Please also see JohnKimble's write up from last July...The good news, the stock is approximately 15% cheaper.

We think the market is wrong about DowDuPont’s current valuation, and we expect this disconnect to resolve itself over the next nine to twelve months. Wall Street currently has several concerns with DowDuPont. First, investors are skeptical that DowDuPont will achieve its target of $3.3 billion of annual cost reductions and $1 billion of added revenues. To date, the company is ahead of schedule and increased the total number from $4 billion to $4.3 billion. Second concern is that even if DowDuPont achieves these synergies, Wall Street believe that the company’s operating margins will still suffer. The third concern is that no two companies of this size and scale have ever successfully merged and then split into three separate companies that are more competitive than their predecessors. A lot can go wrong. At the current price, Wall Street is too pessimistic about the execution risk.

DowDuPont is a collection of several unrelated businesses. Typically, a combined company of this size trades at a conglomerate discount. Once management breaks apart the conglomerate and each individual business reports more details on its own operations, the discount should disappear. This basic principal is what creates investment opportunities with spinoffs. Transparency and management’s flexibility regarding capital allocation and business strategy create a better environment to grow a business than when the business resides within a large, diverse corporate entity.

The chemical business is a highly cyclical and commodity-based industry. Current market conditions are typical at economic cycle peaks. Not surprisingly, investors are now cautious about cyclical investments. Finally, China trade war headlines fuel the media narrative. Management believes the risk of such an event is low. Investors should focus more on actions and outcomes than headlines. The uncertainty surrounding the merger integration and the spinoffs is rational, but we believe that DowDuPont will climb this wall of worry over the next year.

Company management publicly stated that the difference between stock market pessimism and the positive trends in the company’s business have created a material disconnect between the business’ fundamentals and Wall Street’s view of the business. Management remains worried about running a business and not consensus earnings estimates published by Wall Street. Management believes that DowDuPont is a contrarian value setup with the market too pessimistic about the business in both the near and long term. Most market participants are concerned with one risk above all other risks–market risk, the likelihood of the share price falling. If the market continues to be weak, most investors will assume DowDuPont will be even weaker. A value investor should always focus more on business results and spend less time predicting stock price movements. The company’s business results do not depend on the stock price but on management’s execution of the merger integration and preparation for the spinoffs. The true source of risk is in execution risk – that management might not be able to do what it publicly states.

DowDuPont is a massive collection of several market-leading businesses. Management intends to execute specific plans designed to increase shareholder value, beyond simply continuing to operate the individual businesses. We think breaking up DowDuPont will generate attractive returns over the next decade. This is a great bet for value investors with long-term viewpoints. We conservatively estimate fair value at $75 per share.

Business Description

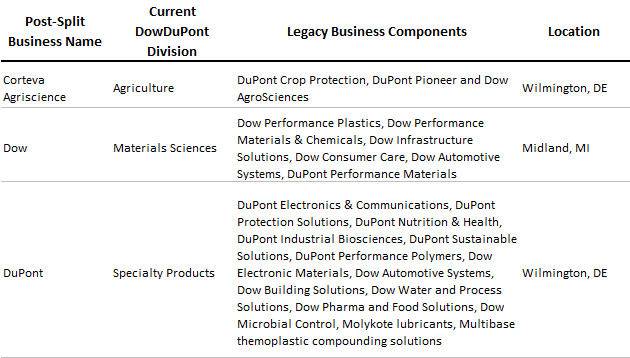

DowDuPont is one of the dominant players in the global chemical industry. The company has annual sales of more than $80 billion and over 100,000 employees across more than 130 countries. DowDuPont is a holding company established for the sole purpose of splitting into three separate businesses, based on its current Agriculture, Materials Science, and Specialty Products divisions. After the spinoffs, the Agriculture division will become Corteva Agriscience, the Materials Science division will be the new Dow, and the Specialty Products division will be the new DuPont. We expect the new Dow to spin off in March. Following Dow, we expect Corteva and DuPont to split by June 2019. As illustrated in the following table, each division is a combination of Dow and DuPont’s businesses:

The logic of the merger followed by a split strategy appears counterintuitive. But one cannot underestimate how complex it is to combine so many different businesses residing under two separate corporate roofs. DowDuPont management believes that it is better to first put the various businesses all under one roof, then assemble the appropriate businesses, and spin off the new companies not until they are ready. Dow and DuPont merged in September 2017. Today, DowDuPont owns three industry-leading companies that trade at discounts to their peers. We believe the discounts will shrink and eventually disappear over the next year as management breaks up the company by spinning off three separate, publicly traded businesses.

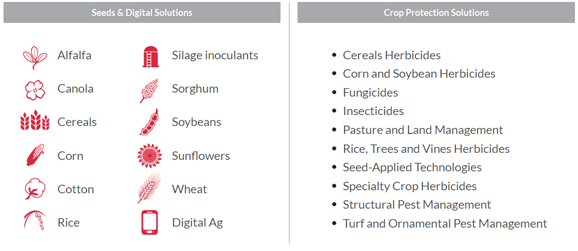

DowDuPont’s Agriculture division focuses primarily on seeds and crop protection—fungicides, herbicides, and insecticides—and has a presence in more than 130 countries. The Seeds business is the number two company in the world behind Monsanto, now part of Bayer AG. This business serves farmers growing alfalfa, canola, cereals (barley, oats, and rye), corn, cotton, rice, sorghum, soybeans, sunflowers, and wheat. The crop-protection company shares the number two position with ChemChina, after Bayer/Monsanto. Last year, Agriculture revenue was $14.3 billion, with pro forma earnings before interest, taxes, depreciation, and amortization of $2.6 billion. Dow and DuPont merged partly due to low prices and reduced planting of corn and soybean crops. ChemChina acquired Syngenta and Germany-based Bayer acquired Monsanto for similar reasons.

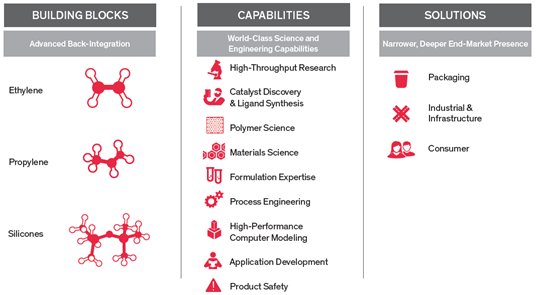

DowDuPont’s Materials Science division is the dominant materials science company in the world. The business uses the basic chemical building blocks of acrylics, silicon, cellulose, ethylene, and propylene to create products focused on the packaging, industrial and infrastructure, and consumer segments. Materials Science generated $43.8 billion of revenue in 2017 and $9.1 billion in operating earnings if one excludes one-time, mostly merger-related charges.

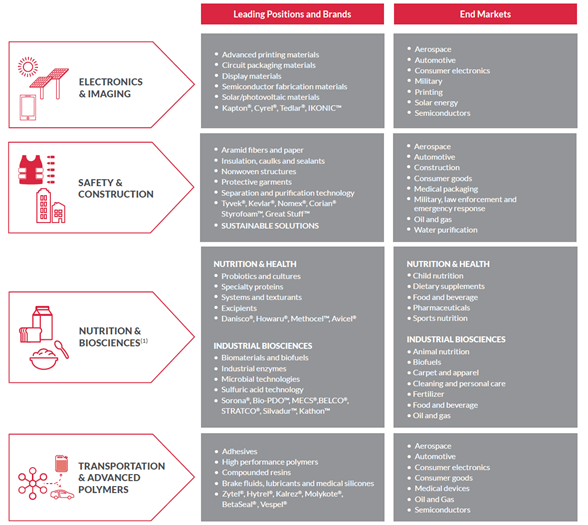

The Specialty Products division is a collection of several businesses, including the world’s largest supplier of electronics and imaging materials, plus industry-leading units serving the nutrition and bioscience, transportation and advanced polymers, as well as safety and construction industries. Once this division spins off as the new DuPont, management expects this standalone company to generate additional spinoffs. Specialty Products generated $21 billion of revenue in 2017 and $5.3 billion in operating profits.

We see a chance for the current DowDuPont discount to close then subsequently coupled with the potential revaluation of each individual business. We considered waiting for the spinoffs before investing but the current discount proved too compelling. DowDuPont now trades significantly below its original post-merger opening price back in September 2017. An investor now has an opportunity to own one of the world’s best chemical companies, one poised for the market to be revalue. Since the merger, DowDuPont business results have been solid, and the company has reduced costs post-merger faster than expected. We expect interest to increase in DowDuPont as we approach the spinoffs. Following the spinoffs, we expect a fair amount of price volatility as large institutional holders rebalance their portfolios. We expect the increased transparency and focus on the newly spun-off businesses to interest more investors.

Valuation

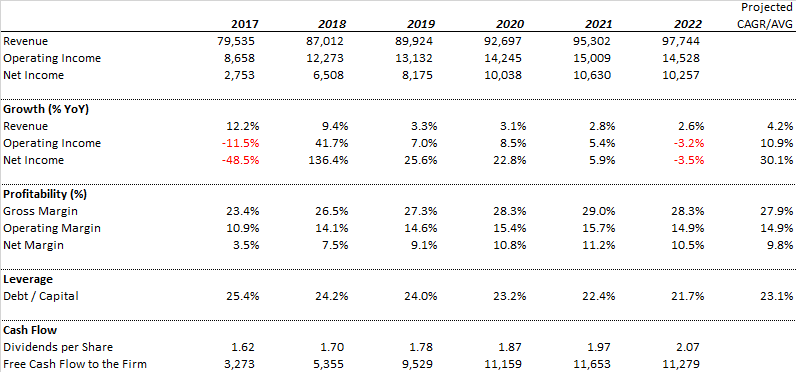

DowDuPont currently trades at a nearly thirty percent discount to our estimate of fair value. We see limited downside as quarterly earnings reports continue to demonstrate solid performance of its various business units. To arrive at our projections, we looked at the company’s valuation in two ways. First, we compared it with its three leading competitors. When combined, they generate revenue and operating profits that are comparable to DowDuPont. The table below shows DowDuPont revenue and profitability for the last two years, plus our estimates for the next four years.

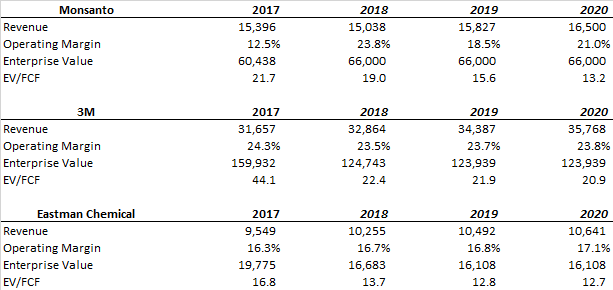

To better understand DowDuPont’s financial position, we present estimates for three of DowDuPont’s competitors: Eastman Chemical, 3M, and Monsanto before the Bayer acquisition.

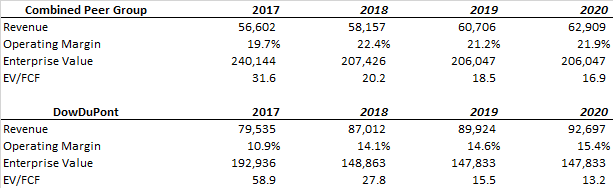

We subsequently compared DowDuPont with its peers by combining and presenting a consolidated look at the three companies. One notices that both DowDuPont’s revenue and operating profits will grow much faster through 2020. There are several reasons for this accelerated growth and profit. First, DowDuPont’s management expects annual expense reductions of $3.3 billion couple with growth synergies which should add $1 billion in annual revenues. Second, the company has a pipeline of new projects coming online which will organically improve the company’s financial performance. Lastly, the company’s agriculture division, Corteva Agriscience, will shortly launch several new products.

If these expectations materialize by 2020, DowDuPont will generate as much as fifty percent more revenue as three of its largest peers combined. Yet, if one invested an equal amount in all three peer companies, they would pay an average valuation of 18.5 times 2019 free cash flow. By contrast, one can buy DowDuPont today for about 15 times 2019 free cash flow and 13 times 2020 free cash flow. In other words, DowDuPont’s peer group trades at a 30% premium but will generate less revenue and free cash flow growth.

When comparing DowDuPont against a wider peer universe, one better understands the discount that currently exists. Looking at 2019 and 2020 consensus profit projections compiled by Capital IQ, one notices that the Materials Science division currently generates about 55% of DWDP’s operating profits, while Specialty Products accounts for about 32%, and Agriculture the remaining 13%. Assume these percentage profit contributions remain steady up until the expected spinoff dates. Using the valuation multiples of DowDuPont’s competitors against its various business units as listed in the company’s 2017 annual report, one immediately sees the valuation discount. We believe this discount will close and eventually disappear as each division spins off into its own separately traded company. In fact, we believe Corteva will eventually assert itself as the dominant company in the agriculture science industry and trade at a premium to its peer group.

Risk to Investment

The prices of raw materials are a concern. DowDuPont uses dozens of different raw materials, many petroleum-derived—a real risk for shareholders going forward. However, one should not over react to price increases. For example, higher prices of raw materials can cause the company’s costs to rise, but these higher raw material prices will also increase the value of the company’s raw-materials inventories that sit on its balance sheet. In many cases, we believe that DowDuPont can pass along cost increases to its clients.

DowDuPont operates various businesses around the world and sources raw materials from many countries. The risk of geopolitical events like terrorism, war, or political changes always exist. Then again, both Dow and DuPont have been around for more than a century and understand how to survive and profit in a globally competitive environment.

The risk that the company’s CEO, Ed Breen, might not be able to see the entire merger and divestment process through is also present. We believe that Breen has clearly demonstrated a unique skill set in breaking up a company to maximize shareholder value—an important consideration for our investment thesis. One must trust that Breen remains backed by a deep and talented management team.

I do not hold a position with the issuer such as employment, directorship, or consultancy. I and/or others I advise hold a material investment in the issuer's securities.

Are you sure you want to close this position DOWDUPONT INC?

By closing position, I’m notifying VIC Members that at today’s market price, I no longer am recommending this position.

Flag DOWDUPONT INC for Removal

Are you sure you want to Flag this idea DOWDUPONT INC for removal?

Flagging an idea indicates that the idea does not meet the standards of the club and you believe it should be removed from the site. Once a threshold has been reached the idea will be removed.

You Cannot Submit Message ... Yet

You currently do not have message posting privilages, there are

1 way you can get the privilage.

You can apply for full membership by submitting an investment idea of your own. Or if you are in reactivation status, you need to reactivate your full membership.