| 2016 | 2017 | ||||||

| Price: | 11.25 | EPS | 0 | 0 | |||

| Shares Out. (in M): | 32 | P/E | 0 | 0 | |||

| Market Cap (in $M): | 361 | P/FCF | 0 | 0 | |||

| Net Debt (in $M): | -39 | EBIT | 0 | 0 | |||

| TEV (in $M): | 322 | TEV/EBIT | 0 | 0 | |||

| Borrow Cost: | General Collateral | ||||||

Sign up for free guest access to view investment idea with a 45 days delay.

- Fortissimo Bagging

Description

Investment Thesis

Kornit Digital (“KRNT” or the “Company”) is an Israel-based producers of garment printers that IPOed at $10 per share under the JOBS Act a little over a year ago. It sells its printers and ink principally to custom t-shirt shops and smaller design companies. Facing decelerating growth and increased competition in this core market, management has convinced investors that KRNT can keep its growth story going by successfully entering the higher-end garment printer market with a new printer it is “developing,” the Allegro. This printer has, in fact, been in a state of perpetual development. People do not seem to realize KRNT first launched the Allegro in 2011 and have yet to sell a single one. Regardless, this is a market with a totally different customer set (large commercial fabric companies), in a new geography (Asia) that is dominated by several much larger incumbent producers that offer a more attractive value proposition to customers. Revenue deceleration, inability to scale, weak quarter-to-date import data and unfavorable channel checks indicate the Company is challenged and make KRNT a very attractive short with a +50% near-term return potential and 75% return over the next year.

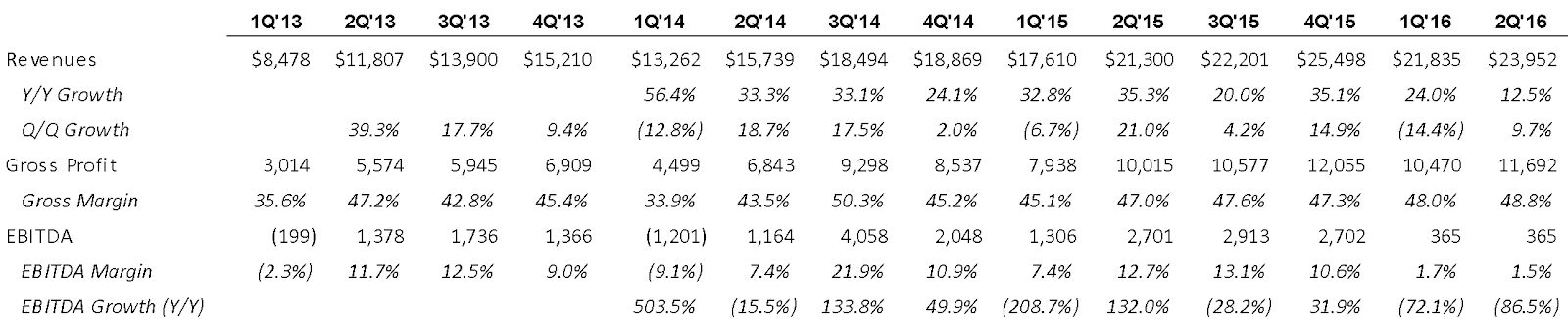

Kornit’s growth has decelerated meaningfully in 2016 with sequential revenue growth of -14% and 9.7% in Q1’16 and Q2’16, respectively. Over the last three quarters management has blamed performance shortfalls on timing and they were expecting “a very strong second half” and “a strong third quarter.” Now KRNT is banking on 2H’16 yet customs data indicates only one shipment containing eight Avalanche printers has been received in the US since June 30. This implies only $3.2M in revenue at MSRP. Contrast this with expectations of +30% annual revenue growth and the fact that zero Allegro printers have arrived. The credibility of management’s guidance is questionable. They have proven to routinely embellished facts and make cryptic statements. Earlier this year, the CEO Gabi Seligsohn said KRNT was “in advanced stages with a large DTG customer” to be there “global provider.” There has been no mention of this prospective customer since and when asked about it last month, he changed the subject. KRNT has recently run back up from its lows earlier this summer and now trades at 51x LTM EBITDA and 3.9x LTM revenue. Meanwhile, last year, EFII acquired the industry leader in textile printing, Reggiani, for less than 10x EBITDA.

Catalysts

The primary drivers of this outcome include: 1) revenue shortfall in Q3 leading to guidance cuts from the current lofty expectations; 2) increased competitive pressures leading to price cuts, margin decline and market share loss; 3) failed entry into R2R and very limited adoption of Allegro printer; 4) stock re-rating as its challenges are illuminated; and 5) potential share sales from Fortissimo Capital.

Business Background

Kornit was founded in 2002 and is headquartered in Israel with all production currently taking place in that country. The Company was acquired by Fortissimo Capital for $16M in 2011 and was inauspiciously brought public on April 1, 2015. KRNT develops, designs, and markets direct-to-garment (DTG) digital inkjet printers and corresponding ink for the global textile industry. These are machines that enable the printing of designs and patterns onto fabric. The technology is essentially a more complex form of that used in conventional desktop inkjet printing. The primary users of the products are custom decorators and made-to-order garment printers (e.g. personalized t-shirts).

Approximately 65% of revenue came from the US, 23% from EMEA and 13% from the Asia Pacific. 72% of sales are through third-party distributors, only 28% of sales are direct. Kornit sells eight models of DTG printers targeting both higher and low through-puts, with ASPs ranging from $69K to $425K. Kornit’s printers can print on a variety of materials ranging from cotton, wool, denim and polyester (but not on dyed polyester or nylon). Printer sales and support account for approximately 60% of sales and ink for 40%. Although Kornit is placing less emphasis on its entry-level models, its Breeze model accounts for ~70% of the Company’s installed base and the majority of the new units sold. The patent protecting this printer expired last month.

Industry Overview

In DTG printing, an inkjet printer is used to print directly on a textile, often consisting of patterns or images. DTG printers are primarily used for small, short-run prints hence their popularity amongst custom t-shirt stores. The competitive landscape amongst DTG printers is intense, with Brother, Epson, Anajet, Kornit and Aeoon Technologies leading the pack with a dozen or so niche/ regional operators. At the high through-put segments, Kornit competes against Aeoon as well as traditional analog manufactures. Currently the DTG installed base stands at 35,000 printers with Kornit consisting of around ~1,200 units implying a 3.5% market share.

The roll-to-roll (R2R) market is much larger than that of DTG as R2R is focused on printing on fabrics which are converted into finished garments on a commercial scale. In R2R printing, rolls of fabric are passed through a wide inkjet printer that prints images and patterns on the fabric. Such uses include wallpaper, furniture fabric, and mass produced clothes. The industry is led by MS Printing Solutions (Dover), Konica Minolta, Reggiani Macchine, Durst and traditional analog manufacturers.

The digital textile printing industry according to Smithers Pira estimates global revenue of digital textile printing equipment and ink will grow at a 15% CAGR from 2016 to 2019 (from $1.2B to $2.6B in 2019). These projections are inclusive of both DTG and R2R applications. The R2R is expected to be relatively flat over the next several years, while the DTG market is smaller and growing faster. This ambitious growth is predicated on a continued mass demand for customization and personalization. Management guidance and the current stock price are implying KRNT will grow at over 2x this rate.

Investment Rationale

The bull thesis is predicated on Kornit generating strong top-line growth driven by its unique product and attractive secular trends among its potential customer base. The following details the inaccuracies of the bulls’ suppositions:

-

Intensifying Competition & Weak Position: Kornit operates in a highly competitive DTG inkjet printing space, competing against Brother, Aeoon, Epson, Neoflex and many more. Kornit’s products have been noted to be of good quality, but are priced at the high end of the market. Several competitors offer printers at materially lower price points. Epson’s F2000 printer sells for ~$17k versus Kornit’s Breeze at $70k yet the two have nearly equivalent performance specs and output. Epson’s F2000 was first released in 2013 and only became more broadly available last year. Now most any distributor or printer salesperson you speak with will recommend an F2000. This may explain Kornit’s meager 3.5% current market share. Further competitive disadvantages include:

-

Kornit’s products cannot print on dyed polyester or nylon.

-

Kornit’s entry level Breeze printer will be rolling off patent at the beginning this year.

-

Among the sales representatives consulted, all recommended competing DTG printers such as Epson and M2 versus Kornit due to price and ability to print on dark dry fit.

-

At $620k, KRNT’s Allegro R2R product is at a price disadvantage to traditional analog methods such as screen carousels. More on Allegro below.

-

Slowing DTG Growth: Kornit’s growth has decelerated meaningfully in 2016 with sequential revenue growth of -14% and 9.7% in Q1’16 and Q2’16, respectively. Now KRNT is banking on 2H’16 yet ImportGenius data indicates only one shipment containing eight Avalanche printers has been received in the US since June 30. This implies only $3.2M in revenue at MSRP. Contrast this with expectations of +30% annual revenue growth and the fact that zero Allegro printers have arrive yet.

-

Advocates for the Company purport that the proliferation of “fast fashion” will drive demand for Kornit’s printer. While it is true fast fashion retailers aim to release new collections every month versus traditional retailers who generally have 4 – 5 collections, Kornit’s printers are not the optimal solution versus current analog options. This is due to fast fashion’s positioning as a low cost producer, which does not meld well with DTG/R2R printers which carry higher production costs versus traditional methods. In the over half a decade that Kornit’s technology has been on the market, the only adopters have been custom t-shirt designers and smaller scale garment companies. This fact provides pretty clear evidence of Kornit’s value proposition and potential.

-

Entrance into R2R: After facing intensified competition in the DTG space, which caters to custom t-shirt printers, KRNT has attempted to go upstream into the R2R inkjet space, which does not print on t-shirts but fabric/textiles directly. The Company’s future growth hinges on a successful roll-out of Kornit’s R2R Allegro printer. The sell-side is willfully ignorant and fails to realize that Kornit actually announced its entrance in the R2R space with the Allegro in 2011. In the ensuing four years, the Company has not gained any traction outside of a handful of customers who are in beta tests. To date, the Allegro printer has been predominantly tested with small custom designed fabric, giftwrap and wallpaper designers, not high volume textile manufacturers servicing the likes of H&M and Ralph Lauren. Moreover, Kornit expects to roll-out this product in 18 months. Simply said, Kornit is late to the market as larger peers already dominate the inkjet R2R space, notably Konica Minolta’s Nassenger series, Durst Photechnik, Dover/MS Printing Solutions and Reggiani.

-

It has been reported that some of KRNT’s Asian customers that use the Breeze have experienced periodic ink shortages. Such downtime would be catastrophic for a commercial customer. KRNT’s lack of servicing and distribution infrastructure add major operational risks to prospective Allegro users. Konica Minolta, Durst Phototechnik Dover and Reggiani each have global services and sales personnel in place. KRNT has 49 employees dedicated to service and support globally, 85 total employees outside Israel and only 25 people in its single Asia office. Significant amount of incremental operating expense will be required if KRNT wants to compete. On the last earnings call, management blamed its inability to sell in Asia on macro-economic conditions in region.

-

Limited IP and Undifferentiated Technology: Kornit only has seven US patents that will begin expiring next year. At least two of these patents were acquired earlier this year for only $2M from Polymeric Imaging. If the Company had valuable proprietary technology or knowhow, it would not use a contract manufacturer for the production of its printers (ITS Industrial Techno Logic Solutions and IFAT). The print heads for Kornit’s system are supplied by FujiFilm Dimatix and the emulsion used in its ink is solely supplied by BG Bond (a subsidiary of Ashtrom). It appears that the only value KRNT adds are the “modifications” it does to the print heads after they are received. The IP for these print heads is owned by FujiFilm and are available to any competitor. The Company does not have any sustainable advantages. The industry’s low competitive entry barriers make KRNT’s market position tenuous. This is troubling, particularly for a company that is compared to R&D intensive, advanced tech names such as those in the 3D printer space. One need only look at the parallels to the desktop inkjet printer industry.

-

Sales Capabilities: Kornit heavily relies on its distributors as over 75% of sales come through this external network with Hirsch and SPSI accounting for 45% of KRNT’s sales. Meanwhile the two largest DTG distributors (Stahl and EquipmentZone) have chosen to partner with Epson.

Valuation

At $11.25 per share, KRNT has a $361M market capitalization. Sell-side expects revenue growth to accelerate to +30% in over the next two quarters and continue at that rate through 2017 yet even the most optimistic industry forecasts are calling for only 15% end-market CAGR through that period. Management guidance and Street estimates assume GMs will increase nearly 50% by 2017 and that adjusted EBITDA margins will nearly double from 9% to 16% 2017. These margin goals are unattainable, due to the lack of operating leverage embedded in the business (KRNT has actually experienced margin compression). This is likely only going to get worse given the large operating expenses the Company will need to assume to sell and support the Allegro.

Regardless, Kornit is a sub-scale “old-tech” inkjet printing business with limited moat, meager EBITDA generation and limited differentiated technology or patents yet KRNT’s current 3.9x revenue and 51x EBITDA multiples is two times that of 3D printers and even higher than that of most high recurring revenue SaaS businesses. Meanwhile, printer companies in Japan (Brother Industries and Seiko Epson) trade at less than 5-6x EV/ EBITDA. Brother and Seiko are much larger, established and generate higher ROIC than Kornit. At 6x EV/ EBITD, KRNT’s implied stock price would be 75% lower. The best comparable is EFII’s acquisition of Reggiani last year at 9-10x EBITDA. At 10x EV/ EBITD, KRNT’s implied stock price is $3.25 per share, 70% below current. It is worth restating that Kornit was acquired by Fortissimo Capital for just $16M in 2011 compared to its current $361M market cap.

Other Red Flags& Risks

-

Accelerating Cash Burn: Over the last four quarters KRNT’s FCF has become increasing negative. It does not appear its investment in market and sales is materializing and that it will be able to reach any sort of scale.

-

Lack of Operating Leverage & Deteriorating Working Capital: Despite having a high margin “recurring revenue” ink annuity stream, incremental EBITDA margins have been poor at KRNT implying no operating leverage. The Company’s working capital also suggests degradation, with inventory building at twice the rate of revenue and A/R growing at multiples faster than revenue.

-

Management Departure: Head of Marketing left in June. Also may be worth mentioning that $1.5M in market cap per employee is very high given the nature of the business.

-

Overhang: Fortissimo Capital (an Israeli private equity firm) owns 49% of the shares.

- The risk of an acquisition is very low given KRNT’s limited IP and precedent multiple of the EFII-Reggiani deal.

I and/or others I advise hold a material investment in the issuer's securities.

Catalyst

1) revenue shortfall in Q3 leading to guidance cuts from the current lofty expectations

2) increased competitive pressures leading to price cuts, margin decline and market share loss

3) failed entry into R2R and very limited adoption of Allegro printer

4) stock re-rating as its challenges are illuminated

5) potential share sales from Fortissimo Capital

| show sort by |