| 2018 | 2019 | ||||||

| Price: | 2.44 | EPS | 0.22 | 0.24 | |||

| Shares Out. (in M): | 202 | P/E | 11.1 | 10.2 | |||

| Market Cap (in $M): | 493 | P/FCF | 10.5 | 9.8 | |||

| Net Debt (in $M): | 17 | EBIT | 65 | 70 | |||

| TEV (in $M): | 510 | TEV/EBIT | 7.8 | 7.2 | |||

Sign up for free guest access to view investment idea with a 45 days delay.

- None found

- BETA

- FIVE BELOW INC FIVE 04/08/2020

- SLEEP NUMBER CORPORATION SNBR 08/21/2018

- PARTY CITY HOLDCO INC PRTY 10/20/2019

- DOLLAR GENERAL CORP DG 02/02/2019

- Grocery Outlet Holding Corp GO 01/09/2023

- GROCERY OUTLET HLDNG CORP GO 09/28/2021

- Big Lots, Inc. BIG 08/02/2018

- Bell Atlantic/Verizon VZ 04/07/2000

- CARTER'S INC CRI 11/04/2020

- Sky Network Television SKT 07/06/2021

Description

Kathmandu – A highly mispriced, leading vertically-integrated brand in specialty outdoor retail, with sustainable growth post-restructuring. Strong competitive similarities and lessons from The North Face (TNF), the global best-of-breed. And major tipping point with Oboz acquisition to transform into a global powerhouse brand.

Kathmandu is the leading outdoor adventure retailer; apparel and equipment specialist in Australia (AU) and New Zealand (NZ). It possesses strong moats in this niche - with its highly functional products, and support from being close to the needs of the outdoor community. This reduces the risk of disruption from new entrants in the generalist and cross category space (Amazon, Decathlon, H&M).

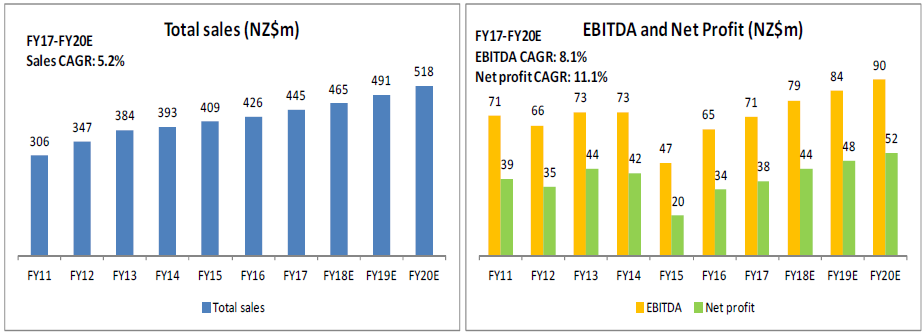

A strong indication of its brand equity is its ability to consistently price products at a huge premium to generalist competitors – similar to TNF and Patagonia. At NZ$2.20, FY18 (Y/E in July) is just 10x P/E, 5.5x EV/EBITDA, 5.5% dividend yield, earning 16% cash ROA, with 7-9% earnings growth in the next 5 years. It is priced at >50% discount if we look at recent acquisitions like MacPac. And the US-brand Oboz footwear acquisition is a major tipping point to transform it into a multi-bagger with a long growth runway (Look at commentary). If the revenue synergies with Oboz are executed well, we are likely to see ̃15% sales growth over the next ten years, at its current absurdly low valuation. The investment thesis as below:

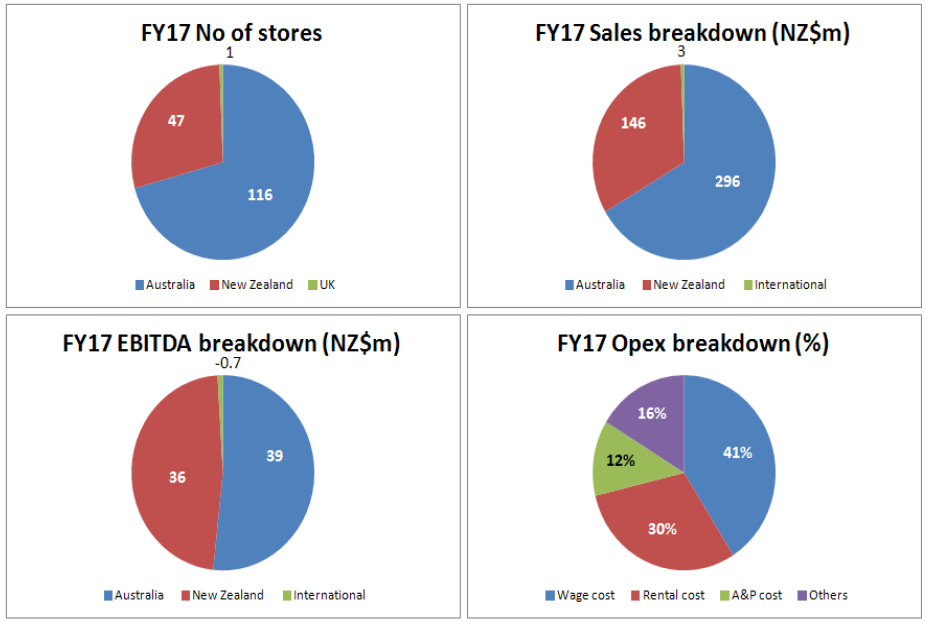

1. Leading vertically integrated brand. Kathmandu is the largest outdoor specialist brand in AU and NZ, with 12.5% share in the growing but fragmented AU market. The NZ market is mature, and here its revenue is >2x the second largest specialist, Macpac. As one of the few vertically integrated brands in this niche, it owns key parts of the supply chain – it sources technological fabrics and components, at volume and prices fixed per order to avoid overstocking. It owns its distribution centers and 95% of its products are original designs and contract manufactured (85% from China). There is heavy emphasis on design innovation with the team in NZ expanding from 10 to >60 in the last eight years.

2. Strong cost competitiveness. Besides the obvious advantages of vertical integration - original and highly functional products, control over product lead time, distribution efficiency and store inventory control, many do not fully appreciate its strong cost advantage that few retailers can match. >60% of its sales are derived from Christmas, Easter and Winter when it offers heavy promotions at 40-50% discount, yet it is able to earn a minimum 58% GPM during these 3 seasons, with a healthy overall FY 62-63% GPM (similar to luxury brands). Other retailers trying to match its promotions with the same high extent of sales seasonality will make huge losses, given retail markup at only 30-40%. And this promotional model is necessary, same as TNF and Patagonia, because customers buy on impulse for vacations (everyday low pricing is infeasible given its non-commoditized nature and low volume). Kathmandu is well known for its high quality and broad range, but is considered expensive. These promotions reinforce the concept of scarcity (removed from shelves after the season) and high value to its customers.

3. Strong functional differentiation that attracts the growing urban affluent. Just as TNF and Patagonia did, Kathmandu builds its functional brand image very carefully by sponsoring expeditions & top athletes in this niche, getting them to test and improve its new products, focusing on environmental sustainability, and fostering a social community on its online website and social media by encouraging user generated content etc. This empowers such brands to price their newest design down jackets at $500 (Uniqlo sells at <$100), backpacks at >$200 (Samsonite at half the price). TNF and Patagonia go one big step further by focusing on the hardcore mountaineering niche – a 2-metre tent at TNF designed for punishing conditions on the mountain peak costs $5,500 (Kathmandu’s highest priced tent at $1,800), an inferno sleeping bag from TNF at $730 keeps explorers warm in a -40C climate, at Petagonia for $530 you get a neoprene-free, natural rubber, hooded wetsuit for use in water temperatures down to 0C. While these high-end products belong to the long-tail, they promote a halo effect to mainstream sales such as down jackets. And the secret recipe is selling them to the growing urban affluent who only camp at the mountain base once a year, but wear them daily for walks in the park to reinforce the experience. It is really not that different from Nike and Adidas. Importantly, due to the versatility and multiple functions of its products, customers require detailed demonstration from well-trained staff, and this is a strong barrier of entry to online brands.

4. Highly recurring sales from its Value Summit Club. An invaluable asset is its Value Summit membership club. Implemented since 2008, membership accelerated particularly in recent years as the new management targeted promotions at its members, with 1.8m active members in 1H18 (the largest in its niche; Macpac has only 0.33m, Anaconda has 2m but it is really a generalist department store). Value Summit contributed 67% of revenue in FY15 when it had 1.4m members, and it’s likely to contribute >70% recurring sales now given faster membership growth than sales. This membership base provides important data on repeat purchases, and fosters a stronger community bond as members are informed of new products through emails, about its organized expedition trips, encouraged members through incentives to input product feedback (almost every online featured product has user reviews), and post user content such as expedition videos and photos to share experiences.

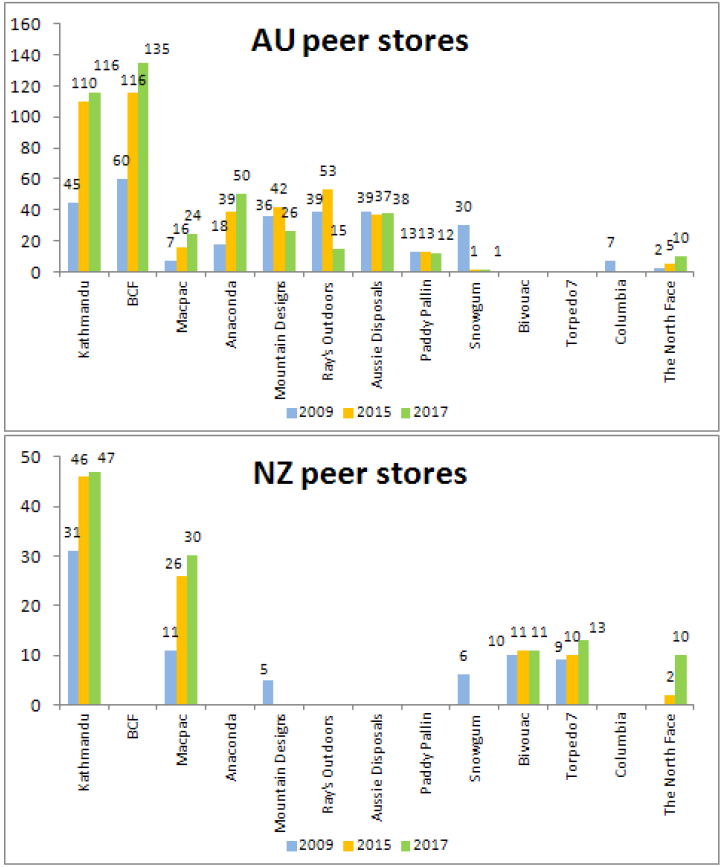

5. Consolidation opportunity as the AU competition weakens. Investors are worried the Australian retail has slowed down since emerging from the mining crisis two years ago, while rents continued to climb due to scarcity of prime space. However, this has turned into an opportunity for Kathmandu. Although it faced higher rental costs, its biggest competitors are forced to scale down significantly or shut down. Ray’s Outdoors, Mountain Designs and Snowgum are such examples. Among its AU peers, only Macpac and Anaconda are growing in the past two years. With 12.5% market share in AU, Kathmandu is likely to become the prime beneficiary of industry consolidation as it did in NZ and the US – in the US, TNF commands 36% share and Patagonia at 20%.

Since 2014, there is a major shakeup in the industry after its crazed expansion followed by the mining crisis. It became apparent that a strong brand is needed to survive, and vertically integrated players have the edge of clearing stock quickly to refresh their brand.

6. Successful turnaround since 2015. Under the previous management installed by the PE fund, which listed the company in 2009, FY15’s dismal net profit dip of -52% is a result from patchy execution of rapid store growth (90% more stores since IPO in 2009), and an attempt to ramp up SSSG through increasing store SKUs by 30% in just a short span of 2 years. High sales seasonality also magnified the issue of inventory overhang and pressured GPM once the systems couldn’t keep up.

Since Jun 15, with the new management team and new CEO, Xavier Simonet, the ship is steered back to sustainable growth at 4-5 new stores per year vs. 15 new stores previously. The determination to clear outdated store inventory saw 2H15’s GPM recover by 70bps y-o-y after 3 painful quarters. More importantly Xavier, who has a strong background in brand management from Radley, DB Apparel and 11 years at LVMH, prioritizes brand distinctiveness through engineered products, less discounting and membership growth.

7. Sustainable growth opportunities. On the strategic front, its AU expansion is at the mid-stage with a potential network of 180 stores vs. 116 in FY17. By focusing on smaller format stores in high traffic malls, its potential was increased from 140 stores previously. But this also requires careful execution; since opening 4-5 new smaller stores cannot support unnecessary overheads. On the other hand, these stores are closer to its target urban affluent customers, and they provide a higher level of service for functional products, which a large store at 1500sqm cannot do.

Internationally, it is pursuing an asset-light wholesale model and online platform to expand in Europe (Tmall in 1H18). Online has reached 7.5% of sales and is growing at 15-20%, a proportion way higher than most Australian retailers who are playing late catch-up. The wholesale model in Europe is an enormous opportunity as we see from TNF’s history. It held European trade shows last year to showcase its distinctive products, with contribution to start in FY18. Autumn/winter orders are shipped to European customers, with initial spring/summer 2018 order received. Product-wise, Kathmandu can learn from TNF by expanding its skiing and footwear range (which is very limited) as it penetrates Europe, and notching up to highly-functional products for hardcore mountaineers.

AU should sustain 5 to 6% sales growth in the next 5 years with operating leverage. 1H18 guidance at 4% sales growth from new stores; despite SSSG declining -0.8%, due to NZ’s unusual -6.4% SSSG.

8. Unfairly penalized valuation. Kathmandu has emerged as a stronger and more sustainable business post-FY15, but FY17 NPAT is still 10% below the FY14 peak – because then retail conditions and rapid expansion were propped up by the mining boom. Misunderstood, it is priced at FY18 10x P/E, 6.8x EV/EBIT or 5.5x EV/EBITDA, which is >50% discount to fair value.

In 2015, the Briscoe failed acquisition for Kathmandu is an illuminating case – Briscoe is a leading NZ homeware retailer that is aware its growth opportunities are very limited. It tried to pass a low ball at NZ$1.80, pricing Kathmandu at forecast FY16 9x EV/EBIT or 7x EV/EBITDA (which is still higher than current valuation multiples), after the latter took a 52% NPAT nosedive. As expected, Kathmandu’s Board and shareholders rejected the bid, because they believe its strong vertically-integrated brand should trade at 12x EV/EBIT or 9.4x EV/EBITDA (supported by peer comparisons from the independent valuer). Super Retail Group, one of the largest retailers in AU, recently acquired Macpac for FY18 9x EV/EBITDA. Super Retail even made a statement that it has determined the most viable strategy in the outdoor adventure space is to acquire, synergize and grow a brand with deep product know-how and support from the community. An educated guess is that Super Retail would be very eager to acquire Kathmandu at >12x EV/EBIT or >10x EV/EBITDA, given there is no other that comes close to its leadership in this niche.

Company background

Kathmandu has a storied history which sheds valuable insights. In 1987, Jan Cameron and co-founder Bernard Wicht started their first store in Melbourne, followed by their first store in NZ in 1991. From the start, Kathmandu was a small specialist outdoor retailer which manufactured many of its products, and its complexity and range improved throughout the 1990s; by 2002 it became a full vertically-integrated retailer with sufficient scale to access quality materials at a lower cost than competitors.

A common thread between Kathmandu, TNF, Patagonia and Macpac (at a later stage) is that the founders are outdoor fanatics who have a good understanding of why functional, effective products are so necessary to their customers. Jan Cameron started by making sleeping bags because she couldn’t accept the market was offering prehistoric products. However, these founders are conflicted because they preferred the outdoors than running a company, and their strong views on environmental sustainability conflict with their success due to consumerism. As a result, many have sold out and even Patagonia’s founder, Yvon Chouinard, the reluctant businessman wished he had sold his business. Therefore, Yvon instilled a strong company motto – “Let my people go surfing” (referencing to the Exodus by Moses); to make products that are highly functional, durable and environmentally friendly to compensate for consumerism. This has been the cornerstone that reinforced the brand over the years.

In 2006, Jan Cameron sold Kathmandu to a PE consortium for NZ$275m, which subsequently listed it in 2009 on both ASX and NZX at a market cap of NZ$426m (NZ$2.13 per share), priced at 9x EV/EBITDA. The IPO proceeds were used to completely buy out the PE fund’s equity and pay the company’s debts, rather than beefing up the company’s resources. Peter Halkett, the MD and CEO then, was appointed by the PE fund since 2006 and remained post-IPO till 2015.

During his tenure, the company focused obsessively on top-line growth - through rapid store openings, rebranding >70% of stores that were opened just 2-3 years ago, accelerated retail staff hiring, upsizing store SKU by 30% within two short years, and haphazardly started its UK store operations which were loss-making until they were closed down by FY17. From FY09-15, 74 new stores or 90% more stores were opened, mostly in Australia along with the industry frenzy. There was a lot of pressure to perform to growth targets, as seen in the FY10 report; where Peter explained that the company couldn’t meet forecast in the prospectus, because it would risk too much inventory clearance and damage the brand.

Moreover, his compensation was mainly tied to EBITDA growth, in the belief that investments would pay off eventually. To understand his philosophy, Peter was previously the CEO of Pacific Retail Group, a US retail property manager. He might have viewed it more from a monetization perspective, rather than a LT brand building tedious process which requires choosing the right battlefields carefully.

Since the company was sold to the PE consortium in 2006, there is a legacy $122m goodwill and $149m brand value recognized using the purchase accounting method (it is asset light since it doesn’t own stores). Its main shareholders are: Briscoe Group (19.8%), which still holds onto its ownership despite the failed takeover as it recognizes the strategic value of the company. And a number of fund companies such as UK-based TA Universal (12%), AU-based Novaport Capital (7.5%) and Challenger Limited (7.6%), and NZ-based Harbour Asset Management (6.1%).

Sustainable growth post-restructuring in FY15

In Jun 2015, Xavier and the new management team came aboard. Compensation has changed towards EBIT growth. The key strategy shifted towards brand differentiation through improving functional design, reducing store clearance and growing its membership. International expansion will take on an asset‐light model through wholesaling in Europe and investing in the online platform.

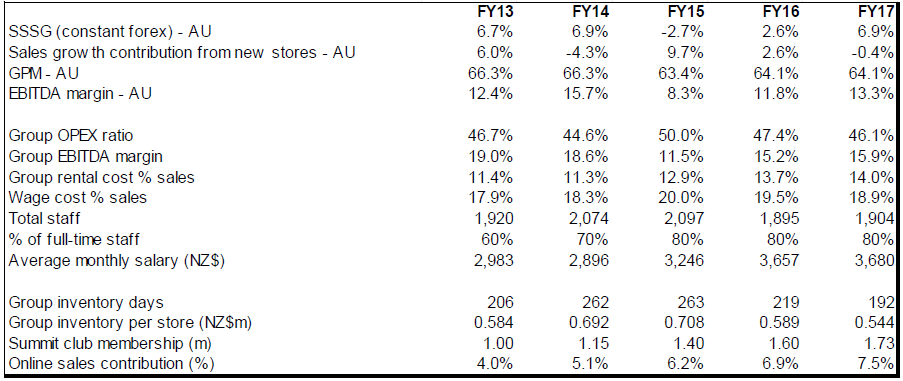

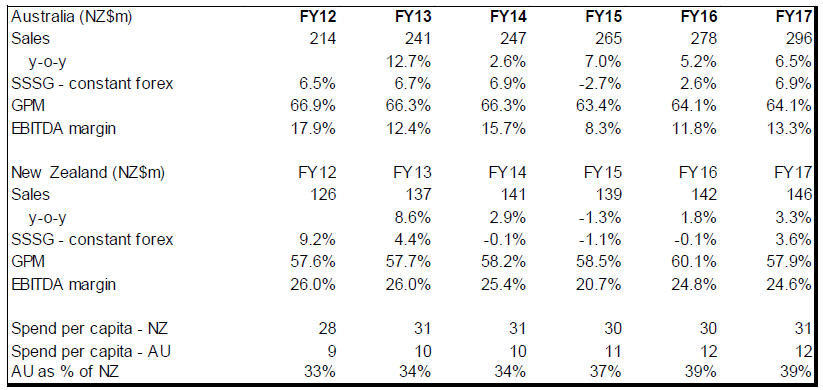

Post-2015, many of its largest competitors in AU have scaled down significantly or closed down. Kathmandu’s results as shown above indicate a strong recovery, and a more sustainable business post-restructuring. Focusing on AU (where the downturn was more significant), its biggest improvements are SSSG and EBITDA margin (driven by operating efficiency). This is in light of a moderated pace of new stores, and a subdued GPM LT target (revised downwards from 62-64% to 61-63%), due to a slow retail market recovery. However, its high GPM at >60% (similar to high-end luxury brands) is an indication of its cost competitiveness as a vertically-integrated brand, against retail peers at ̃35-40% GPM.

At the group level, management has driven down the opex ratio and increased EBITDA margin - through raising store sales and optimizing retail labor and advertising cost (targeted only towards promotional seasons and shifting spend towards more effective online channels). However, EBITDA margin has not returned to its peak level due to rising rental cost.

This rental cost ratio should improve from FY18, due to operating leverage from a slower store rollout and higher utilization of its new mega distribution centre in Melbourne (which leases land in an industrial development). Importantly, wage cost ratio has come down, despite the percentage of full-time staff growing from 60% to 80% and average salary higher by 27%. As mentioned earlier, customers require detailed demonstration from skilled staff to justify purchases of its functional products.

Lastly, inventory has reduced significantly both in turnover and on a per store basis. Inventory days at 6-7 months is considered healthy, given 60% of product mix comes from apparel (which refreshes every season), and 40% from equipment which can last more than a year. The new management has also done well to accelerate both the Summit Club membership and online contribution growth in recent years.

Business model elaboration

Although AU GPM is 6% higher than NZ (higher prices in general), its EBITDA margin is about 10-11% lower than NZ. This is because basic salaries are ̃9% of sales in NZ compared to 14% in AU. Rents are also higher in AU and most leases have automatic increases. An important metric which management monitors is the country spend per capita, where AU is only 39% of that in NZ, the latter being a mature market. Management is targeting AU to reach 60% of NZ when the store network reaches its potential 180 outlets. It also symbolizes the extent of competition and Kathmandu’s brand equity in Australia.

Kathmandu’s products are in outdoor apparel (60% of sales from 65% in 2009), and equipment (40% from 35%). Apparel includes: waterproof jackets, down jackets, thermals, fleece jackets, shirts & pants, Merino apparel, footwear. Equipment includes: packs, bags, sleeping bags, footwear, tents travel accessories, camping accessories. Among its products, functional down jackets, travel packs, bags & accessories and sleeping bags prove to be most popular. Products are also segmented into three price points and features – for the young emerging professionals, professionals with families, and the retirees. This is similar to luxury brands initiating new customers with entry-level products.

It owns two state-of-the-art distribution centers, a 7,800sqm in Christchurch and 25,000sqm in Melbourne, which are invested to support the full 180 potential store network in AU, future wholesale and online demands. As a comparison, Amazon’s first AU distribution center in 2017 is 24,000sqm.

It doesn’t do wholesale nor franchise in NZ and AU, therefore it has complete control over display merchandise and inventory. 80-90% of its material purchases are in USD, hence it hedges AUD/USD and NZD/USD on a forward 12-month basis (but not AUD/NZD, where there is translational fluctuations). Online sales started in 2008 and grew to 7.5% in FY17, but most of it comes from NZ and AU currently. I believe a two-pronged wholesale and online model is necessary to penetrate the European market.

Neither is Kathmandu making specialized gears that have a high element of safety risk. These include ropes, carabiners & harness, belay device, ski bindings, ski and trekking poles etc. There are a few companies that invest heavily in these, such as the French hidden champion Petzl, Dynastar for skiing, Black Diamond and to some extent, The North Face (TNF). It is astute not to dip its toes into this tough business; Patagonia’s founder set up a separate equipment company which later faced multiple lawsuits from safety breaches. It went into receivership, was acquired and renamed as Black Diamond.

However, Kathmandu can learn from TNF by notching up its apparel and equipment to cater to hardcore mountaineers under more challenging conditions, and improve its skiing and footwear product range. This will reinforce its reputation as an outdoor specialist that the urban affluent are attracted to.

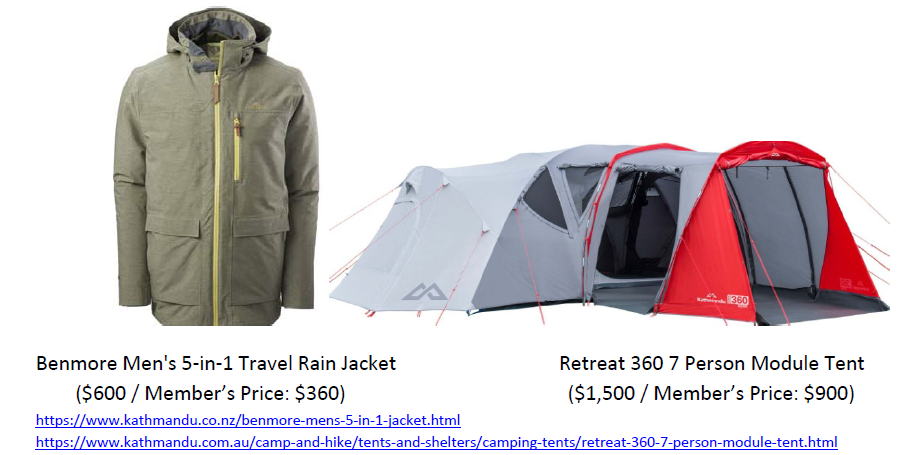

The above are examples of functional products from Kathmandu. The Benmore Jacket can be worn in five ways: down jacket, down vest, waterproof outer jacket, waterproof outer with vest zipped in, waterproof outer with full down jacket zipped in. This makes it very versatile for different conditions of wetness, temperature and breathability.

The 7‐person module tent is designed to maximize the amount of interior space and headroom, while protecting the structure with a strong waterproof flysheet, durable fiberglass poles, insect‐proof vents/doors/windows, magnetic lighting and solar charging ceiling. It even has a unique controllable cooling ventilating system. Kathmandu sources unique combinations of materials for different products; it also has a wide range of Merino wool apparel which originates from NZ and AU. Merino wool is known for its breathability, ultra fine fiber which feels soft on the skin, and is lightweight and heat‐insulating.

Competitive landscape turning favorable

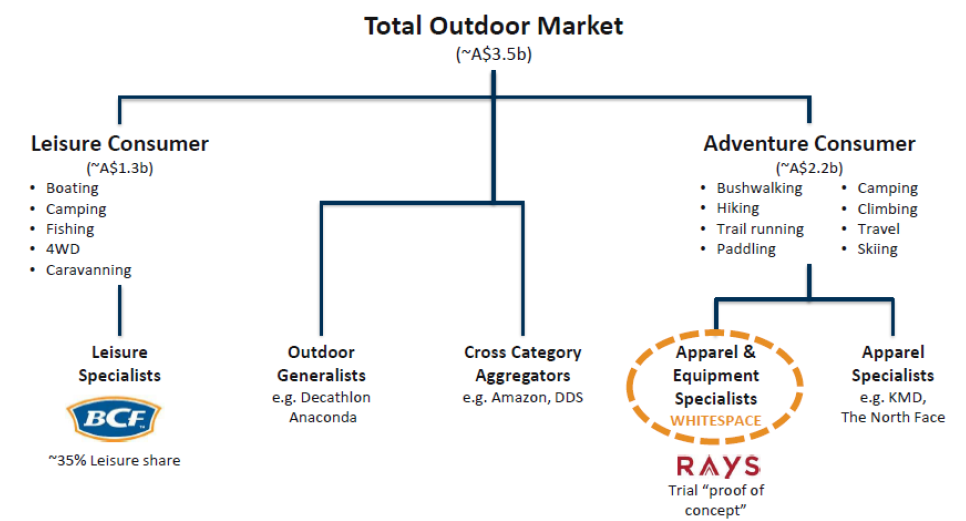

Source: Super Retail Group 1H18 presentation

The Australian outdoor market is estimated at A$3.5b, where adventure makes up A$2.2b and leisure at A$1.3b. Adventure and leisure have very different product and customer mix. The adventure consumer is the urban affluent or the hardcore outdoor enthusiast, who is willing to pay for highly functional apparel and equipment, to enhance their adventure experience. The leisure consumer lives in suburban areas and treats boating, camping, fishing or caravanning as their way of life. Therefore, the leisure consumer views demand as a necessity, rather than an aspirational want. Naturally, the adventure consumer goes for impulse buying and product turnover is higher. Kathmandu’s AU business commands a 12.5% share in the adventure segment, which has been growing at ̃5% in the past decade.

Since 2015, its largest competitors in AU such as Ray’s, Mountain Designs and Snowgum have downsized or shut down. Kathmandu’s biggest competitor is Super Retail Group (SUL:AU), which acquired BCF in 2004 for 5x EV/EBIT, Ray’s Outdoors in 2010 for 7.2x EV/EBIT, and MacPac in Mar 18 for 9x EV/EBITDA. However, in terms of brands, only MacPac comes close to Kathmandu’s brand image and specialty.

Looking at this sector’s history, the important lessons we learn are: (1) There are high barriers to entry in the adventure segment - product know-how, brand equity and support from the community. (2) The adventure segment cannot compete on price, especially since strong generalists and cross-category aggregators will disrupt in volumes. (3) The adventure segment is cyclical (though less than general retail), and brands are not bullet-proof. They can be destroyed if they lose their differentiation and premium image. (4) The high barriers to entry also limit synergies with brands from other fields.

Super Retail Group holds an assortment of brands including Super Cheap Auto which sells auto parts, general sporting brands like Rebel Sports, BCF (Boating, Camping and Fishing) with 35% share in the leisure segment, Ray’s Outdoors is a large-format (1,500sqm) store chain selling mostly camping equipment (35%), outdoor apparel (27%) and outdoor equipment (15%) with the rest being general merchandise. It sells both its own brands and third party brands, though it has now transitioned into pure retailer selling third party brands. Lastly, it acquired MacPac, after years of unsuccessfully trying to turnaround Ray’s by leveraging on BCF’s systems and management. MacPac focuses more on apparel than Kathmandu, at 76% vs. the latter’s 60%, and equipment at only 24% vs. the latter’s 40%.

To begin with, BCF is really not a competitor to Kathmandu. Its suburban customers will not pay a premium for camping equipment, and they are looking for a one-stop shop of value products that are deemed a necessity for their way of life. Service quality is important, where BCF is considered a part of their suburban community. BCF is estimated to earn ̃6% EBIT margin, less than half of Kathmandu’s 13-14%. It is clear that Ray’s is lacking in every aspect that BCF’s customers are looking for, which makes any synergies very limited. It was initially hoped that Ray’s could complement BCF through its own brand product know-how, particularly in apparel, since BCF sells mainly national brand equipment.

However, Ray’s never had a strong enough brand differentiation nor the required service level. And due to the uniqueness of the adventure segment, there were no synergies in sourcing or customer relationship management. In FY17, Ray’s has downsized to 15 stores from 53. Ray’s exited a number of categories, such as fishing, workwear, BBQ equipment, caravan accessories. Since FY16, it focused on selling third party outdoor brands like Patagonia, Jack Wolfskin, Mountain Safety Research – SSSG turned slightly positive, but it also means a lower GPM now as a pure retailer. It continued to make $7m loss in FY16 and $6m loss in FY17, leading to the downsizing.

Super Retail is hoping that MacPac can turnaround Ray’s and leverage on Ray’s remaining 15 store network to grow its Australian store presence (where MacPac has 24 stores in AU vs. Kathmandu at 116). MacPac shares a very similar business model as Kathmandu, because they underwent the same history. In 2008, MacPac was sold to three outdoor enthusiasts who decided to convert from a wholesale model to a retailer in order to improve its brand image. In 2011, Jan Cameron (Kathmandu’s founder) acquired MacPac and turned it into a vertically-integrated model. Its sourcing, contract manufacturing and functionality focus are very similar. Even its premium pricing and price categories take after Kathmandu.

Except that it is currently >10 years behind Kathmandu in terms of scale, product range & innovation. In 2015, Jan Cameron sold Macpac to Champs (PE fund) for A$70m at 7x EV/EBITDA, which was re-sold to Super Retail for A$135m at 9x EV/EBITDA. This means that in the last two years, Macpac achieved 12.5% sales CAGR from a low base, and 15.5% EBITDA CAGR; the higher profit growth is very likely the result of aggressive cost-cutting by the PE fund. Yet, Macpac’s FY18 sales and EBITDA are only 20% of Kathmandu! Its membership base at 330k is also a far cry from Kathmandu’s 1.73m. And I doubt there are much synergy between Ray’s and Macpac, since Macpac thrives on designing its own functional products, whereas Ray’s has turned into a fledging department store with a high cost structure.

Similar to Ray’s, Mountain Designs also operates a large store format, selling both own brands and third party brands, but the latter is more category-focused in hiking, rock-climbing and general outdoor. Mountain Designs exited its NZ cash cow business to pursue growth in AU, but a similar story of rapid growth followed by the mining crisis led to three years of price discount fatigue. Unlike Kathmandu, it is more of a generalist than a specialist, and it doesn’t have sufficient vertical control to stamp out excess inventory quickly. It was reported to make $7m loss last year and has downsized to 26 stores, from 42. Aussie Disposals is a generalist selling camping and hiking equipment, blue collar workwear and military and hunting apparel and gear. Similar to BCF, its customers are mostly suburban.

Besides Kathmandu and Macpac, Anaconda is the only peer that managed to grow after the 2014 mining crisis. Anaconda belongs to the Spotlight Group, a large discount retailer that owns retail properties. Anaconda operates a much larger store format (>2000sqm), selling a very broad range of categories such as kayaks, fishing equipment, general sports, bicycles, outdoor apparel & equipment. It only sells third party brands, such as MacPac and The North Face in the adventure category (Kathmandu doesn’t do wholesale in AU and NZ). Anaconda appeals to the rookie outdoor fan who hasn’t pledged brand loyalty. As a discounter it is cheaper, especially since most of its products belong to the entry level price category. It is a pure generalist discounter, hence it appeals to a very different customer. However, this strategy may be disrupted by the likes of Amazon and Decathlon in the coming years.

Finally, The North Face stores in Australia are run by independent partners, who also carry other brands such as Ray’s and Bivouac. Just as Kathmandu makes Europe a priority instead of the US, TNF is also unlikely to compete head-on in AU or NZ where there is a dominating retail competitor - since retail is the main building block for selling functional adventure products.

Similarities and Lessons from The North Face

In 2000, the big break came for both TNF and its acquirer, VF Corp (VFC:US). VFC bought TNF for merely $25m, with annual revenue of $240m. Despite having a strong brand, TNF was facing intense cost competition from cheaper overseas bases, and it was run to the ground by intense channel-stuffing and a series of costly mistakes.

After restructuring its manufacturing overseas and reducing stock clearance, TNF’s sales went on to compound at 19% CAGR to FY12, or 15% CAGR to FY17 at $2.4b with over 200 stores. As VFC grew from $5.7b to $11.8b over this period, TNF (this once minor acquisition) contributed 37% of its dollar growth. Priced at 24x P/E, VFC’s premium stem mostly from TNF and Vans’ brand equity and their growth.

With $2.4b global revenue and $1.45b from the US, TNF commands 36% market share in the $4bn US outdoor market, with Patagonia at 20% share. Given the AU outdoor market is way more fragmented (Kathmandu at 12.5% share), Kathmandu stands to benefit as the prime beneficiary of consolidation. TNF earns ̃17-18% EBIT margin, higher than Kathmandu’s 13-14% as the latter has yet to realize its operating leverage, after investing in a series of smaller stores, new distribution centers and IT systems.

The global adventure lifestyle market is estimated at $25b, where Kathmandu makes up only 1.3%. Therefore in the global arena, Kathmandu has far from realized its brand potential. We see important similarities with TNF, as well as opportunities for Kathmandu to scale up like the global champion:

a. Preserving functional image. TNF’s motto is “Never stop exploring”, and the brand represents pushing the limits of design so that enthusiasts can push their limits outdoors. TNF also designs the snow apparel for Vans which became very successful. Even though it profits from the faster growing urban affluent, through Summit Shops that sell more apparel than gears; it treaded this fine line carefully by focusing on functionality and connecting closely with the outdoor community. This is important because the casual wear market is very fickle. Part of TNF’s strategy is to open stores with different formats, such as mountaineering and skiing stores, flagship stores, Summit Shops. This avoids brand dilution, but also requires a broad enough product range and differentiation in the specialist and mainstream segments. Kathmandu can learn by notching up functionality for the hardcore market. Even though these products belong to the long tail, it will strengthen its specialist identity both locally and overseas.

b. Broaden product range. As mentioned above, Kathmandu has plenty of room to improve its limited skiing range and footwear. By 2005, TNF realized its footwear sales were growing rapidly and soon making up 1/3 of total sales, as consumers seek greater differentiation in functionality for various terrains in outdoor training & adventure. But this requires doubling its R&D team, adding category-specific sales people and launching targeted marketing and stores with higher footwear mix. We estimate footwear at ̃10% sales for Kathmandu (4% for Macpac). Footwear and skiing products have a big market in Europe, and Kathmandu cannot let up this opportunity.

c. Wholesale opportunity. Wholesale trials to Europe just started in 1H18, but this is too big an opportunity to underestimate, for a functional brand like Kathmandu. TNF generates 62% of sales from wholesale: where 37% of sales from international markets and the remaining 25% from US wholesale. It sells through specialty outdoor, premium sporting goods stores and selected department stores. Even Canada Goose, which sells pricey parkas, gets 70% of revenue from wholesale. Why are these brands able to leverage so much on wholesale? It is because retailers like department stores prioritize sales per sqft – this means expensive brands that are high in demand give them the highest profitability. Of course, wholesaling comes with a host of challenges, where channel stuffing or counterfeits (less likely in Europe than in China) can damage a brand. But for Kathmandu, this is unexplored territory and sales tend to pick up very fast once the systems are in place. It is an asset light model with very promising growth.

d. Online platform growth. Unlike its generalist peers, TNF views Amazon enthusiastically as its partner in the US. TNF started a dedicated key account leader and team in the US working with Amazon, mirroring their model in Europe. The key is to understand how to sell better through Amazon’s platform, help them understand its brand better, and collaboratively clean up the unauthorized dealers. In the same way, Amazon is going to help Kathmandu in Europe. Although Kathmandu is making 7.5% of sales through online with ̃15% growth (vs. retail at 5% growth), it can do better. Its Australian retail peers are lagging far behind, with JB Hi-Fi leading the pack at 3% of sales from online. But TNF with its bigger base is making 9% of sales from online and growing at 20% CAGR. TNF leveraged the digital marketplaces in Europe, and it is far more advanced in digital/mobile payments including WeChat in China, click and collect model, social media content etc. It is also augmenting hologram projection on iPads to demonstrate equipments like tents which are not placed in smaller stores. We believe a two-pronged approach in wholesale and online complement each other well to expand into Europe.

Commentary on recent Oboz US footwear acquisition - Major Tipping Point to become a multi-bagger with long growth runway

This acquisition is a pleasant surprise that is likely a major tipping point for KMD to become a multi-bagger. Importantly, it points to two of the main points I've made in the report: (1) Wholesale channel is an enormous opportunity for KMD, as we see from TNF and Canada Goose where this channel contributes 62% and 70% of sales respectively. (2) Footwear is a very promising product category that KMD must capture, and this acquisition has nailed it. Footwear is the fastest growing product category for TNF and has reached >33% of sales, while KMD has only 7.8% and MacPac 4% from footwear. Moreover, footwear is a highly complementary product that draws frequent customer visitation to retail stores and are less seasonal (compared to its main product down jackets). (3) Overall, KMD has chosen the right target, but the terms of the acquisition could be improved - I'll explain later.

Oboz is acquired for NZ$110m or FY18 10.6x EV/EBITDA or ̃13.4x P/E. 45.5% of the acquisition price is to be funded through equity issuance at NZ$2.16 per share (increase share count by 11.5%), with the remaining 54.5% through debt.

The Oboz brand is founded in 2007 by three outdoor fanatics with deep understanding of the functional needs of their customers, and close relationships with third party retailers. It is a full vertically-integrated brand that sells mostly through wholesale in the US - a majority are authentic specialty outdoor adventure retailers, and limited online and general sportswear retailers. There is a earn-out clause that requires Oboz to earn NZ$10m EBITDA in FY18 (54% increase over LY), with NZ$21.5m (of the total NZ$110m price) in escrow. Oboz's revenue and EBITDA were ̃10% of KMD in FY17. It is a fast growing brand with sales CAGR of 40% for the last four years. If we take TNF's estimated footwear sales as a reference, Oboz is only 9% of the former, hence it's still a fairly small niche brand at the high growth stage.

Post-acquisition on a FY17 pro-forma basis, footwear makes up 15.8% of the enlarged sales vs. 7.8% previously, US will become a new market with 8.3% sales contribution, and wholesale at 8.9% contribution. It isn't a minor acquisition since it amounts to 25% of KMD's market cap before share issuance. Therefore, the business model and risk profile certainly change significantly after the acquisition.

Oboz has significant footwear product development experience, sourcing and R&D capabilities. It designs and sells a broad range of footwear for backpacking, hiking, travel, winter and general outdoor wear. The brand resonates strongly with the hiking enthusiasts group due to its design authenticity, quality, fit and comfort, and corporate social responsibility image. It is particularly known for its O-FIT insole, a proprietary insole design customized for each model based on large data collected from the makeup of feet, to provide strong protection and shock absorption for rough terrains. Its defining features are its cushioning and durability, and a high supportive arch and deep cushioning heel cup. Based on US user reviews from forums discussing outdoor adventure, Oboz is generally acknowledged for its unique focus on outdoor functionality, but its protection features come close to being podiatric; some are unused to such firm insoles for daily purposes.

KMD has chosen the right target because they share many similarities in terms of culture, a strong vertically-integrated and highly functional brand. (1) Beyond that, Oboz's main customers, the authentic specialty outdoor adventure retailers, are the gateway for KMD to wholesale its portfolio and notch up its overseas image as a specialist brand. The US wholesale channel is a huge market as we can reference from TNF. (2) Also, KMD can now invest in A&P for Oboz in AU/NZ to increase brand awareness and grow its footwear sales. (3) KMD can also accelerate its learning curve on wholesaling from Oboz, especially in terms of choosing the product range to introduce, the customers to work with, how to optimize brand investment with its downstream partners, and controlling wholesale inventory which is much harder. (4) The broader portfolio and brands means that it is better positioned to penetrate the wholesale channel in Europe, which has a big market for outdoor footwear. (5) KMD has been working with Oboz for a long time as its biggest international partner, therefore it has a good sense of the management reliability.

However, I believe some terms of the acquisition could be better: (1) At NZ$2.16 issuance price, KMD is >50% undervalued at 5.5x EV/EBITDA while the acquisition price for Oboz is decent at 10.6x EV/EBITDA. This means there will be quite a dilution for existing shareholders. (2) More importantly, the earn-out clause is too short term with only FY18 target; usually it's set on milestones over a 3-5 year period. As a pure wholesaler, it is really not difficult to meet sales target by channel stuffing or introducing new product launches. (3) As noted, a key risk is that Oboz's top management leave, because they hold deep product know-how and close relationships with customers. The short term earn-out clause certainly doesn't help here, and it is known that these outdoor enthusiasts prefer returning to the outdoors than staying in the office. (4) Oboz valuation may be considered on the high-side looking from its standalone entity; if we consider its business model vulnerabilities - it is a single product category brand without retail as its sustainable building block, it derives 45% of revenue from a single customer, and it relies on just 2 parties (likely Pou Chen and Feng Tay, both have strong bargaining power) to manufacture its products. But if we consider the revenue synergies with Kathmandu which will make Kathmandu a much stronger brand, this pivotal acquisition is well worth it.

The key risk is losing Oboz's top management. But I believe that overall, this is an important tipping point for KMD that is likely to create a long growth runway. As a comparison, TNF grew at 15% sales CAGR from to US$240m in 2000 to US$2.4b in 2017.

It’s a welcoming change to see Xavier and his team embracing acquisitions as a growth engine, rather than relying solely on organic growth in the company's history. KMD's previous management tried to accelerate organic growth in a way that's haphazard and short-term focused. In contrast, the new management has wisely chosen an asset-light overseas expansion strategy in wholesale and online rather than retail, which is too risky as shown by the closure of its 5 UK stores initiated by the previous management. And now it uses these savings to invest in a very compatible target that will strengthen KMD on the geographical, product and channel distribution fronts. To me, it demonstrates good strategy and resource allocation.

It is still too early to comment what kind of growth rates we are expecting from Oboz, though I believe it's multiples of KMD's organic 5% sales growth. The important things to look out for will be KMD's international sales and profit growth, how quickly it pays back the additional debt with FCF, and whether it is able to increase Oboz brand sales in its AU & NZ retail stores, which is also very promising.

I and/or others I advise do not hold a material investment in the issuer's securities.

Catalyst

(1) The Oboz footwear acquisition, which will strengthen KMD on the geographical, product and channel distribution fronts. Kathmandu is no longer just a highly undervalued strong brand with sustainable 7-9% earnings growth and 5.5% dividend yield. It has reached a major tipping point to become one of the leading global outdoor brands like The North Face, with possibly >15% earnings growth for the next 10 years, using an asset-light international expansion strategy.

(2) Kathmandu is a highly desired takeover target, as seen by Briscoe retaining its strategic 19.8% stake despite the failed takeover in 2015. And I believe many retailers will be very interested to integrate this highly functional outdoor brand. As Super Retail Group puts it (which acquired Macpac, Kathmandu's main brand competitor), the most viable strategy in the outdoor adventure space is to acquire, synergize and grow a brand with deep product know-how and support from the community. The barriers to entry are too high to start a new brand to compete against leaders like Kathmandu or The North Face.

| show sort by |