Description

LSB Industries Inc. (LXU US)

February 2018

LSB Industries (“LXU”) is a nitrogen fertilizer and mining chemicals producer with a $200mm market cap, but which trades in sufficient volume to be actionable for many funds (~$3mm daily volume traded).

The back story of this 50 year old company is quite interesting. I recommend reading BlueViper’s August 2015 writeup and associated comments as context. A lot has occurred since that point, not least of which, a 70% drawdown in share price.

The thesis here is simple: LSB is a risky levered equity stub with potential for a takeout amid improving industry fundamentals and strengthening publicly-traded peer “currencies”. As with any good levered stub, there’s significant upside mitigated by large balance sheet risks, and thus deserves a small position sizing.

LSB has historically been plagued with crippling cost overruns, delayed project completions, blatant nepotism, bang-your-head-against-a-wall operational issues, and acts of God. It’s even recently been plagued in the biblical sense. But the company has survived via rescue financing, asset sales, and a changing of the guard. At the end of the day, these are assets that *should* be able to generate $160mm in EBITDA given today’s Tampa ammonia and natural gas prices, assuming the plants achieve acceptable on-stream rates and that the company is consuming spot gas.

For this type of earnings power (there’s no consensus according to Bloomberg, and I don’t have access to Sidoti, the only firm that covers the name) the company has a fully-loaded Q3 enterprise value of $740mm. So the company is trading at 4.6x something like today’s EBITDA potential. This compares favorably to CF which trades for 12.4x/10.7x this/next year’s Bloomberg consensus EBITDA. CVR (ticker: UAN) and Yara (YAR NO) both trade at approximately 8x this year’s EBITDA.

Note that the company’s El Dorado, AR plant went through a major expansion project which only wrapped up in 2016 and cost ~$800mm alone—net of capitalized interest. While clearly the gem of the portfolio (which isn’t saying much), El Dorado is one of LXU’s four plants and represents approximately half of the company’s ammonia output. One relevant question might be whether the entire company is at least worth the build cost of El Dorado. Note that, when it's running, El Dorado regularly outputs well-beyond nameplate.

The company has two major problems with its balance sheet. First, as part of rescue financing done in late 2015, Security Benefit (part of Guggenheim) owns 140K shares of Series E 14% cumulative, redeemable preferred stock which currently carries a $179mm liquidation preference and is PIKing (due to a lack of cash generation of late, as well as a 2:1 fixed charge coverage ratio governing the RP basket of the company's Notes which is not currently met). Second, the company has $375mm in 8.5% Senior Secured Notes maturing 8/1/19 that the company may have challenges refinancing given the unreliability of on-stream rates.

Given the operational and financial challenges the company has faced, the business has essentially had a “for sale” sign around its neck for the last few quarters. But the problem has been that during this time, nitrogen fertilizer has been out of favor with investors, and it appeared that certain publicly-traded strategics either didn’t have the multiple in their currencies or had publicly committed to de-levering. My guess is Koch is interested, but in order to not get fleeced, LXU would need one other interested party who’s serious.

I firmly believe the company would be worth more in the hands of a strategic. First, significant overhead would go away. Second, fertilizer production and distribution benefits from scale (procurement, logistics, transportation, etc.) and depth of regional presence. Third, someone like a Koch or CF probably has the talent available to run these assets more reliably than they are currently run. There have been some questions over CF’s ability to acquire LXU’s assets from an antitrust standpoint, but management doesn’t think it’d be impossible.

I believe that given improving industry fundamentals and market sentiment, along with the PIKing time bomb that is LSB’s balance sheet, management will be very focused on selling the company. This is a management team that surprised the market by selling its HVAC assets in 2016 for $364mm, more than anyone expected (14.5x trailing EBITDA). It’s also been actively selling other small non-core assets. Also note that LXU’s CEO, Dan Greenwell (who I deem a straight shooter), was CFO of Terra during its [wildly overpriced] sale to CF in 2010.

Management feels it can address the refinancing of the bonds during 1H 2018, but my take is this will be contingent on lenders getting comfortable with the future reliability of the assets. I note that the bonds trade just above par, and are callable at 101.9 until 8/1/18, and par thereafter.

As for the 4th quarter (company reports 2/26 after close), EBITDA will likely be slightly negative given downtime, repair expenses, costs to fulfill orders via 3rd parties during downtime, and other one-offs. But eyes should be on the Q1 and FY outlook for product pricing as the Tampa index is up nicely from where it was when they hosted the Q3 call on 10/31, and as the effective prices customers pay begin to catch up to the upswing in the index (slight lag).

Below is a chart that outlines the gross profit (based on my own recipe) in converting spot nat gas to a ton of Tampa ammonia, compared to an unlagged LXU stock price. If you were to shift the stock chart component (orange line) to the right, you’ll notice shares aren’t [yet] seeing the benefit of recent industry tailwinds.

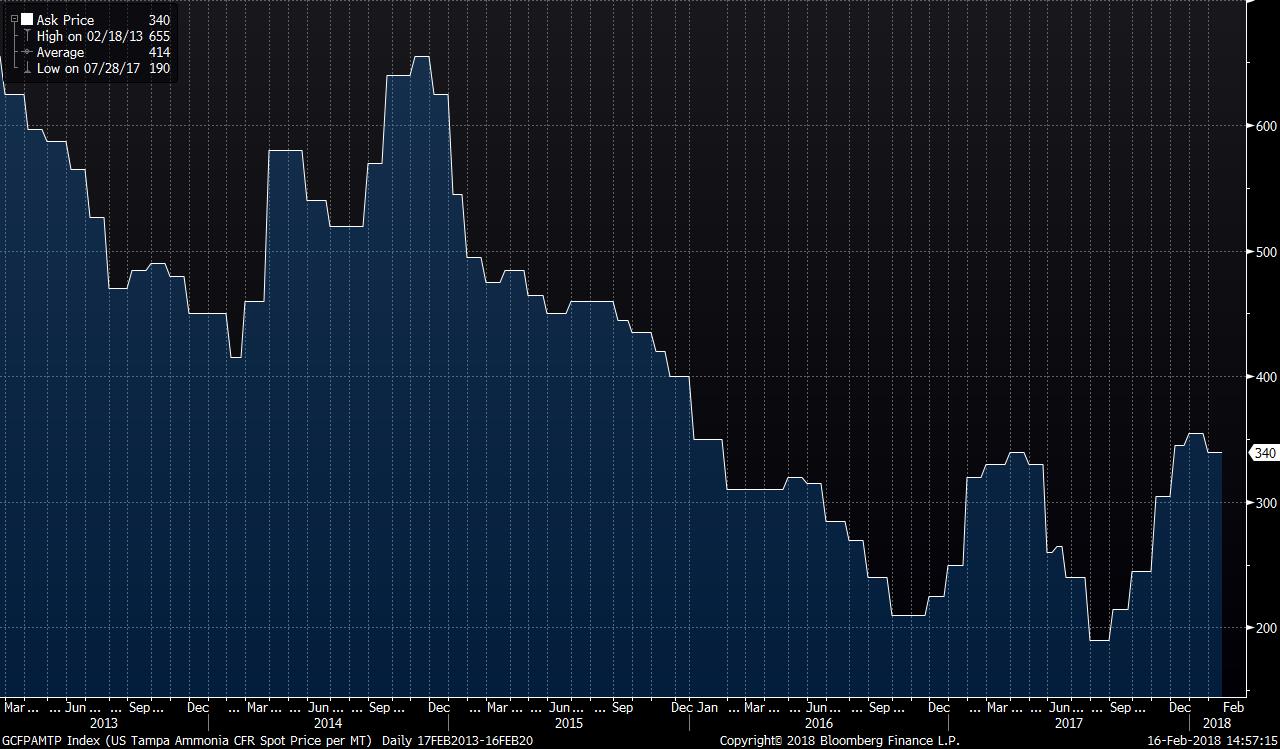

And here’s a 5 year chart of Tampa ammonia:

I do not hold a position with the issuer such as employment, directorship, or consultancy.

I and/or others I advise hold a material investment in the issuer's securities.

Catalyst

Increased on-stream time for Pryor and El Dorado, HY bond refinancing, sale of the company, partial calling of the pref