| 2022 | 2023 | ||||||

| Price: | 1.96 | EPS | 15.40 | 20.04 | |||

| Shares Out. (in M): | 393 | P/E | 13.1 | 10 | |||

| Market Cap (in $M): | 923 | P/FCF | 14 | 10 | |||

| Net Debt (in $M): | 205 | EBIT | 90 | 105 | |||

| TEV (in $M): | 1,207 | TEV/EBIT | 10 | 9 | |||

Sign up for free guest access to view investment idea with a 45 days delay.

Description

We believe the branded cider and beer manufacturer C&C Group has fundamentally transformed its business over the last several years through the acquisition of a UK beverage distributor, Matthew Clark, and the appointment of David Forde as CEO. Market share gains in new outlets and branded penetration in outlets set the company up to approach double digit profit growth in the medium term after fully recovering from the pandemic. C&C has a strong balance sheet and the cash generative nature of the business creates scope to return more than half the current market cap over the next several years.

Shares are extremely undervalued at 8.5x free cash flow. Put simply, despite recent revenues 15% above pre-COVID levels and cost savings equal to 15% of pre-COVID EBIT, C&C’s enterprise value is 33% below pre-COVID. We see 170% upside to shares through Feb 24.

Business Overview

C&C is a branded cider and beer manufacturer in the UK and Ireland with leading brands Tennet’s, Bulmers, Magners, Orchard Pig, among others. C&C is a vertically integrated manufacturer with wholesale distribution businesses in Ireland, Scotland, and now the UK through the acquisition of Matthew Clark Bibendum. Bulmers and Tennent’s have very strong market share in their respective geographies i.e. Ireland and Scotland, while C&C has struggled to grow share in the UK.

C&C, through its distribution business as well as branded business, has significant exposure to on-trade (pub, restaurant, bar, etc.) sales, which caused the company to face pressure during the COVID pandemic. EBITDA (pre-IFRS 16) during FY20 fell to -€50M and the company raised capital through a rights issue in May 2021. New CEO, David Forde, joined the company in January 2021 from Heineken, where he was most recently MD of Heineken UK.

Investment Thesis

1. Acquisition of Beverage Distributor, Matthew Clark, has transformed the group into a leading vertically integrated beverage company in the UK and Ireland

2. Significant evidence of recovery of UK on trade and C&C’s market share gains

3. New CEO David Forde has the right capabilities and strategy to drive growth and shareholder value

4. Strong existing balance sheet, cash conversion, and organic growth opportunity support significant capital return over the next several years

5. Share price is currently discounting a GFC-like recession and valuation or full inflation impact

1. Acquisition of Beverage Distributor, Matthew Clark, has transformed the group into the leading vertically integrated beverage company in the UK and Ireland

- C&C group was last written up by Straw1023 in April 2018 which outlined the merits of C&C’s acquisition of Conviviality (Matthew Clark Bibendum)

- C&C had business and share price momentum prior to the pandemic as investors began to appreciate its strategy and benefits of the transaction started to be reflected in financials

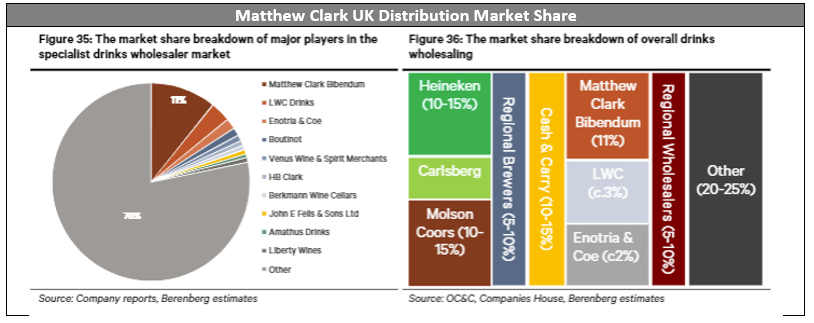

- C&C now operates the largest distribution network in the UK and Ireland with scale economies benefiting C&C and customers as it invests to improve its value proposition

- Launched new data platform for market insights PROOF, onboarded customers onto in online ordering platform, and launched new supplier portal

- Reach into the UK and Ireland makes C&C a must use for coveted brands and creates potential for exclusive relationships for brands seeking to expand in the UK and Ireland

- Distribution provides critical advantages as regulatory, industry structure, and sustainability trends make traditional marketing channels less effective for alcohol brands

- Consumer choice increasingly being made at point of sale because of proliferating options, driving benefits for distributors that can get beverages on taps

- On trade distribution increases awareness as traditional marketing and advertising channels are facing growing challenges from government restrictions

- Restrictions on advertising and marketing include advertising blackouts, sport sponsorship bans, and separation of alcohol from other goods in stores

- Minimum unit pricing, now in Scotland and Ireland, limits the ability for new or existing brands to gain share and build awareness through lower pricing

- Improvements in efficiency and sustainability by consolidating distribution into fewer players, benefiting the largest distributors in the market

- Distribution has been a critical ingredient of C&C’s playbook in Ireland and Scotland where its brands Bulmers and Tennent’s have dominant market share, but lack of distribution was a barrier to success in the UK

- Bulmers has 65% of the on-trade cider market and Tennet’s has 48% of Scotland’s volume share of lager, whereas C&C has just 13% of cider across the UK and Ireland

2. Significant evidence of recovery of UK on trade and C&C’s market share gains

- Reopening in the UK and Ireland supports our view that consumers want to return to the on trade

- C&C has navigated the pandemic while not only protecting its customer base but also growing market share

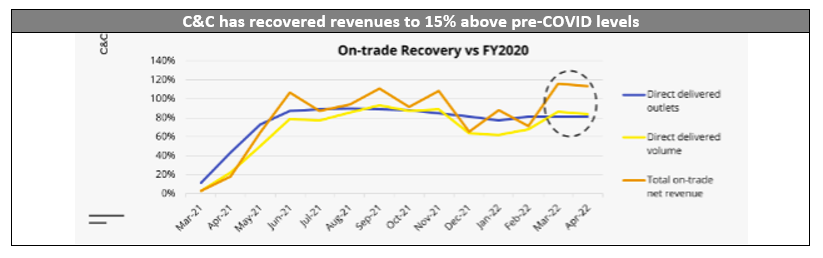

- C&C’s net revenue grew 15% in March and April vs pre-pandemic levels, despite delivered outlets returning to 80-85% of FY20 levels

- Outlet levels lagging pre-COVID levels are driven by pub closures and C&C culling low revenue and lower opportunity customers (e.g., facility that purchases a single pack of water)

- Net revenue has outpaced pub and bar drink sales, indicating share gain for C&C through the pandemic

- Higher net revenue per direct delivered outlet drives higher margins, which C&C confirmed during its CMD with the statement that March and April profit margins were slightly better than FY20 levels

- The periods of reopening in June 21, September 21, and November 21 have proven that the on-trade will come back and C&C will be able to restart its business to serve customers profitably.

- We believe, the likelihood of more restrictions has fallen due to the large base of immune protection from vaccines and infection across the population, other tools to fight the disease e.g. Paxlovid, Monoclonal Antibodies, etc. and declining population support for restrictions.

- C&C has been able to win new customers throughout the pandemic in the UK, where competitors have had weaker balance sheets and capabilities in serving customers

- Britvic exited the Irish market and we estimate their Irish business was 1/3 of the size of C&C’s Irish distribution business

3. New CEO David Forde has the right capabilities and track record to drive shareholder value

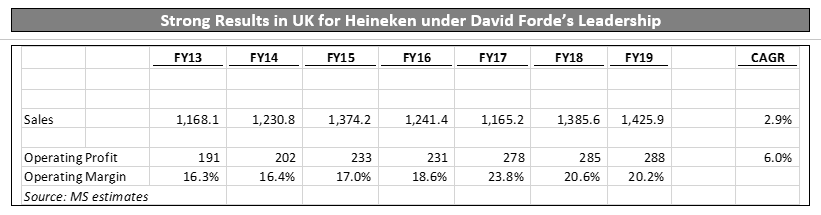

- David Forde joined C&C from Heineken UK and we think he brings the right mix of operational discipline, and growth orientation to drive shareholder value

- Forde spent 32 years at Heineken, notably his last 7 years as Managing Director of Heineken UK and the previous 4 years as MD of Heineken Ireland

- He has attracted several people from Heineken, including the UK marketing director Lucy Henderson who had a strong presentation at the capital markets day

- Forde has a strong track record at Heineken UK where he grew sales LSD, increased operating profits MSD, and expanded margins by 25% during his tenure

- Forde outlined a simple strategy at his capital markets day centered on using C&C’s distribution to customers, and share of wallet with a focus on growing cider and premium beer

- C&C plans to increase direct brand marketing investment from MSD to 10% over time by allocating new investment across several brands with significant growth potential

- The company plans to increase marketing investment over time to support accelerated growth while delivering margin expansion

- There is considerable runway for expansion in both cider and premium beer where C&C has 13% and 4% share respectively with premium beer being 2x the market size of cider and a very large market

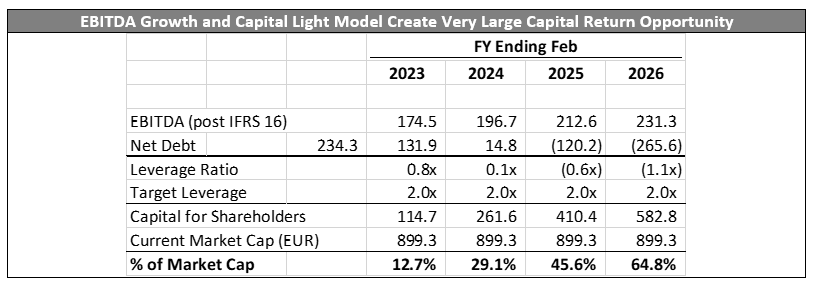

4. Strong existing balance sheet, cash conversion, and organic growth opportunity support significant capital return over the next several years

- Management believes that C&C has all the assets that it needs to succeed, will be focused on organic growth, and does not need to make significant capital investments to support growth

- Agency brands and partnerships augment C&C’s organic growth and support the company’s capital light approach to growth

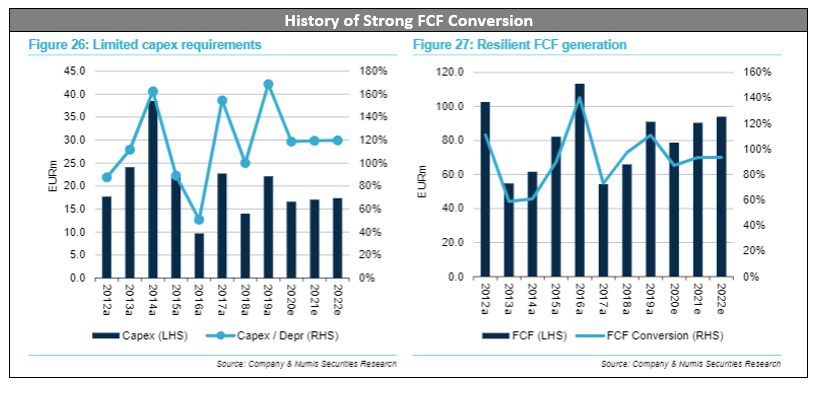

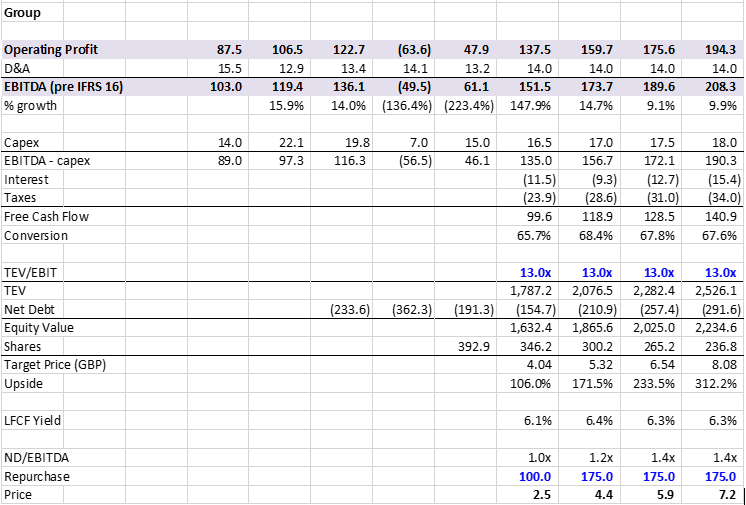

- Capex expectations of 15-17M over the medium-term equivalent to just 10% of EBITDA (equivalent to the company’s pre-IFRS 16 depreciation charge)

- Management guided to medium term 65-75% cash conversion, however, prior to COVID C&C’s branded business averaged 90% conversion which could make the 65-75% conservative

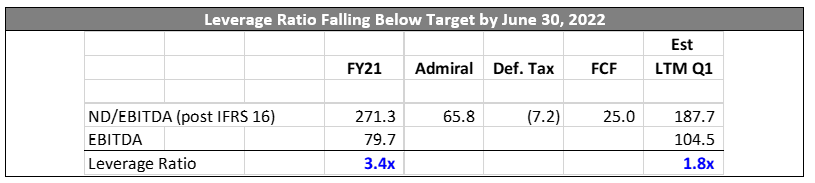

- C&C’s net debt is below pre-pandemic levels and leverage will rapidly approach target ND/EBITDA of 2.0x in the next quarter, enabling the company to begin capital returns

- Lapping periods of lock down in Spring 2021, the sale of Admiral Tavern, free cash generation will bring C&C net debt below 2.0x enabling capital returns at the half year

- Low leverage, high cash conversion, EBITDA growth, and cheap shares create a very attractive share repurchase opportunity for C&C over the next several years

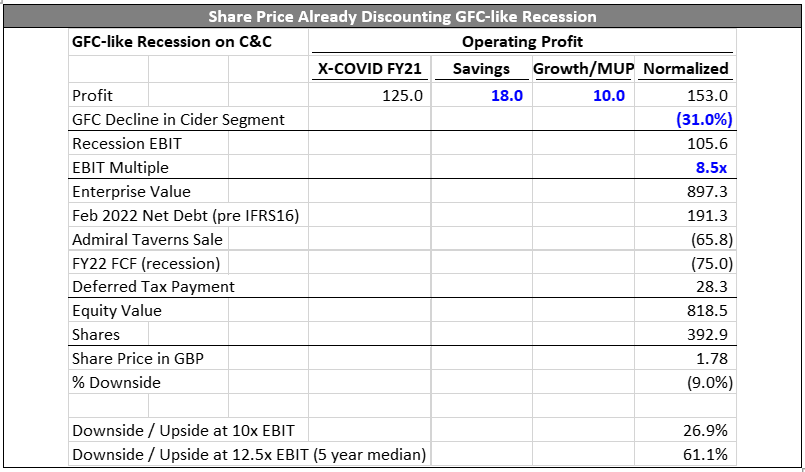

5. Share price is already discounting a GFC-like recession and valuation or full inflation impact

- C&C shares appear to be discounting a GFC-like impact to profitability and valuations from profit levels normalized from operating improvements, industry benefits (MUP), and growth

- In FY09, C&C’s operating profit in its cider division declined 31%

- Shares traded at an average EBIT multiple of ~8.5x (shares briefly traded lower to 6.75x from Oct 2008 to Feb 2009)

- Unemployment rate increased to 7.5% in the UK and 12.6% in Ireland vs 3.7% and 4.7% respectively today

- We believe there would be less than 10% downside to C&C’s share price.

- Sales, profits, and C&C’s multiple all rebounded the subsequent year.

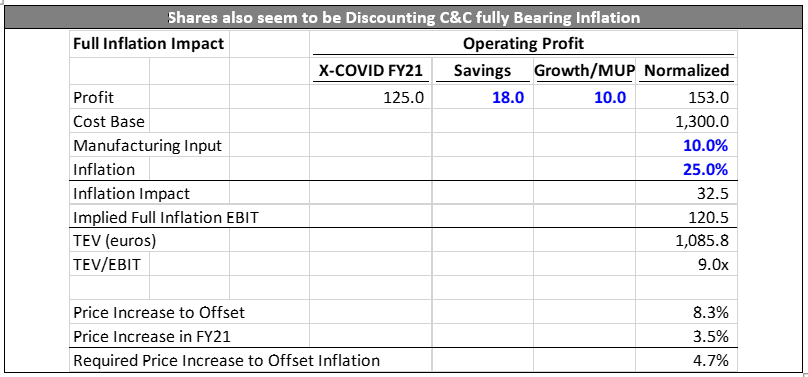

- Shares also seem to be fully discounting C&C enduring the full impact of inflation on the company’s profits

- C&C is fully hedged for FY23, but would face inflationary headwinds starting in FY24

- C&C’s cost base has experienced a 25% weighted average increase in cost at market rates, which would drive a €32M headwind to profits.

- Excluding any pricing actions, normalized profits would equal 120M and shares would be trading at 9.0x EBIT multiple, a 33%+ discount to the 5-year median EBIT multiple

- Offsetting this inflation seems manageable, requiring just a 5% additional price increase after the company’s 3.5% price increase in the fall of 2021

Valuation

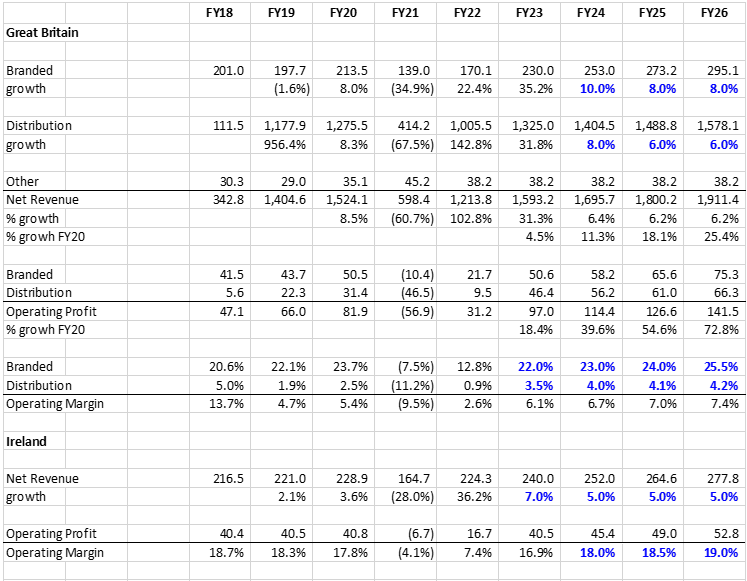

- We believe C&C will fully recover sales and profits in FY23 and benefit from investments in cost structure reduction and market share gains from the pandemic

- C&C guided to MSD to HSD EBITDA growth prior to the pandemic, but we believe the outlook for the group has improved significantly from industry changes through the pandemic, and new leadership

- The company is off to a strong start with March / April sales +15% vs FY20 and slightly better profitability, and has grown its customer base 12% since the start of the year

- Over the medium term, we believe these changes will drive near double digit EBITDA growth as Matthew Clark distribution margins expand to 400bps+, Matthew Clark continues to win new customers, and C&C builds tap share within outlets

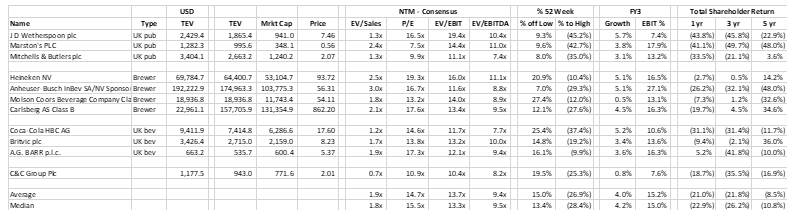

- As C&C increases its investment in its brands while sustaining margins and profit growth, we believe C&C shares should re-rate higher, and trade in line with UK vertical beverage companies such as AG Barr

Comparable Companies

Key Risks

- The UK consumer facing unprecedented inflation, reduces visits to pubs, bars, and restaurants

- Mitigant: the UK and Irish consumer has built up savings throughout the pandemic and has been unable to visit the on trade over the last two years. Unemployment remains and wage growth persists across the UK and Ireland

- Consumer preferences shift away from Cider to another beverage such as hard seltzer

- Mitigant: hard seltzer has launched with limited success in the UK and ireland

- UK pub landscape continues to consolidate driving more bargaining power in the hands of pub co’s

- Mitigant: Despite recent consolidation the UK on trade market remains highly fragmented

I and/or others I advise hold a material investment in the issuer's securities.

Catalyst

- Reporting strong results (trading update typically in first week of July)

- Issuing financial guidance

- Announcing a share repurchase and restarting dividend

| show sort by |