| 2017 | 2018 | ||||||

| Price: | 35.80 | EPS | 0 | 0 | |||

| Shares Out. (in M): | 64 | P/E | 0 | 0 | |||

| Market Cap (in $M): | 2,292 | P/FCF | 0 | 0 | |||

| Net Debt (in $M): | -93 | EBIT | 0 | 0 | |||

| TEV (in $M): | 0 | TEV/EBIT | 0 | 0 | |||

Sign up for free guest access to view investment idea with a 45 days delay.

- Adtalem Global Education, Inc. ATGE 09/04/2020

- Adtalem Global Education Inc. ATGE 06/28/2017

- BETA

- DOUBLEVERIFY HOLD INC-REDH DV 05/28/2021

- DEVRY EDUCATION GROUP INC DV 01/20/2015

- DeVry DV S 07/06/2004

- DEVRY EDUCATION GROUP INC (DV) DV 12/23/2015

- Digital Value SpA BIT:DGV 02/26/2020

- VALEANT PHARMACEUTICALS INTL VRX. 05/12/2017

Description

Why Does this Opportunity Exist?: For profit education stocks have rallied hard since the election. I believe some investors have stopped looking in this field because they think the move is over. Also, since many sell-side shops have dropped coverage of the for-profit education section, many are not aware of the changes that have taken place both at the company and within the industry.

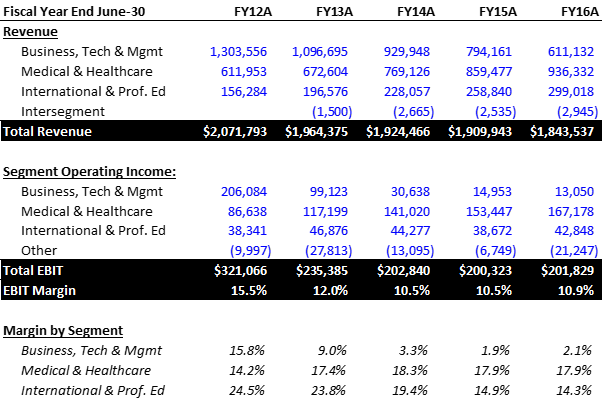

Business Description: Much has already been said about DeVry in past postings, so here I am going to list all of the other parts of the business and how they related to the current reporting. DV has 3 main segments: 1) Medical and Healthcare – Includes AUC (American University of the Caribbean School of Medicine), RUSM and RUSVM (Ross University School of Medicine and the School of Veterinary Medicine), Chamberlain College of Nursing and Carrington; 2) International and Professional Education – Includes DeVry Brasil and Becker, and 3) Business, Technology and Management includes DeVry University (what people typically think of when they hear "DeVry").

Levers for Operating Improvements:

Company at an inflection point: Expect to show further momentum in earnings growth. DV has had a solid string of consecutive quarters of improvement in Operating Income. They are growing enrollments in medical and nursing side; many believe there is some secular growth here addressing the nursing shortage we have in the U.S. (this will be a problem regardless of what happens to the ACA)

Too much focus on DeVry the college, and not on the other parts: Focus on DeVry University’s declining enrollments has blurred the strong operating performance at the brand’s other colleges. Strong profitability increases are occurring at these other brands as well. Today, virtually all earnings growth is coming from growing colleges serving Medical, International, and Professional Education. I would argue that their past performance has been masked by issues faced at DeVry University, but this should not persist. DeVry is a fundamentally different business from what investor might remember, and not necessarily the shrinking ice cube that it used to be.

Over the past 5 years DV’s business portfolio has undergone a large shift away from DeVry University. Most notably, DeVry went from 63% to 33% of revenues, while the Healthcare, International and Prof. Education (everything else), went from 37% to 67%. When it comes to EBIT, the change has been even more dramatic. DeVry’s contribution to EBIT has gone from 64% all the way down to only 6%. Operating margins on Medical & Health / International are much higher than the corporate average, implying that going forward the portfolio will experience earnings upside from faster growing and higher margin businesses than before. I would argue that the market has not fully appreciated this change in portfolio mix because it does not screen well, DV still has the legacy "DeVry" name, and it takes work to build the pro-forma financials based on the many restructuring charges and recent acquisitions.

Still more room for them to reduce overhead: Moving forward they will be duplicating the kinds of cost reduction strategies that have worked well at DeVry University across their other institutions. Thus far mgmt. has proven to be very adept at cutting costs.

Equity de-risked with regulatory headwinds behind them from the FTC and the DoE litigation: In October 2016, they reached an agreement with the DoE. On Dec 15-16, DV announced it would settle litigation with the FTC regarding the use of employment statistics in advertising. These cases consumed a significant amount of management’s time in 2016. With these in the rear-view mirror they can now focus more on going on offense and growing the business.

Announced new $300M share repurchase program: This authorization is through 2020, replacing its $100M share repurchase authorization that was announced on December 15, 2015. What I believe is even more interesting, was the choice to simultaneously cancel its bi-annual cash dividend. This is a sign that they believe buying back shares is a better way to return capital to shareholders than its dividend, further suggesting that A) mgmt. believes DV is to be undervalued and B) they are comfortable taking on more leverage.

Company has signaled they intend to take on long-term debt: See the recent conference call commentary from February 3rd:

Ques: “Given that you have debt now, would you be willing to stay levered if that meant the opportunity to buyback more stock?”

DV: “The answer is, yes. We would be willing to look at that and, obviously make sure that we are doing that in a prudent fashion that our board approves of but, yes, we would.”

DV (Later in the Call): “We are in a new day here. We have that behind us, and we recognize as a management team and as a board, which is obviously integral to these questions that we are trading below our – we are undervalued. We are trading below our intrinsic value and we know that and we recognize that…”

The business has had to stay under-levered up until know for two main reasons. 1) Due to regulatory issues/settlements, there were restrictions as to how much capital could be returned to shareholders. This is in their rear-view mirror. And 2) enrollments were previously falling hard, but the declines in the industry are beginning to stabilize. So with some positive momentum I expect DV to return more capital to shareholders as the other higher-margin, non-DeVry segments power the company forward.

Valuation: As mentioned above, today the company is optically cheap, trading at approx. 12.0x-12.5x forward EPS, and 6.75x-7.0x forward EBITDA. To put in context the other comps are trading at about 8x-8.5x forward EBITDA and 16x -20x forward EPS. (Note: Forward EPS may appear rich for some names because of expectations of the industry finally returning to earnings growth). For the sake of this write-up I don’t like the SOTP valuation because I do not anticipate DV breaking itself up and selling for parts. (They seem happy with the assets they have today). And EV/EBITDA might not be best because DV is overcapitalized and I expect it to take on more leverage in the future. With conservative assumptions I can see DV doing EPS between $2.90 -$3.25, implying a current valuation of 11x-12.3x. Using a 15x forward multiple that gets to $44 - $49 per share, for a potential upside of 22% - 36%. To illustrate the potential upside from buybacks and increased leverage, the current buyback authorization is for $300M, or 13% of the market cap. That is also about equal to 1x of EBITDA. So for illustrative purposes, if DV took on an additional 1x of debt, and spent $300M to buy back 8.3M shares at $36 (let’s assume the stock goes nowhere), that would juice EPS to $3.30 – $3.75, which at 15x would get you a stock range of $50 -$56, for a potential upside of 38% - 57%.

Downside Risks: Of course given the operating leverage in an education business model, one needs to monitor enrollment trends. Should they accelerate to the downside, I would change my mind. However, there have been signs of stabilization after years of declines, the worst actors have been forced out of the market, and DV has focused their growth on vericals focused on medical/nursing and foreign markets. Based on the commentary from this mgmt. team, if things went bad, I would not be surprised if they sold the company for its parts. (Highly unlikely) However, the increased leverage and higher share-buybacks should provide some downside protection as they get a handle on earnings. The new $300M authorization is equal to 13% of today’s market cap. I think that gives you some downside protection while we wait for the business to improve.

I and/or others I advise hold a material investment in the issuer's securities.

Catalyst

Share buybacks, operating improvements.

| show sort by |