| 2013 | 2014 | ||||||

| Price: | 67.50 | EPS | $0.00 | $0.00 | |||

| Shares Out. (in M): | 106 | P/E | 0.0x | 0.0x | |||

| Market Cap (in $M): | 7,160 | P/FCF | 0.0x | 0.0x | |||

| Net Debt (in $M): | 1,200 | EBIT | 0 | 0 | |||

| TEV (in $M): | 8,360 | TEV/EBIT | 0.0x | 0.0x | |||

| Borrow Cost: | NA | ||||||

Sign up for free guest access to view investment idea with a 45 days delay.

- Goodwill Impairment

- Mining

- Manufacturer

- China

Description

Joy Global (JOY) is a manufacturer and servicer of high productivity mining equipment for the extraction of coal and other minerals and ores. One particularly relevant fact about Joy Global is that the Company reports a goodwill number of 1.38 billion USD as of Oct 26th, 2012 and I believe it may be facing a write-down of well over 1 billion USD if Caterpillar's Friday announcement were to be used as a barometer. Joy Global spent roughly 1.4 billion USD in 2011 and 2012 to acquire International Mining Machinery (IMM), a Hong Kong listed company, through its wholly owned subsidiary Joy Global Asia. It is worth noting that Caterpillar completed its acquisition of ERA Mining Machinery around the same time frame as Joy Global's International Mining Machinery acquisition. In this article, I will discuss the background of the story, Caterpillar's recent write-down announcement, the connections of the insiders and the likely implication for Joy Global.

Background and Impetus

Caterpillar (CAT) announced on Friday, January 18th in a press release that it is writing down 580 million dollar related to Siwei, the operating subsidiary of its recently acquired ERA Holdings. Dialing back the clock, on November 11th, 2011, Caterpillar announced its intention to purchase ERA Mining Machinery for as much as 887 million USD to broaden its exposure to modernization of Chinese coal mines, according to the Wall Street Journal and its separate press release. In a separate Wall Street Journal article discussing the most recent stumble by Caterpillar, the journalist cited about 700 million USD as the price paid. In other words, Caterpillar wrote off well over 80% of its purchase price on its embarrassing mining machinery acquisition in China. Indeed, investing in China is full of perils for the unsuspected, even for investors with both industry expertise and the ability to carry out a thorough due-diligence process.

In the SEC filing related to its write-down, Caterpillar stated the following:

"We believe our process is rigorous and robust and includes Caterpillar personnel and outside accounting, legal and financial advisors. It is important to understand that Siwei was a publicly traded company with audited financial statements. What we discovered at Siwei following the acquisition was deliberate, multi-year, coordinated accounting misconduct that was concealed by the persons responsible". (Text bolded by the author)

Commenting on the nature of the accounting misconduct, Caterpillar said:

"Caterpillar first became concerned about an issue when discrepancies were identified in November 2012 between the inventory recorded in Siwei's accounting records and the company's actual physical inventory. This was determined by a physical inventory count conducted at Siwei as part of Caterpillar's integration process. Caterpillar promptly launched a comprehensive review and investigation into the nature and source of this discrepancy. This extensive review has identified inappropriate accounting practices involving improper cost allocation that resulted in overstated profit. The review further identified improper revenue recognition practices involving early and, at times unsupported, revenue recognition. This review is ongoing".

For Caterpillar, however, a 580 million dollar write-down is completely manageable; with a market capitalization of roughly 63 billion USD, 580 million doesn't even amount to 1% of its market capitalization. A similar situation, however, paints a much bleaker picture for Joy Global's shareholders.

Who Are the Insiders?

To write down over 80% of its acquisition, one would have to argue that Caterpillar was seriously duped. The recent Wall Street Journal article by Mr. James Areddy did a fine job depicting connections behind ERA Mining Machinery; the connections, however, foretells a bigger story Mr. Areddy has yet to see.

In James Areddy's article discussing the unusual roots of Caterpillar's blunder, two individuals at the center of discussion are Mr. Rubo Li and Mr. Emory Williams.

"The company had been a relic of China's planned economy, but a U.S.-trained mining engineer and coal tycoon, Li Rubo, and Emory Williams, a Beijing-based American entrepreneur, transformed it over the past decade, seeking to tap growing demand for industrial equipment. They got it publicly listed as a non-Chinese company, with prominent international shareholders."

Mr. Li and Mr. Williams were entrepreneurs who started ahead in transforming Chinese SOE (State-owned Enterprises) into private companies and eventually bring them to listing on exchanges such as Hong Kong Stock Exchange. Mr. Williams has been the chairman of ERA Mining Machinery as well as one of the controlling shareholders of the Company through Mining Machinery. According to relevant disclosure and a Forbes article, Mining Machinery is 33% held by Mr. Williams and 67% held by James. E Thompson, which is identified as the son in law of Mr. Rubo Li by Wall Street Journal as well as Forbes. ERA's operating subsidiary Siwei was created during a wave of privatization of SOEs during the early 2000s. While Caterpillar's investigation is still on-going, the identification of the relevant roles and economic interests of both Mr. Rubo Li and Mr. Emory Williams exposed the vulnerabilities of Joy Global's acquisition of International Mining Machinery (01683) and very well should prompt a detailed internal review and audit of IMM by Joy Global, which may result in significant write-downs.

Where Are the Connections?

Before I proceed to discuss the parallels and connections between the ERA Mining Machinery acquisition by Caterpillar and the International Mining Machinery acquisition by Joy Global, I would like to highlight part of a very strongly worded statement by Caterpillar.

"What we discovered at Siwei following the acquisition was deliberate, multi-year, coordinated accounting misconduct that was concealed by the persons responsible".

"Multi-year" here is extremely significant and it goes a long way to explaining why I believe after carrying out internal audit and reviews, Joy Global will likely write down a significant percentage of its purchase in IMM and will be much more severely impacted due to the relative size of the acquisition and its own market capitalization.

While the Wall Street Journal article discussed in great details Mr. Li, who is also known as John Lee, and Mr. Williams' relationship and involvement in ERA Holdings, it failed to mention their ties to International Mining Machinery. As a matter of fact, Mr. Li and Mr. Williams are co-founders of International Mining Machinery and both own significant stakes in IMM according to public disclosures as well as other relevant information I obtained.

For starter, when International Mining Machinery went public on January 29th, 2010, in its global offering prospectus, Rubo Li was mentioned a whopping 122 times and Emory Williams was mentioned 101 times. Further, there had been extensive amount of related party transactions reported between the company and Mr. Li and Mr. Williams. The public disclosure at the time shows Rubo Li and Emory Williams together owned 9% of IMM, the remaining 91% was owned by the Resolute Fund, L.P., through TJCC Holdings. Emory Williams resigned as a director of the Company right before it went public likely because he is also the executive chairman of a primary competitor, ERA Holdings. Mr. Li, however, remained a director of the Company until early 2011.

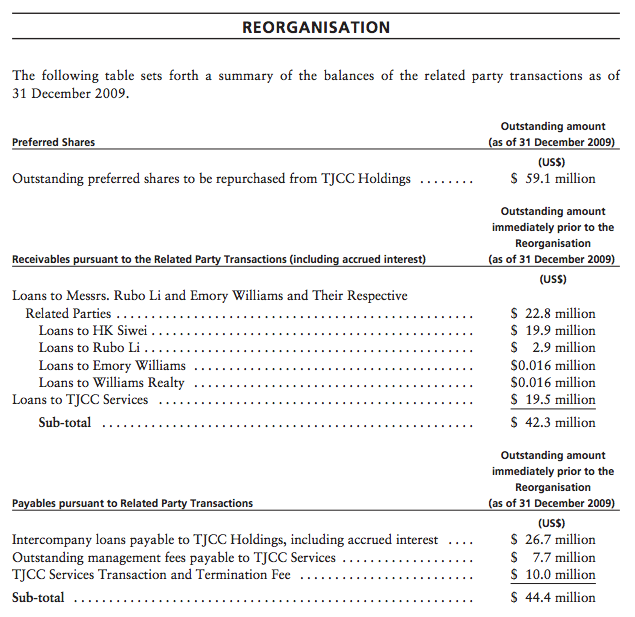

Further evidence pointing to an incredibly intertwined relationship between Rubo Li, Emory Williams and International Mining Machinery include the related party transactions reported in the prospectus. (A) Loans to HK Siwei (yes, this is the part of ERA that Caterpillar had to write off) ; (B) Loans to Rubo Li; (C) Loan to Mr. Emory Williams; (D) Loan to William Realty. TJCC apparently settled all the relevant related party transactions and forgave the loans at the time of IMM going public according to the Company's disclosure. In the prospectus, Rubo Li was identified to have acted as the Vice Chairman of the Company prior to it going public. I was also able to find a number of other articles that showed Mr. Li was clearly in an operating capacity at International Mining Machinery prior to its public offering.

Below is the page listing the relevant related party transactions involving Mr. Li and Mr. Williams at the time of the offering:

(click to enlarge)

Another important piece of information involves Mr. Li and Mr. Williams surfaced when the prospectus went on to discuss their roles in founding IMM.

"Mr. Rubo Li, our non-executive Director, and Mr. Emory Williams, our former Director who resigned as a Director in December 2009, had assisted The Resolute Fund, L.P. in identifying Jiamusi Machinery and Jixi Machinery as potential attractive acquisitions and subsequently participated in the acquisition negotiations. Mr. Rubo Li and Mr. Emory Williams were given minority interests in our Company as well as"founder participation" in the event of repurchase or redemption of our preferred shares as an incentive provided by The Resolute Fund, L.P."

Even though per public disclosure, Mr. Li and Mr. Williams stake in IMM was roughly 9%, my further research indicates the group likely controlled around 45% of IMM through their interest in TJCC Holdings or Resolute Fund.

The history of International Mining Machinery starts with combining two State-owned Enterprises, Jiamusi and Jiaxi Machinery back in late 2005 when China was going through a phase of privatization aimed at improving efficiency and balance sheets of such corporates. The creation of International Mining Machinery was in fact a case study when it comes to discussion on the topic of how foreign capital invaded traditional industries in China. The article I linked provids a great background story on the creation of IMM. According to the above-referenced article, the total purchase price of the two companies combined amounts to roughly 300 million RMB or slightly less than 40 million USD at the exchange rate in 2005. This discussion further highlighted breakdown in terms of ownership interest: International Mining Machinery, at the time, was 60% owned by interests controlled by Jordan L.P., 15% owned by Emory Williams and 25% owned by entity controlled by Rubo Li. While China had gone through an incredible period of expansion, and the value of acquired subsidiaries of IMM probably increased in value, at Joy Global's purchase price of 1.4 billion USD, that would have represented an appreciation of well over 35x over the course of 5-6 years; To put that number into perspectives, the most parabolic growth company of the last decade, Apple, increase in value by around 10x during the same period of time.

Conclusion

Based on the evidence I presented, I believe a detailed internal review and audit of International Mining Machinery is warranted by Joy Global in light of the recent scandal reported by Caterpillar. While it is difficult to predict the outcome of such investigation and what level of write-down Joy may ultimately take, it is most likely going to be very significant given the size of its IMM acquisition, the percentage reported in Caterpillar's write-down and the important connections shown between IMM and ERA. A write-down north of a billion USD is very well within the realm of possibilities and could happen in the very near term.

I and/or others I advise hold a material investment in the issuer's securities.

Catalyst

| show sort by |