of company advertisements:

Seriously mixed up fruit (UK) - several variations on the original

https://www.youtube.com/watch?v=bsvvZia2m68

https://www.youtube.com/watch?v=Fdg9vNPDplQ

https://www.youtube.com/watch?v=wrWhtoJekmo

https://www.youtube.com/watch?v=DCLdS7mIZA0

https://www.youtube.com/watch?v=io23NDoW6nQ

I see Vimto in you (UK)

“You’ve described inflation as a gigantic corporate tapeworm. Which of Berkshire’s businesses are best suited to thrive during a period of high inflation and why? Which will suffer the most and why?”

WARREN BUFFETT: Yeah. Well, the best businesses during inflation are usually the best — they’re the businesses that you buy once and then you don’t have to keep making capital investments subsequently…

So, any business with heavy capital investment tends to be a poor business to be in in inflation and often it’s a poor business to be in generally.

And the business where you buy something once — a brand is a wonderful thing to own during inflation.

You know, See’s Candy built their brand many years ago. Now, we’ve had to nourish it as we’ve gone along, but the value of that brand increases during inflation, just as the value of, really, any strongly branded goods.

Gillette bought the entire radio rights to the World Series in 1939. And as I remember, it cost them $100,000, and for that they got to broadcast the Yankees, I think, versus the Reds in 1939.

And think of the number of impressions they made on minds in 1939 dollars for $100,000, and they were getting in the minds of young guys like myself. I was eight or nine. And millions of people — and they did it in those dollars then.

And, of course, if you were going to go out and try out and do — have similar impressions on millions of minds now, it’d cost a fortune. And part of that is due to inflation. Part of it’s due to other things.

But it was a great investment, which could be made in 1939 dollars that paid off, in terms of selling razors and blades in 1960 and 1970 and 1980 dollars.

So that’s the kind of business you want to own.

Valuation Notes

2022 free cash flow (£ 000s):

16,336 Net cash generated from operating activities

7,025 adjust for change in working capital

(1,245) Acquisition of property, plant and equipment

(995) Payment of lease liabilities

4,300 Adjustment for HMRC cash payment (once-off tax settlement)

_____

25,421 FCF

Capex ran below depreciation in 2022 after years of overinvestment in OoH segment. Using depreciation instead results in 23,140.

[1] Source: UNPD World Population Prospects 2019

[2] https://medium.com/graham-and-doddsville/tom-russo-capacity-to-suffer-is-critical-3f48a607bd8c

[3] https://www.apa.org/monitor/2011/12/imprinting

I and/or others I advise do not hold a material investment in the issuer's securities.

Catalyst

John Nichols (founder's grandson, current Board member) held months of takeover talks in 2007, after which he said:

"There is no 'for sale' sign up here. When someone comes to you with a price, you have to have a look. Everything has a price."

source: https://www.manchestereveningnews.co.uk/business/business-news/no-vimto-takeover-1004425

| show sort by |