Description

Overview

We believe that the CVR created as part of the merger between BMY and CELG offers an attractive risk reward. The CVRs offer a $9 payoff if all three drugs are approved by the specified timelines. Clinical risk has been largely de-risked here, and thus it is highly likely that all 3 drugs will be approved. We estimate that approval probabilities are 80%, 85% and 70% respectively for ozanimod, JCAR017 and ide-cel, suggesting the CVR should be trading closer to $4.28 vs. its current $2.63. And though there is some timing risk (especially with the ide-cel approval) we believe the most likely scenario is that the CVR will be paid out in full - presenting a 200%+ return from the current price in the next 12-15 months.

CVR TERMS

This CVR was created as part of the merger of BMY and CELG. It will pay out $9 per share if all three conditions are met.

Each share also will receive one tradeable CVR, which will entitle its holder to receive a one-time potential payment of $9.00 in cash upon FDA approval of all three of ozanimod (by December 31, 2020), liso-cel (JCAR017) (by December 31, 2020) and bb2121 (by March 31, 2021), in each case for a specified indication.

Ozanimod

Ozanimod has been studied in Multiple Sclerosis and Crohn’s Disease. Ozanimod acts as a sphingosine-1-phosphate (S1P) receptor agonist, sequestering lymphocytes to peripheral lymphoid organs and away from their sites of chronic inflammation. Celgene gained rights to the compound through its acquisition of Receptos.

Ozanimod is on track to be approved by December 31st, 2020 and thus meeting the CVR criteria. In CELG’s 3Q19 earnings release they notes that that a PDUFA date has been set with March 25th, 2020. This is not a first in class compound, which increases our confidence in approval. Two S1P1 modulators (Gilenya and Mayzent) are already on the market.

With an established mechanism of action, ozanimod has shown efficacy largely consistent with other agents in the class with a 38-48% reduction in annualized relapse rate.

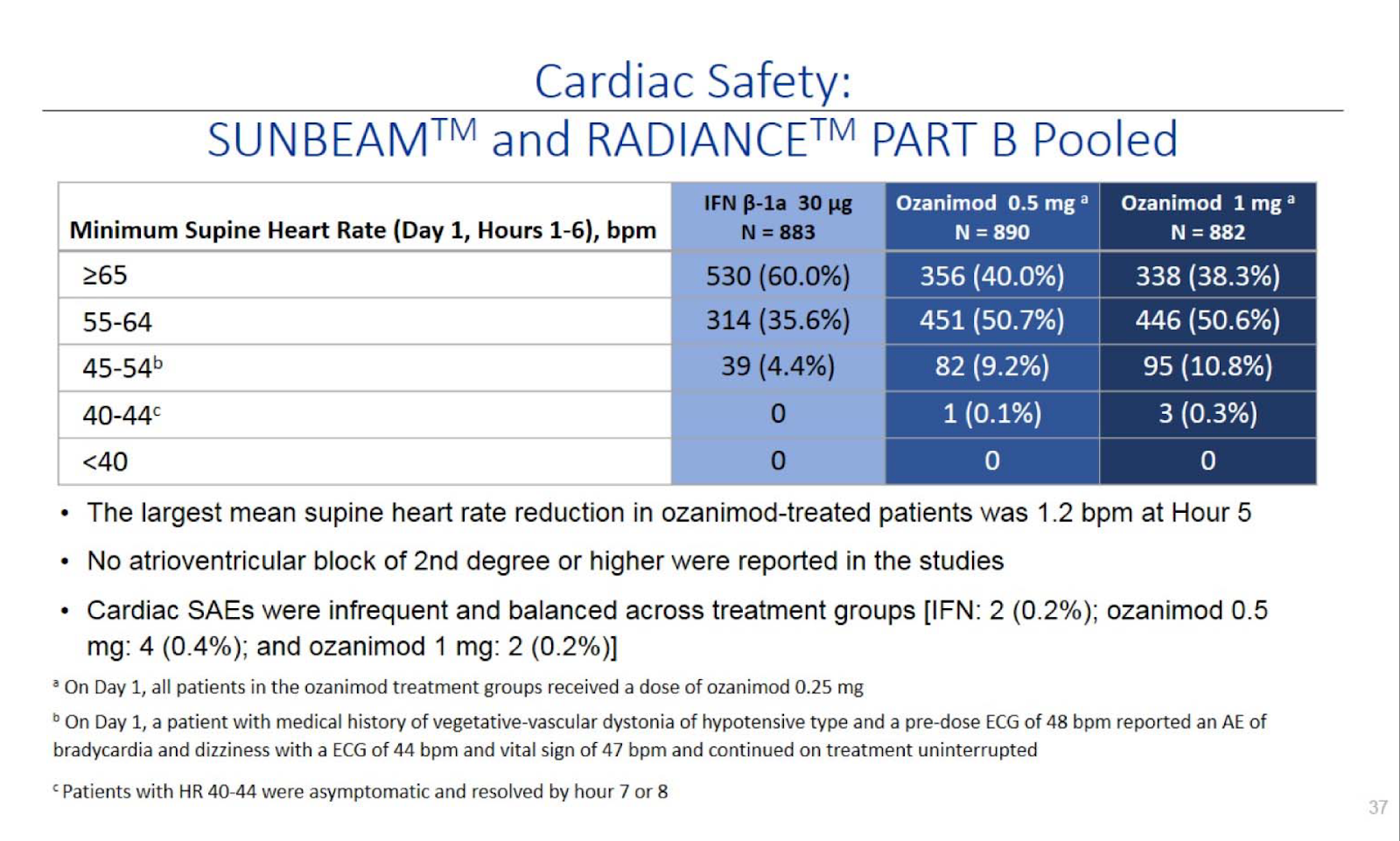

Cardiac safety is the largest concern with drugs of this class. Their 7 day titration schedule appears to avoid slowing of heart rate cconcerns.

Link to pivotal data

This is actually the second time this drug has been filed for approval. On February 27, 2018 CELG announced that it had received a Refusal to File (RTF) letter from the FDA for their ozanimod new drug application. This was related to a preclinical issue regarding a major active metabolite CC112273. The issue is that the company had not adequately characterized the metabolite, not that there were safety concerns. The metabolite accounts for 90% of ozanimod's activity and has very selectivity and potency as ozanimod for the S1P1 and S1P5 receptors.

On their 1Q18 earnings call CELG addressed the path forward for ozanimod. Celgene had a Type A meeting with the FDA and submitted a plan to address the concerns by bridging to the existing non-clinical data and will address the clinical pharmacology component by using PK/PD data.

Fundamentally it appears that the issue was incompetence on the regulatory team (and possibly lack of integration from the Receptos acquisition) that led to the RTF with the original filing, not an actual safety issue. Given the acceptance of the NDA filing this time around (an RTF letter means that the NDA is not accepted) and the overall safety and efficacy profile of ozanimod we believe there is a high chance of approval.

We believe given the known mechanism of action, and supportive safety and efficacy profile, that ozanimod has 80% chance of approval by the CVR date of Dec 31, 2020.

Liso-cel (JCAR017):

JCAR017 is a second generation anti-CD19 CAR-T treatment with the lead indication for NHL. JCAR017 was originally developed by Juno Therapeutics that had a strategic collaboration with CELG. CELG later acquired Juno in 2018 and gained full rights to JCAR017 and other T-cell therapies.

The efficacy profile of liso-cel shows that is largely comparable to existing therapies Yescarta and Kymriah. The major differentiation of liso-cel is on the safety side where the rate of grade 3 cytokine release syndrome (CRS) events was lower than the other agents.

Prior approvals in the CAR-T space of Yescarta and Kymriah were ~6-7 months after filing. CELG’s 3Q19 earnings release states that they expected BLA submission by YE and BMY confirmed this in December at their American Society of Hematology (ASH) presentation. This timeline is consistent to support approval before the December 2020 for the CVR requirement. JCAR017 received break-through designation (BTD) for the treatment of relapsed/refractory aggressive large B-cell non-Hodgkin lymphoma (NHL) in December 2016. This is one of the few designations from the FDA that is based on strength of data and suggests that the FDA will prioritize this review.

Given the known mechanism of action, comparable efficacy and better safety than approved agents, we think that JCAR017 has a high chance of success. With a filing due imminently and the relatively quick approval timeline for previous CAR-T therapies we believe there is an 85% chance of approval by the CVR milestone deadline.

Ide-cel (bb2121)

Ide-cel is a CAR T cell therapy targeting B-cell maturation antigen (BCMA), which is expressed on the surface of normal and malignant plasma cells. The ide-cel CAR construct includes an anti-BCMA scFv-targeting domain for antigen specificity, a transmembrane domain, a CD3-zeta activation domain, and a 4-1BB co-stimulatory domain hypothesized to increase T-cell activation, proliferation and persistence. Ide-cel CAR T cells are proposed to recognize and bind to BCMA on the surface of multiple myeloma cells leading to apoptosis.

In November 2017, ide-cel was granted Breakthrough Therapy Designation (BTD) by the U.S. Food and Drug Administration and PRIority Medicines (PRIME) eligibility by the European Medicines Agency based on preliminary clinical data from the phase 1 CRB-401 study.

Ide-cel is being developed as part of a Co-Development, Co-Promotion and Profit Share Agreement between BMS and bluebird bio (Ticker BLUE).

In early December, BMY released positive top-line data from their KarMMa study of ide-cel in relapsed and refractory multiple myeloma. Across all doses the overall response (OR) was 73.4%, and the complete response (CR) was 31.3%, with median duration of response (DoR) of 10.6 months among 128 relapsed/refractory multiple myeloma (MM) patients. For the high dose group, the results higher with and OR of 81.5%, CR of 35.2%, and median DoR of 11.3 months (the median follow-up duration for all patients). The safety data were consistent with what had been previously released.

Given the highly refractory population studied here and the strong rates of response and manageable safety, we believe this agent is likely to be approved.

At their ASH presentation BMY confirmed that they intend to file in the 1H 2020. With the March 31st, 2021 deadline to meet the CVR requirements there is some risk that if the filing occurs late in 1H 2020 and the FDA does not grant priority review that it may be approved by the deadline. However, given the BTD and the strong efficacy we would expect a priority review.

The strong efficacy in a heavily pre-treated population without other treatment along with the BTD gives ide-cel a strong case for FDA approval despite us not having seen the full Phase II data. There is some additional risk here on the timing side if BMY does not file until the end of 2Q 2020. Thus overall we would estimate a 70% probability of approval by the March 31, 2021 deadline.

I do not hold a position with the issuer such as employment, directorship, or consultancy.

I and/or others I advise do not hold a material investment in the issuer's securities.

Catalyst

Approval of drugs by milestone dates.