| 2021 | 2022 | ||||||

| Price: | 10.50 | EPS | 0 | 0 | |||

| Shares Out. (in M): | 205 | P/E | 0 | 0 | |||

| Market Cap (in $M): | 2,100 | P/FCF | 0 | 0 | |||

| Net Debt (in $M): | 0 | EBIT | 0 | 0 | |||

| TEV (in $M): | 0 | TEV/EBIT | 0 | 0 | |||

Sign up for free guest access to view investment idea with a 45 days delay.

- SPAC!

Description

Overview:

The Hillman Group (ticker: LCY today, HLMN soon) is a pretty boring, low growth business on the surface. It is being overlooked because of its route to market and business profile.

Hillman is being acquired via a SPAC - a now crowded field difficult for many investors to effectively sift through. The nature of the business did not excite either retail investors or the new cohort of SPAC investors looking for high growth or high profile investments. And the deal is closing just as the market sours on SPACs. In other words, the perfect setup…

But for those looking through the noise of the transaction close and willing to do some work on merits, HLMN offers a unique opportunity for value minded investors to buy a stable, quality, profitable business with good growth and very low multiples. I see a reasonably conservative case to $20/share (from $10.50) in about 18 months. So while this may not be the rocket ship like some other SPACs, HLMN may prove that the tortoise can beat the hare (or insert other intentional mixed metaphors).

Background:

Hillman is a key supplier of high consumable and small products to a range of hardware retailers. Hillman sells nails, nuts, bolts, other fasteners, gloves, keys and other related items to Home Depot, Lowes, Walmart, ACE and a variety of other hardware and home supply stores.

On the surface there isn’t anything particularly compelling about this business or the products sold.

But Hillman has proven to be a solid, consistent business for a long time. In fact, the company has grown organically in 55 of 56 years since its founding. It survived the financial crisis and housing market crash of 2008 and the covid recession in 2020 very well (grew sales and/or EBITDA through the downturns in both instances). Looking just at their sales history, it’s hard to identify economic cycles or housing cycles (not that they don’t have impact, just that the business manages well through them - not growing too fast, and not falling when activity slows).

The Moat:

What makes the Hillman business today most compelling is its distribution. Hillman employs 1,100 sales and service reps in the field with their retail customers. They have become the DSD partner to HD, LOW, and Ace Hardware delivering nuts, bolts, picture hangers, etc. and managing the category for their customers. Hillman is the Pepsi or Coke of the hardware and home improvement world. Retailers rely on Hillman to stock shelves and keep inventory managed, making them a valuable partner and extremely difficult to replace. And Hillman can leverage these national accounts as they grow their own brands and expand into new brands and categories.

An additional moat for Hillman is the product categories tend to be e-commerce resistant. Nuts, bolts, screws, etc. tend not to be high on the radar for Amazon purchases for obvious reasons. Also, DIY weekend warriors tend to bundle Hillman products with other materials to complete projects and professionals tend to pick up Hillman products as part of their daily or weekly runs on the way to job sites. Neither of these occasions are at high risk of e-commerce disruption.

The Relative Financials:

The Hillman moat and value to customers translates to solid financials versus other building product or distributor peers. Hillman generates among best in class gross margins and EBITDA margins versus traditional distributor peers, despite significantly higher revenue concentration with key customers for Hillman - which demonstrates the value provided.

The Business Opportunity:

As a public company, Hillman can grow with its categories, expand its brands to adjacent products and continue to drive value through additional rollup opportunities.

Grow with the categories

Home improvement categories generally continue to grow at GDP+ rates consistently. Since 2001, the industry has compounded at ~4% annually with 2 down years (2008-2009), surviving a housing boom and bust cycle and a slowly recovering housing market.

Expand to new adjacent categories

Hillman has identified a number of potential categories and products for expansion to leverage its brands and distribution relationships. Given current revenue of ~$1.5B and a ~$45B addressable market, there should be plenty of opportunities for expansion across its brand portfolio for any reasonable investment time period.

Bolt-on acquisitions can drive meaningful incremental value

Hillman can bring national distribution, enhanced category management, and sales support to brands to provide meaningful value to acquisition candidates. Two recent larger deals demonstrate the power of successful M&A for Hillman. BTP was bought for $345m and PF multiple paid was reduced from ~10x EBITDA to 5X EBITDA based on performance in the first 26 months. In a similar time period, Hillman lowered its effective purchase price of MinuteKey from 17x to 7x EBITDA.

Transaction:

The SPAC:

Lancadia Holdings III (LCY) is the SPAC acquiring Hillman. They have announced a transaction to buy Hillman Companies in a transaction that is expected to close this quarter. Lancadia Holdings is co-chaired by Richard Handler of Jefferies and Tilman Feritta of Golden Nugget and Landry’s. They had a hard time with WAITR their first deal, but have done better with GNOG, their second SPAC together.

De-SPAC Transaction:

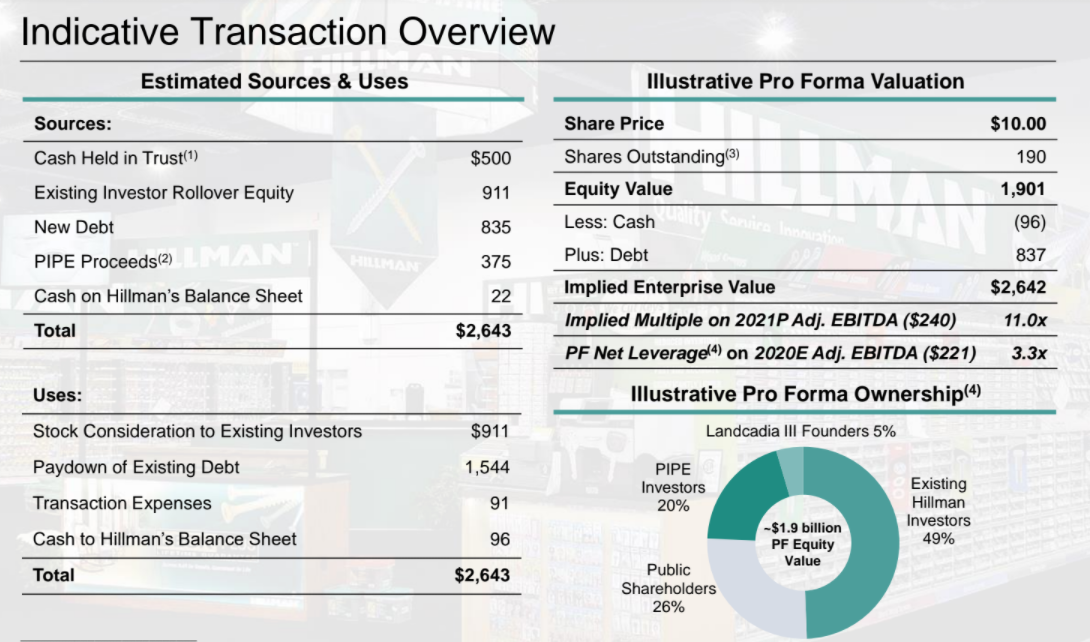

The LCY SPAC has $500M in trust and is adding $375M of PIPE to de-lever Hillman as it transitions from a private equity portfolio company to a public equity. The sponsor is not taking any dividend or selling any stock as part of the transaction and is instead rolling its equity.

On deal announcement the company presented the sources & uses and pro forma capitalization as follows (which is essentially the same as the stock is still about $10/share).

Actual pro forma capitalization will depend on the amount of trust that redeems shares for cash or converts to Hillman shares.

Pro forma for the deal, Hillman will be approximately 3x levered. As a private equity portfolio company, the company operated with substantially more leverage and clearly has the capacity to do so for the right mix of acquisition opportunities, though the management team appears more interested in lowering not raising leverage levels in the near to mid term.

Financial Projections:

Hillman has provided the following financial projections with the transaction:

Valuation:

For the reasons stated above, Hillman valuation should benefit from consistent revenue growth, stability through macro cycles, leading margin profile, large rollup opportunity, and less risk from ecommerce.

A framework to think through valuation consistent with most here is an ~18 month view. Hillman should generate ~$300m of EBITDA by 2023 (potentially faster with more acquisition). @ 15x EBITDA, this implies $4.5B of EV and ~$4B of market cap, again depending on pace of acquisition this could accelerate but with more net debt. The company has approximately 205m shares outstanding, so HLMN can trade to $20/share by year end 2022 - a double in a little more than 18 months.

Historical and current framework of valuation for industrial distributors suggest that 15x EBITDA is fair, despite less ecommerce risk embedded in Hillman.

And multiples of other stable rollups in the building products space suggest 15x EBITDA may be too conservative.

Using a range of 13x (trough multiple of last 5 years for building product peers and multiple of lower quality peer GWW in distribution) to 25x (current multiple of other building product peers with worse margins) generates a range of valuation of $15-30/share. This suggests 50% to 300% potential, depending on how the market chooses to value this business.

I and/or others I advise do not hold a material investment in the issuer's securities.

Catalyst

De-SPAC in Q2

Reported financials through 2021 and 2022

| show sort by |