| 2020 | 2021 | ||||||

| Price: | 1.43 | EPS | 0 | 0 | |||

| Shares Out. (in M): | 56 | P/E | 0 | 0 | |||

| Market Cap (in $M): | 80 | P/FCF | 0 | 0 | |||

| Net Debt (in $M): | 0 | EBIT | 0 | 0 | |||

| TEV (in $M): | 0 | TEV/EBIT | 0 | 0 | |||

Sign up for free guest access to view investment idea with a 45 days delay.

Description

Investment Summary

Hill International (HIL) is a relatively illiquid microcap whose market capitalization has fallen 50% since the end of FY 2019. Although there have been several setbacks, the new management team has met its important cost reduction targets, and insiders have been buying. Furthermore, despite the COVID pandemic, 95% of the Company’s employees remain at work, and the business continues to generate revenue and win new projects. HIL is an attractive takeover target and is currently trading at a valuation covered by a conservative valuation of just one of its geographic segments -- the US business.

The Business

HIL is a professional services firm that provides fee-based construction management services. With most of HIL’s contracts structured as time and materials or cost-plus, HIL avoids taking on construction and completion risk. Moreover, HIL’s earnings power should benefit from recent cuts in its Selling, General, & Administrative (SG&A) cost base. Management argues that they can hold SG&A steady as the top-line grows. HIL plans to grow the top-line (undistracted by restatements and boardroom drama) by seizing opportunities as infrastructure spending increases post-COVID.

HIL’s Hilly History

HIL has been written up on VIC several times over the past five years, most recently by both aa123 and gi03. I encourage the reader to review both of these write-ups as they present a compelling argument for why HIL was, at that time, an attractive turnaround about to reach a corporate governance and profitability inflection point.

Since the most recent write-up in 2017, HIL’s shares have traded as high as $6.11 and as low as $1.08. Despite the attractive set up in 2017, HIL’s shares have declined by ~67%, closing most recently at $1.43. From our perspective, the macro trend in HIL’s share price is, at least in part, due to investor exhaustion from the events of the recent past and a temporary, COVID-related, poor cash flow Q1 in 2020.

In 2015, HIL received two premium takeover bids ($5.50/share and $4.75/share) that each valued the business at roughly 10x TTM EBITDA. HIL summarily rejected both of the offers without negotiation. At the time of the offers, HIL’s founder, Irvin Richter, and his son, David Richter, were at the helm.

Activist investment firm Bulldog Investors embarked on two separate proxy battles with the Company, which ultimately led to the restructuring of the Board (independence) and the resignation of CEO David Richter. To address the concerns of the activists, in 2017, HIL announced that it would embark on a Profit Improvement Plan (PIP), which vowed to cut SG&A by 25% to a run rate of $120M and to refocus the business on profitable growth. Revenue growth would fall straight to the bottom line, and management guided that a 10% EBITDA margin (on Consulting Fee Revenue) was ultimately achievable. Also, the Company divested one of its units (the Construction Claims Group (CCG)) and used the proceeds to de-lever and, as a result, became a pure-play professional services firm. A refocused operation was ostensibly more attractive to potential acquirers.

Unfortunately, just as HIL seemed to be turning a corner with respect to governance, the sale of the CCG unearthed accounting issues related to foreign exchange transactions that delayed HIL’s 2016 results, led to the complete restatement of FY 2014, FY 2015, and FY 2016 financials, and delayed 2017’s reporting. The restatements resulted in a “collective reduction to Hill’s net earnings of more than $30 million” for the periods 2014 through Q1 2017 [see SEC complaint below]. The restatement included $5 million of foreign exchange losses on intercompany loans that HIL had incorrectly recorded. According to the SEC complaint, although Chief Accounting Officer Ronald Emma and his employee Nicholas Tornello discovered the errors in 2014, rather than make the requisite adjustment, the two decided to fraudulently “bleed” the losses out over time. To make matters worse, HIL raised $40M in equity from investors who relied on the misrepresented financial statements. [SEC complaint]

As a result, understandably, the share price declined. Ultimately, the Company incurred ~$20M in extraordinary audit-related expenses and paid $500K to settle with the SEC.

To add insult to injury, HIL was delisted from the NYSE and began trading OTC Pink. On the day HIL began trading OTC (August 14, 2018), volume spiked to over 11M shares, and the price fell 30%, a pretty clear indicator of forced or indiscriminate selling by institutional investors (or others).

HIL was subsequently relisted on the NYSE just a few months later on October 18, 2018. However, in 2019, due to its decreased market capitalization, HIL was deleted from the Russell 2000 Index and was added to the less-followed Russell Microcap Index (where it remains today).

At the end of 2018, it appeared that HIL was going to emerge from its restructuring and begin to see its growing backlog flow through the P&L. CEO Raouf Ghali stated that HIL’s clients now understood that HIL was “once again focused on their needs,” rather than its internal issues.

HIL had a solid, though not spectacular 2019 finishing the year with Consulting Fee Revenue (CFR) of $309M, SG&A expense of $111M, EBIT of $18.3M, and adjusted EBITDA of $16.9M (5.5% EBITDA margin on CFR). The results (except the adjusted EBITDA number) include a ~$7M net recovery on an outstanding doubtful account from Libya (See “7. Optionality” below). After years of distractions and uncertainty, the 2019 results were undoubtedly positive. Looking forward to 2020, HIL guided to $330 - $350M in CFR, representing top-line growth of 6.8% - 13.3% over 2019. They also guided EBITDA margins of 5.5% - 7%. Therefore, 2020 EBITDA expectations were in the range of $18M and $24.5M. 2020 looked like it would be a breakout year for the Company.

Then, in 2020, the coronavirus pandemic hit, resulting in project deferrals and cancelations. In addition, low collections related to the global shutdown resulted in significant negative free cash flow in Q1 2020. The Q1 result was perhaps the last straw for some investors as HIL shares broke out of lockstep with the overall market and have remained at depressed levels ever since. HIL announced Q1 results on 5/7/2020.

Why HIL Is A Buy Today

1. Valuation

HIL is commendable for its detailed disclosure of segmented results for each of its geographical segments. However, below the gross profit line, regional comparison becomes a challenge. Reported operating performance numbers included unrealized foreign exchange effects and expenses allocated via transfer pricing for tax purposes. To make matters more complicated, in 2019, HIL reclassified certain “back-office expenses and foreign currency translation gains” from individual regions in the operating profit/(loss) table to the corporate costs line item. The reclassification rendered past geographic results difficult to compare with current results, but it might make future results more comparable.

Despite the reclassification, gross profit values across regions remained relatively unaffected. Given that HIL targets a $120M aggregate cost base, we use the regional gross profit values to compare region profitability and an aggregate $120M cost base deduction from consolidated gross profit in our estimation of operating income for the overall entity.

The gross profit numbers below show that each geography is profitable and covers its variable direct expenses. Regions such as the United States and the Middle East are significantly larger than other segments yet boast similar gross margins. Thus, it is reasonable to assume an opportunity exists for HIL to scale the undersized regions and add meaningfully to the consolidated entity’s profitability while effectively holding SG&A fixed at $120M.

Note that we compute the above gross margins as Gross Profit/Total Revenues. The Total Revenues line item includes both (i) Consulting Fee Revenues (CFR) and (ii) subcontracted items and reimbursable expenses, which effectively have a 0% gross margin. Therefore, the calculated margins are lower than if calculated based solely on CFR. For reference, TTM gross margins on CFR are as follows:

HIL’s management team has put forth the following revised guidance for FY 2020:

[Source: Investor Presentation, August 2020]

Again, management computes the gross margin using CFR as the denominator, not Total Revenue. It is also important to note that the $110M SG&A guidance includes an additional $10M stripped out during COVID and that the run rate estimate remains $120M.

We have applied some conservative assumptions to illustrate our view of the upside opportunity present in HIL today. In estimating 2021 CFR, we use the low end of 2020’s initial CFR guidance. We believe this is reasonable because customers have pushed some of the projects that HIL initially expected to burn in 2020 into 2021. Also, governments have an opportunity to use infrastructure spending to boost their post-pandemic economies, and demand for HIL’s services can increase as budgets become constrained, and efficiencies become paramount (See “8. Appendix: Infrastructure”).

We assume a starting EBITDA margin on CFR of 5%, roughly in line with performance today and just under the low end of 2020’s initial guidance. We assume a linear increase from 5% in 2021 to 9% in 2025. 9% represents a 10% discount management’s long-run target of 10%. We allow the EBITDA margin to grow to 9 percent via the CFR growth input. Therefore, we assume that SG&A remains fixed at $120M and that CFR growth, via operating leverage, increases EBITDA and the EBITDA margin. Given HIL’s $120M cost base, EBITDA margin growth to 9% requires a CFR CAGR of just 2.18%. This scenario is roughly a “business as usual” scenario where CFR grows in line with long-run GDP and inflation targets. We assume an 8x EBITDA exit multiple at the end of 2025, which implies a 13% discount rate and a conservative 0.5% terminal growth rate for HIL in perpetuity.

These conservative assumptions and the resulting model provide a rough estimate of HIL shares’ upside opportunity.

Now let’s take a look at HIL’s attractiveness as an acquisition target.

2. HIL Is An Attractive Acquisition Target

DC Capital’s Offers to Buy HIL

DC Capital 1st Offer - 5/7/2015 - $5.50/share

In May 2015, DC Capital Partners, the owner of Michael Baker International, LLC, offered to purchase HIL’s outstanding shares for a cash price not less than $5.50 per share. At that time, the offer represented a 40.7% premium to the share price. Furthermore, DC Capital worded the proposal to indicate that the final price could be above $5.50 per share. However, HIL rejected the offer without further negotiation. The offer was, excluding synergies, roughly at an implied EV/EBITDA multiple of 10x.

[Source: link, HIL filings, author calculations]

DC Capital 2nd Offer - 12/16/2015 - $4.75/share

Later in 2015, DC Capital again made an offer to buy HIL at $4.75/share, citing management failure to achieve stated goals and increased leverage as the cause of the lower bid for the equity:

[Source: link, HIL filings, author calculations]

HIL Sale of Construction Claims Group in 2017

In 2016, HIL sold off its Construction Claims (“CCG”) business to Bridgepoint Development Capital (closed in 2017). The negotiated price was $147M (later renegotiated down to $140M). At that time, CCG generated $163.1M in revenues (making up ~26% of Hill’s CFR) and generated a TTM Operating Profit of $11.1M. The renegotiated price reflected roughly 10x EBITDA.

When DC Capital made its offer, HIL’s Construction Claims business had generated ~$15M in TTM EBITDA. Thus, the ultimate sale price of the CCG was roughly at 9.3x TTM EBITDA on 9/30/2015. By stripping out the EV of the CCG from the subsequent sale, we can estimate what DC Capital would have been paying in terms of EV for the continuing operation (HIL today):

HIL today trades at a ~50% discount to the implied EV offered by DC Capital for HIL ex-CCG despite improvements in governance, controls, leverage, and a reduced cost base. Two comparable transactions indicate a 10x EBITDA multiple is reasonable.

SNC-Lavalin Acquisition of WS Atkins in 2017

The acquisition represented an enterprise value of $4.2B and an estimated 9.8x EBITDA multiple (post synergies).

[Source: link]

AECOM Sale of Management Services Business in 2019

AECOM, a significantly larger direct competitor, announced its Management Services business’s sale for $2.405 billion in 2019 (an 11.6x multiple of EBITDA). The 11.6x multiple was at a premium to AECOM’s consolidated multiple at that time.

[Source: link]

3. Downside Protection: Value of the US Segment Exceeds Market Capitalization

Below are the TTM operating profits by geographical segment. Note how profitable the US segment is. Valuing the US segment alone and applying a conservative multiple illustrates that the US business essentially makes up today’s entire market capitalization. Furthermore, HIL’s recent shutdown of its Brazilian operations should improve operating income in Latin America.

[Source: Company filings]

As stated earlier, HIL moved some expenses from individual regions into the corporate line item. The only period for which we have both sets of numbers is FY 2018:

[Source: company filings]

It is most likely that the delta in the US EBIT after re-classification is related to back-office expenses as it seems unlikely that there would be much foreign exchange expense for the domestic business.

Given how small HIL is relative to, say, AECOM, in an acquisition, a large firm with substantial corporate operations could likely absorb HIL’s EBIT while eliminating much of HIL’s SG&A.

Since we cannot know how an acquirer would handle the back-office expenses, to be conservative, we will adjust downward HIL’s TTM EBIT by ~34% (the reclassification delta evident in 2018 numbers) to develop a worst-case valuation for HIL’s US segment.

[Source: filings & author calculations]

In either case, HIL is cheap today, and the value of the US operations more than covers today’s market capitalization.

4. New Management Team: Aligned Executive Compensation, Reduction of SG&A Cost Base & Shuttering Unprofitable Geography

New Management Team

CEO Raouf Ghali

Raouf Ghali ultimately replaced David Richter as CEO. Mr. Ghali has been with HIL since 1993, having most recently served as the President of Hill’s Project Management Group and as President and COO. HIL went public via a SPAC in 2006, and between 2007 and 2015, while Mr. Ghali was President of Hill’s Project Management Group and HIL was a public company, project management revenues grew by a CAGR of 17% from $135M in 2007 to $468M in 2015.

CFO Todd Weintraub

HIL hired Todd Weintraub at the end of 2018 to steer HIL following the costly and distracting restatement process. The previous CFO, who was apparently out of the loop on the fraudulent activities, retired following the accounting debacle that saw HIL, the Chief Accounting Officer, and a Senior Accountant charged by the SEC.

Executive Compensation Now Aligned with Shareholders

Before the restructuring at HIL, executive compensation was spectacular in its magnitude. In the five years from 2012 to 2017, CEO David Richter took home (including severance) ~$17M in total compensation. He also had two company cars. During that same five-year period, HIL “generated” a net loss of ~115M and, on the day of Richter’s resignation, closed with a market capitalization of $233M. Not to mention, problematic accounting over those periods led to the restatements and the $20M associated expenses.

[Source: Company filings]

As an aside, Richter is currently running for Congress in New Jersey where, perhaps ironically, he vows to “use his private-sector experience to streamline the federal bureaucracy and promote spending reforms that rein in the size and cost of government to balance the federal budget” [link]. Furthermore, he remains a large shareholder in HIL and relies on the market price for personal gain (and maybe campaign funding) like the rest of us:

“You are asking the person who is most concerned about Hill’s stock prices, I wouldn’t even say on a daily basis. I probably look at the stock every hour,” he said. “I’m one of the company’s largest shareholders. I’m very surprised by the current stock price, but it does not impact my ability to satisfy the commitment that I made to the party.”

David Richter, 3/12/20

Source: [link]

HIL’s independent board designed today’s executive compensation plan to align management with shareholders. CEO Raouf Ghali’s base salary was $650,000 in 2019. Mr. Ghali’s 2019 salary represents a 36% decrease from his 2018 base salary and a 60% decrease from David Richter’s peak base salary. Furthermore, in 2019, the board adopted Annual Incentive Awards for the three executive officers tied to:

Significant Reduction In SG&A Cost Base

As touched on earlier, the Profit Improvement Plan set forth by the management team vowed to reduce the Company’s cost structure by $27M to $38M per annum (pretax) by June 2018 and they have done just that:

“We continue to believe SG&A of around $120 million is sustainable for 2020, and the increases in CFR and gross profit will mostly fall right through to the bottom line, increasing our EBITDA margin overtime to approximately 10%.”

Todd Weintraub, HIL CFO

Q1 2019, Q2 2019, Q3 2019, & Q4 2019 Earnings Calls

HIL’s business is inherently lumpy at the top line. The rationalized cost structure provides HIL with more flexibility to withstand revenue gyrations while also increasing the probability that the company benefits from another management promise -- operating leverage.

Furthermore, given the uncertain business climate resulting from COVID-19, HIL was able to temporarily strip an additional $10M from the operating expense budget in 2020.

The Shutdown of Unprofitable Operation in Brazil

In Q2 2020, Hill decided to shut down its money-losing operations in Brazil. The deconsolidation of Hill Brazil resulted in a charge against earnings of $4M in the quarter.

HIL’s US business is very profitable relative to the other geographies in which the Company operates. The shut down of Hill Brazil will likely improve the consolidated operating income picture. A larger competitor with adequate corporate operations could easily bolt HIL on while realizing significant synergies at the corporate level.

5. Insider Buying

In addition to improved governance and incentives, HIL insiders have added to their positions since the COVID related decline in March:

[Source: Sentieo]

CFO Todd Weintraub increased his position by ~47% in May 2020, buying 36,100 on the open market at a weighted average price of $1.36 (~5% below today’s price).

Ancora Advisors, LLC, whose various funds own ~2.14M shares (~3.8% of the company), added 75K shares to its position in May 2020, at a weighted average cost of $1.47. Since 12/2018, Ancora has added ~1.10M shares at a weighted average price of $2.46. Director James Chadwick is a Managing Director at Ancora.

Jamarant Capital, LP, added 88,780 shares in 2020, increasing its position by ~32% at a weighted average purchase price of $1.47. Chairman David Sgro is a Managing Member of Jamarant.

6. Q1 2020: FCF, COVID, & Retraction of Guidance

While the COVID-related threat to the construction and project management industry is likely temporary, the risk of a short term liquidity crunch is a legitimate concern.

On the day of HIL’s Q1 2020 earnings call, shares opened at $2.10/share and closed at $1.64/share. The ~22% decline in share price appears to have been a reaction to HIL’s poor cash quarter and the uncertainty caused by the pandemic, and HIL’s 2020 guidance retraction. In Q1 2020, HIL burned $12M of free cash against a starting quarter cash balance of $15M, which led to an $18M draw on its revolver and quarter-end borrowing capacity of just $2.8M.

Since Q1, cash flow has been positive, with roughly $6M of FCF in Q2.

[Source: Investor Presentation, August 2020]

The CFO believes that the company will generate cash through the end of the year, improving the liquidity position. It is our belief that the cash crunch of Q1 2020 was a one-off event, and HIL’s long-term viability is not in question despite the current market valuation.

Q1 2020 Notable CFO Quotes

“...we have not seen a significant impact to date on our CFR from the pandemic, and we currently believe the CFR we generate from existing projects will mostly continue. However, our CFR in any given year is a combination of CFR from ongoing projects and CFR from new projects. As mentioned earlier, our new bookings are down as many projects scheduled to be awarded this year have been deferred. We are therefore retracting our prior CFR guidance of $330 million to $350 million for 2020. We are not giving any revised guidance on 2020 CFR at this time due to the uncertainty regarding the future economic impact of the pandemic. We intend to provide revised guidance when we have a higher level of confidence of the impact of the pandemic on CFR.”

“We had negative free cash flow of $11.8 million for the quarter. The first quarter is historically slow for collections as some public sector clients await funding from new budgets to become available. The cash flow deteriorated more this year as we saw a significant slowdown in collections in the latter part of March. We believe this was due to an initial disruption in processing at some of our clients as back office locations shut down from coronavirus and went remote. Collections have returned to more normal levels in April.

Todd Weintraub, HIL CFO

Q1 2020 Earnings Call

(our emphasis)

7. Optionality

Emerging Facilities Management Business

Hill's emerging facility management business provides us with the opportunity to extend our client relationships beyond the completion of a project and create a recurring revenue stream [...] We are currently providing facility management services in 3 countries with blue chip clients, including the Abu Dhabi National Oil Company, ADNOC, for its entire portfolio of ADNOC facilities.”

CEO, Raouf Ghali Q2 Earnings call

HIL’s started its facilities management business in 2016. However, in 2020, HIL has increased its emphasis on this business line. The opportunity can generate recurring revenues and increase the duration of the relationship between HIL and the client with an average contract duration of 3 years. The Facilities Management business is potentially cross saleable in all of HIL’s current markets.

Libyan Receivable

The Libyan Organization for the Development of Administrative Centers owed HIL $60M for work the Company had completed. Improper accounting for the receivable led to restatements and a Class Action lawsuit. The SEC found that Hill should have accrued a loss for the receivable. Following the SEC letter, Hill reserved the entire receivable, net of subcontracting expenses, of $48.1M.

HIL has begun to receive payments, but the timing of future payments is uncertain. The amount outstanding and recorded under doubtful accounts stands at ~$32M or roughly 40% of today’s market capitalization, offering a free option. For valuation purposes, we estimate the value of this receivable to be zero, but the management team continues to reiterate that they believe Libya will ultimately pay in full.

Conclusion

HIL is hated by investors due to its troubled past. The company operates an attractive construction management-for-fee business with low construction completion risk. COVID has shaken the construction industry, but we believe that demand for HIL’s services will increase as companies and countries streamline their projects and squeeze efficiencies out of constrained budgets post-COVID. Furthermore, HIL stands to benefit from increases in infrastructure work and will benefit from its long history and lasting relationships with various governments. Even a conservative multiple on just HIL’s US operations covers today’s market capitalization, and despite the pandemic, HIL continues to complete work and book new projects.

Risks

8. Appendix: Infrastructure Needs

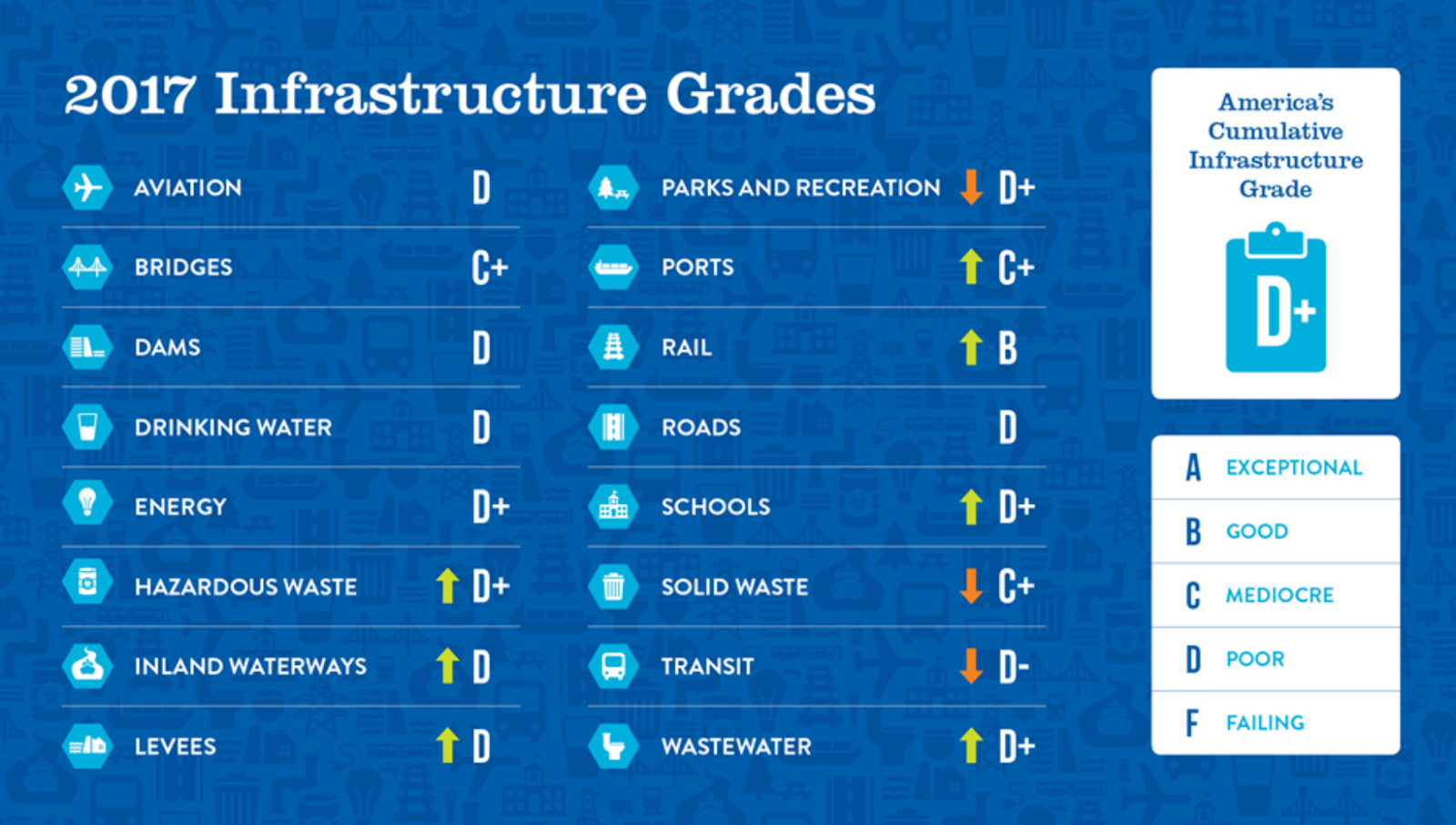

Infrastructure Spending

Every four years, the American Society of Civil Engineers assesses the state of US infrastructure. The most recent report from 2017 illustrates the dire need for increased investment:

Source: ASCE's 2017 Infrastructure Report Card [link]

A comparison with grades from the 1988 report illustrates several critical areas that have deteriorated, notably Aviation, Roads/Highways, Drinking Water, and Transit. [link]

In a 2014 report to the National Association of Manufacturers, Werling and Horst of the University of Maryland concluded that due to “cumulative effects through time, by 2030 infrastructure investments would produce economy-wide returns of close to $3 for every $1 invested.” [link]

US Infrastructure Needs

The United States’ infrastructure quality currently lags behind many of its competitors:

Source: World Economic Forum, “The Global Competitiveness Report 2019” [link]

Global Infrastructure Needs

Source: World Economic Forum, “The Global Competitiveness Report 2019” [link]

Construction Generally

[Source: link]

According to Associated Builders and Contractors, “CBI quantifies the previous month’s work under contract based on the latest financials available, while CCI measures contractors’ outlook for the next six months.” As we might expect, both the level of completed work and the overall confidence level of the construction industry is down significantly from where it was at the end of FY 2019. The obvious conclusion seems to be that the pandemic will ultimately be a net negative to HIL. However, it is our view that the COVID-related downturn in the construction industry is temporary. While the epidemic is likely to shift the mix of project types, it is unlikely to lead to a permanent decrease in demand for construction in the long run. It is probable that Investment in projects linked to hospitality, entertainment, and retail decline while projects in transportation and healthcare will increase. Governments, looking to stimulate their economies, are expected to spend on infrastructure projects. Furthermore, the possible increase in project delays should emphasize the need to operate efficiently, leading to a rise in demand for companies in the project management and construction consulting industry. The battlefield ahead for the sector will undoubtedly be filled with many new and unfamiliar obstacles.

“The coronavirus has cast a spotlight on the importance of worker health and safety, and companies are responding by implementing new job site policies, such as staggered shifts, employee temperature checks, and top-to-bottom disinfections of job sites, tools, and machinery. Virtual meetings will likely be a new normal, as E&C firms are developing new tools to streamline large client meetings, a crucial component in the process of creating commercial projects.”

Deloitte “Midyear 2020 engineering and construction industry outlook.”

[Source: link]

HIL is well-positioned to take advantage of the increased need for efficiency and, given its long-standing relationships with government entities, is similarly well-positioned to aid in economy stimulating infrastructure projects.

I and/or others I advise hold a material investment in the issuer's securities.

Catalyst

Revenue growth, especially in undersized regions.

Positive cash flow through 2020, which improves liquidity position.

Financial reporting without miscellaneous non-recurring charges.

Libyan receivable collection.

| show sort by |