| 2011 | 2012 | ||||||

| Price: | 1.51 | EPS | $0.00 | $0.00 | |||

| Shares Out. (in M): | 77 | P/E | 0.0x | 0.0x | |||

| Market Cap (in $M): | 115 | P/FCF | 0.0x | 0.0x | |||

| Net Debt (in $M): | 0 | EBIT | 0 | 0 | |||

| TEV (in $M): | 115 | TEV/EBIT | 0.0x | 0.0x | |||

| Borrow Cost: | NA | ||||||

Sign up for free guest access to view investment idea with a 45 days delay.

- None found

- BETA

- PERRIGO CO PLC PRGO 03/08/2016

- INFORMATION SERVICES GROUP III 05/25/2017

- Daelim Industrial 000215 02/01/2014

- AMERIGO RESOURCES LTD ARG 05/20/2013

- SOFTBANK CORP 9984 02/22/2014

- Universal Stainless USAP 02/23/2023

- ADA-ES INC ADES 05/10/2013

- SUPERIOR INDUSTRIES INTL (SUP) SUP 02/15/2024

- ARES COMMERCIAL REAL ESTATE ACRE 04/23/2024

- PETMED EXPRESS INC PETS 08/09/2024

Description

Note: this is a slightly edited version of my application writeup, submitted March 28. I also posted it to Seeking Alpha at the end of March. Since then, the market cap has declined from $250 m to $115 m.

From a technical standpoint, the short is no longer as attractive as before, however, fundamentally the stock is worth zero and so the downside is still 100%. I remain short, though I have in the past and will in the future trade the position.

Some key events that have occurred since:

· The company responded to the original report, including some claims that I used faulty numbers. Their ‘new’ numbers contradict the numbers they previously filed with the SEC. Also, their response contains an admission that they had never owned their main operating subsidiary (HLJ ZQPT), which in their SEC filings they had been claiming to have purchased from their chairman for tens of millions of shares. I view this as essentially an admission of securities fraud.

· An anonymous short seller on Seeking Alpha posted SAIC filings showing revenue of approximately USD 2 m vs the company’s SEC filed revenue of approximately USD 50 m. The SAIC filings also show that the company generated losses every year from 2006 to 2009.

· Prescience Investment Group and Kerrisdale Capital jointly published a report claiming ABAT is a fraud. Their report confirmed the SAIC/SEC discrepancy and also included audiotaped conversations with a former customer of ABAT who claims that ABAT’s chairman directly told him that ABAT was a scheme to sell stock.

· The company filed its 10-Q report for 2011Q1. I consider it to be almost entirely a fiction.

Also, some quick comments on technicals:

· The stock has been easy to borrow. I have seen shares available every day, with inventory usually several hundred thousand shares and single digit rebate.

· Daily volume is about 2 million shares. I believe that quants and HFTs are fairly active in the name because it is a Russell 3000 component. As a side note, ABAT claims its primary office is in NY, when in fact that is a small IR office. I believe this is an attempt to game the Russell US Indexes. I believe ABAT also uses a misleading business description to game the cleantech index funds.

· Decently liquid options chain going out to Dec 2010.

· Reported short interest is 11% of float and about 4 days to cover.

· I consider ABAT a less risky short than most pump-and-dumps because I don’t believe that there remains any significant buying interest for Chinese RTO scams. Having said that, the company probably has the ability to generate a one-day move of 15% by putting out false information. I don’t think any of these moves would last long.

Original writeup (w/ minor edits):

I am short Advanced Battery Technologies (ABAT) for the following reasons:

- The Chairman appears to have transferred ownership of ABAT’s key subsidiary to himself without explanation or compensation

- ABAT leads investors to think that it makes cutting-edge electric cars, when in fact it produces cheap scooters and bicycles

- ABAT claims unrealistic margins in what it admits is a commodity space

- ABAT claims to have increased revenue from $4.2 million to $97.1 million from 2005 to 2010 while DECREASING its employee count

- ABAT claims distribution relationships which appear to be fake

- ABAT is a serial issuer of equity at low prices

- ABAT spent $20 million in 2011 to “acquire” a company that it had previously acquired for $1 million in 2008

- ABAT spent $22 million or 7x sales to acquire a failing and possibly related company

- ABAT issued 11 million shares to the Chairman and other individuals to repay a “loan” which appears to be entirely fabricated

- Despite a parade of auditors and multiple restatements, ABAT still has material weaknesses

- ABAT’s RTO promoter, John Leo, is behind a number of suspicious Chinese reverse mergers, most notably CYXI

- No fundamental institutions are significant shareholders

In short, I think that the financial statements and management of ABAT cannot be trusted and therefore the stock is worth zero.

BACKGROUND

Advanced Battery Technologies (ABAT) is a $250 million market cap company listed on the Nasdaq. The company originally went public through a reverse merger transaction with a shell company called Buy It Cheap.com in 2004. The company claims to have increased its revenues from $11 thousand to $97 million from 2003 to 2010.

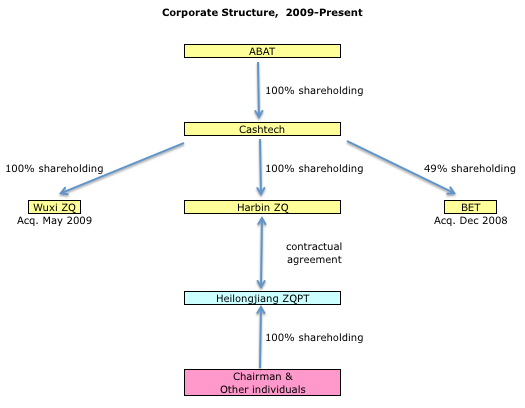

ABAT owns Cashtech Investment Limited (“Cashtech”), a BVI corporation which owns two Chinese entities, Harbin ZhongQiang Power-Tech Co. Ltd. (“Harbin ZQ”), and Wuxi ZhongQiang Autocycle Co. Ltd. (“Wuxi ZQ”), as well as a 49% interest in a Texas corporation named Beyond E-tech, Inc (“BET”).

Harbin ZQ is a non-operating shell that has a contractual arrangement to receive all of the "benefits and responsibilities" of an operating entity called Heilongjiang ZhongQiang Power-Tech Co., Ltd. (“HLJ ZQPT”).

According to the 10-K:

- HLJ ZQPT “is engaged in the business of manufacturing and distributing polymer lithium-ion batteries”

- Wuxi ZQ “is engaged in the business of manufacturing and distributing electric vehicles”

- Beyond E-tech “distributes cellular telephones in the United States”

THE SHORT CASE

The Chairman appears to have transferred ownership of ABAT’s key subsidiary to himself without explanation or compensation

In the 2007 10-K and 2008 10-K, HLJ ZQPT is described as the 100%-owned subsidiary of Cashtech:

Cashtech Investment Limited is also a holding company with only one subsidiary: Heilongjiang ZhongQiang Power-Tech Co., Ltd., a China limited liability company (“ZQ Power-Tech”). Prior to January 2006, Cashtech Investment Limited owned 70% of the capital stock of ZQ Power-Tech. In January 2006 our Chairman, Fu Zhiguo, transferred the remaining capital stock of ZQ Power Tech to Cashtech Investment Limited, so that it now owns 100% of ZQ Power-Tech.

Yet, in the 2009 10-K, we suddenly learn that HLJ ZQPT is actually owned by Chairman Fu again, without any explanation of how he reacquired ownership:

HLJ ZQPT is owned by our Chairman, Mr. Fu and other individuals but controlled by Harbin ZQPT through a series of contractual arrangements that transferred all of the benefits and all of the responsibilities for the operations of HLJ ZQPT to Harbin ZQPT.

The filing fails to mention that this structure is different than the previously disclosed structure.

I searched every SEC filing by the company between the 2008 10-K and the 2009 10-K. As late as the 10-Q filed on August 11, 2009, the company continued to claim ownership of HLJ ZQPT without ever mentioning Harbin ZQ.

The first mention of Harbin ZQ is in an S-3 filing dated August 17, 2009. However, this filing contains no disclosure of the VIE arrangement or Chairman Fu’s ownership.

The only other mention is in the 10-Q filing dated November 9, 2009. Here, we are finally told of the VIE arrangement, but the filing fails to mention that the VIE structure is different than the previously disclosed structure, nor are we told that Chairman Fu owns Heilongjiang ZQPT.

The 10-Q does say that they are now consolidating the results of both Harbin ZQ and HLJ ZQPT, and they refer to the change of accounting standards under topic ASC 810, consolidation. Specifically, they are referring to SFAS 166 and 167 (June 2009).

SFAS 166 requires additional information about financial assets and securitizations, as well as eliminating the concept of a Qualifying SPE. SFAS 166 primarily affects banks and other financial institutions, not manufacturing businesses like ABAT.

SFAS 167 changes the assessment process for what entities must be consolidated. It also expands certain disclosures, specifically, separation of certain VIE assets and liabilities on the balance sheet, disclosure of certain risks, restrictions, and assumptions made during the consolidation process.

However, what SFAS 166 and 167 DO NOT DO is affect in any way how companies represent their ownership of subsidiaries or VIEs. In other words, I’m pretty sure that if ABAT did not own HLJ ZQPT, then representations to the contrary would be considered securities fraud, either prior to or after SFAS 166/167.

If the filings are accurate, the Chairman transferred ownership of the company’s sole operating subsidiary to himself without explanation or compensation. If the filings are inaccurate, then the company is guilty of misrepresenting itself as previously owning 100% of HLJ ZQPT, when in fact it did not (and remember, the company issued millions of shares to Fu supposedly in exchange for his holdings of HLJ ZQPT).

Either way, this is the most egregious action by any Chinese RTO management that I have witnessed, and that’s quite a tough competition to win.

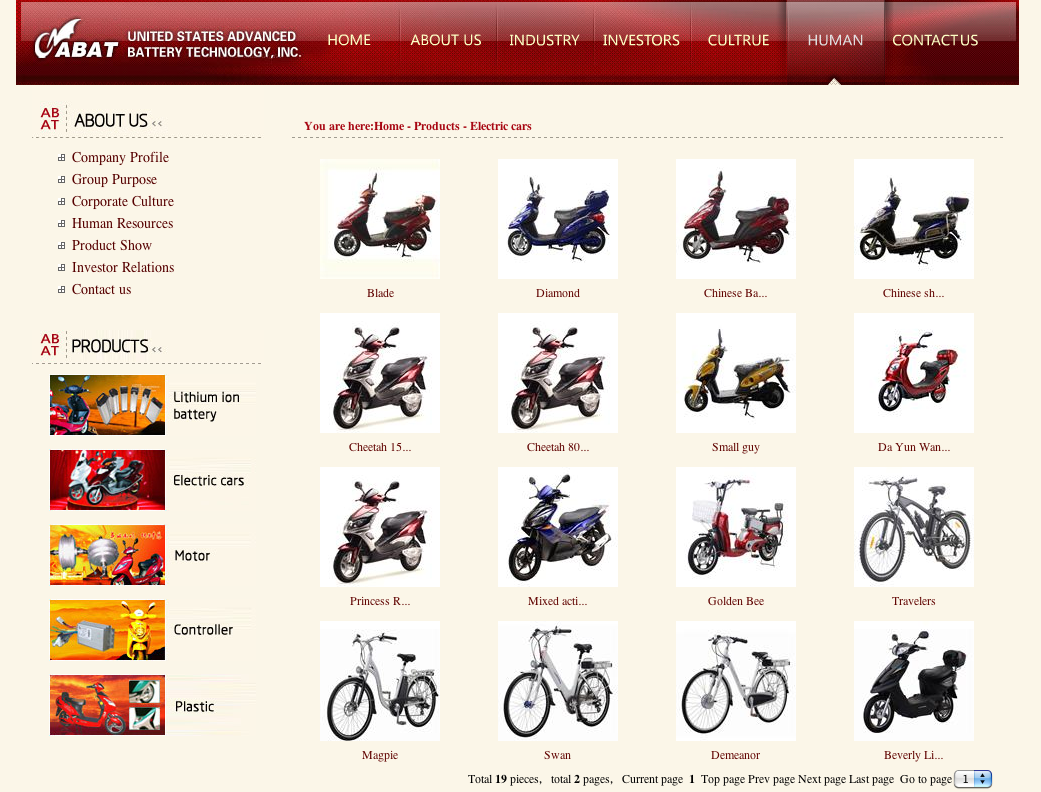

ABAT leads investors to think that it makes cutting-edge electric cars, when in fact it produces cheap scooters and bicycles

ABAT represents that its subsidiary Wuxi ZQ “is engaged in the business of manufacturing and distributing electric vehicles”. On its website, under “products”, the company lists “electric cars” as one of its product categories.

The 10-K also states:

Since 2002, Wuxi ZQ has been engaged in the design, development, manufacture and marketing of electric- and hybrid-powered two wheel vehicles, as well as electric-powered agricultural transport vehicles and sport utility e-vehicles . [emphasis added]

This sounds exciting: electric SUVs! An unsuspecting investor might place ABAT into the same category as high tech companies like Tesla Motors or BYD.

Yet the 10-K continues: “The prices of Wuxi ZQ vehicles range from $427 to $3,471, with an average selling price of $574.” Let’s assume that the e-SUVs are at the high end of that range, $3,471. This would be an astoundingly cheap price and I am shocked that the company has not yet taken the world by storm with a three thousand dollar electric SUV.

The company website, despite having many photos of its products, shows not one single electric car, SUV, or agricultural vehicle. The photos are of cheap electric scooters and bicycles.

To emphasize this point, one does not normally think of Amazon.com as a place where one would purchase vehicles, electric or not. And yet, Amazon sells exactly the same type of cheap scooters and bicycles that ABAT makes, offered by many different companies (clearly it is a commodity product).

ABAT claims unrealistic margins in what it admits is a commodity business

ABAT’s 10-K states:

The technology utilized in producing polymer lithium-ion batteries is widely available throughout the world , and is utilized by many competitors, both great and small. ZQ Power-Tech’s patents give it some competitive advantage with respect to certain products. However, the key to competitive success will be ZQ Power Tech’s ability to deliver high quality products in a cost-efficient manner. This, in turn, will depend on the quality and efficiency of the assembly lines that we have been developing at our plant in Harbin. [emphasis added]

In other words, the company admits that LiPoly batteries are a commodity. This should come as no surprise: LiPoly batteries have been available in consumer electronics since 1996. An examination of ABAT’s patent portfolio does not reveal any IP that would give it any substantial advantage.

Evidence that ABAT has no special technology is found in its R&D expenditures:

|

($'000) |

R&D |

Revenue |

R&D %Rev |

|

2004 |

$65 |

$1,191 |

5.46% |

|

2005 |

$143 |

$4,222 |

3.39% |

|

2006 |

$185 |

$16,329 |

1.13% |

|

2007 |

$383 |

$31,897 |

1.20% |

|

2008 |

$4 |

$45,172 |

0.01% |

|

2009 |

$348 |

$63,561 |

0.55% |

|

2010 |

$204 |

$97,128 |

0.21% |

Note: The company claimed a 2005 R&D expense of $32 in the 2005 10-K, but changed this number without explanation to $143 in the 2006 10-K. In the table, I gave them the benefit of the doubt and used $143, but I think that $32 is more likely to be the correct figure.

2010 R&D expense was 0.2% of its claimed revenues. So one would not expect ABAT to have significant technology to enable better margins than its competitors. Yet, looking at its public comps (I am being generous with the word “comp”), no one is even in ABAT’s ballpark:

|

|

Gross Margin |

Op Margin |

Net Margin |

R&D % |

R&D $m |

|

ABAT'10 |

52.7% |

38.9% |

37.8% |

0.2% |

$0.2 |

|

ABAT'09 |

44.6% |

28.5% |

34.3% |

0.6% |

$0.3 |

|

Wuxi'08 |

9.4% |

-25.9% |

-39.9% |

4.4% |

$0.4 |

|

VLNC |

12.7% |

-113.4% |

-146.5% |

27.5% |

$4.4 |

|

AONE |

-17.9% |

-153.4% |

-156.7% |

62.4% |

$60.7 |

|

ENS |

22.9% |

7.0% |

3.9% |

undisclosed |

undisclosed |

|

TSLA |

25.9% |

-125.9% |

-132.8% |

79.3% |

$37.6 |

|

BYDDY |

21.6% |

11.9% |

9.4% |

3.2% |

$195.6 |

This doesn’t make much sense: ABAT manufactures commodity products with expensive ingredients. The rest of the industry is having trouble turning a profit. Yet, ABAT claims margins that would make Google jealous.

Now, before you say that ABAT has a lower cost structure because it is in China, of course this cannot be the explanation because its competitors also manufacture in China or other low cost countries, and regardless, ABAT has a number of domestic competitors who should have compressed industry margins. Manufacturing in China is a notoriously low margin business.

The main difference between ABAT in 2009 and 2010 is the addition of Wuxi. Since consolidated margins improved significantly YoY, Wuxi’s implied post-acquisition gross margin was about 60% and op/net margins about 40%. These are absolutely ridiculous claims given that Wuxi had pre-acquisition gross, op, and net margins of 9.4%, -25.9%, and -39.9%.

ABAT claims to have increased revenue from $4.2 million to $97.1 million from 2005 to 2010 while DECREASING its employee count

|

($'000) |

Revenue |

SG&A |

Employees |

Rev/Emp |

SG&A/Emp |

|

2004 |

$1,191 |

$2,811 |

362 |

$3.29 |

$7.77 |

|

2005 |

$4,222 |

$1,221 |

1,261 |

$3.35 |

$0.97 |

|

2006 |

$16,329 |

$1,604 |

1,264 |

$12.92 |

$1.27 |

|

2007 |

$31,897 |

$3,283 |

1,262 |

$25.27 |

$2.60 |

|

2008 |

$45,172 |

$3,263 |

909 |

$49.69 |

$3.59 |

|

2009 |

$63,561 |

$9,890 |

854 |

$74.43 |

$11.58 |

|

2010 |

$97,128 |

$7,842 |

1,176 |

$82.59 |

$6.67 |

Also note that the 2009 and 2010 employee counts include employees of Wuxi ZQ. It is amazing that the consolidated employee count decreased even as ABAT acquired a new subsidiary that accounts for almost all of its 100% revenue growth from 2008 to 2010.

Fraud is a more likely possibility than employee efficiency growing 25x over 5 years in a commodity manufacturing business.

ABAT claims distribution relationships which appear to be fake

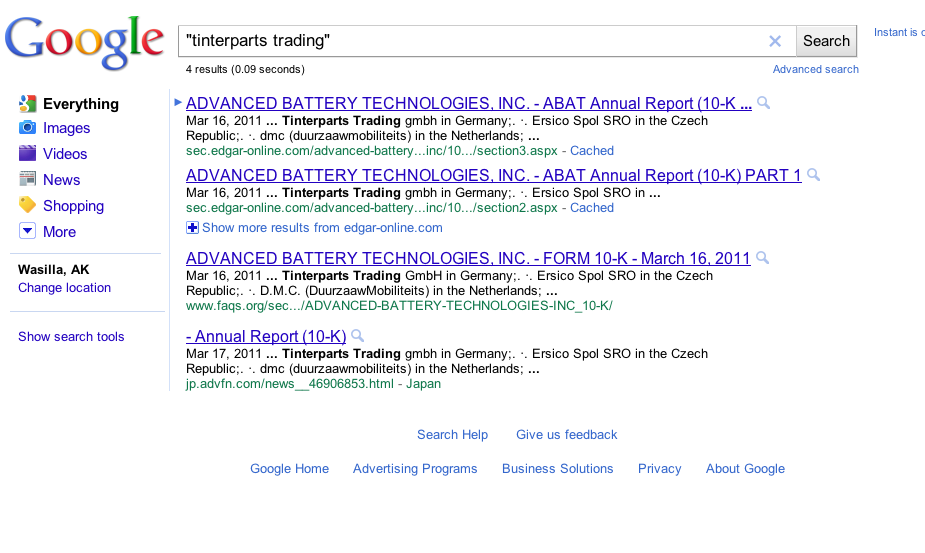

ABAT claims in its 10-K report, “In May 2010 Wuxi ZQ signed an agreement with All-Power America to serve as the first U.S.-based distributor for Wuxi ZQ since the May 2009 acquisition.” All-Power’s website does not even mention electric scooters or bicycles.

I spoke with an employee of All-Power America who has access to a list of APA’s suppliers. This person told me that although one of APA’s subsidiaries sells electric scooters, Wuxi ZQ is not one of that subsidiary’s suppliers. The person I spoke with had never even heard of Wuxi ZhongQiang Autocycle Co.

I also questioned a manager at Kuralkan, the sole manufacturer, distributor and exporter of Kanuni motorcycles since 1995, which Wuxi claims a relationship with. This manager stated, “We do not know this company [Wuxi ZQ].” He also confirmed to me that Kuralkan is the only manufacturer of Kanuni motorcycles. (“Kanuni” is the name of the Kuralkan boss’s son).

Another purported distributor, “Eco Style Di in Italy” has a nonsensical name, as the word di is Italian for of. I tried looking up “Eco Style” instead, and that company does not appear to have any business related to distributing scooters or bicycles.

Other purported Wuxi distributors seem to not exist at all. A Google search for the following names did not have any search results besides ABAT filings:

How likely is it that in 2011 a legitimate company would not have a website or any search results at all? What are the odds of a “coincidence” involving several of Wuxi’s purported distributors having no websites or search results?

ABAT is a serial issuer of equity at low prices

- In August 2008, the company issued 5 million common shares and warrants to purchase an additional 2.6 million shares.

- In June 2009, the company issued preferred stock that converts into 4.3 million common shares and warrants to purchase an additional 3.5 million shares.

- In December 2010, the company issued 7.5 million common shares and warrants to purchase an additional 3.7 million shares.

In addition to the equity sales, the company also issued, in aggregate, at least 30 million shares for acquisitions and a suspicious “loan repayment” (at least 26 million of these shares went to Chairman Fu and friends).

If the financial statements are believed, then these issuances were done at unreasonably low P/E multiples at times when the company had significant net cash balances. The only possible explanations are that (1) the financial results are inflated, (2) the counterparties are related and getting a sweetheart deal, or (3) the management is incredibly stupid.

In my opinion, issuing shares at absurdly low prices to fund opaque transactions is one of the most serious red flags that a public company can have.

ABAT spent $20 million in 2011 to “acquire” a company that it had previously acquired for $1 million in 2008

[Note: I have edited this section to incorporate information from a later article of mine]

In January 2011, the company claimed that it acquired Shenzhen Zhongqiang New Energy Science & Technology Co., Ltd. (“Shenzhen ZQ”) (??????????????) for 135 million RMB (about $20 million).

However, this Shenzhen government registration, dated September 10, 2008, shows that Shenzhen ZQ changed its Legal Representative and Executive (Managing) Director from Huang Youlin (???) to Fu Zhiguo (???).

This transaction was mentioned in a lawsuit filed by Huang’s son against ABAT, in which the younger Huang claims ABAT reneged on its employment agreement. Huang also claims that he received death threats from Fu Zhiguo after he threatened to file a lawsuit.

ABAT acquired the Huangs’ company for $1 million and renamed it Shenzhen ZQ in 2008; two years before they told the public that they acquired it for $20 million. We believe that this connection was overlooked because the court regularly refers to Shenzhen ZQ as “Shenzhen ABAT” or “SABAT”. However, as a motion filed by ABAT’s own attorneys makes clear, SABAT is simply an “English rendition” of the company’s real name, Shenzhen Zhongqiang Energy Science and Technology Co. Ltd.

The PACER docket also includes a sworn affidavit from Chairman Fu indicating that ABAT purchased this company in 2008 for $1 million.

ABAT spent $22 million or 7x sales to acquire a failing and possibly related company

[Note: I think the following is a pretty generous analysis based on the SEC filed numbers. If you look at the SAIC filings, it is even uglier]

In 2009, ABAT paid $3.64 million, 70 million RMB, and 3 million common shares to acquire Wuxi Angell (later renamed Wuxi ZQ), the producer of electric scooters and bicycles. Previously, ABAT had advanced Wuxi $3.81 million. Note that the purchase agreement does not mention the advance, and the consideration amounts do not appear to include it. So the total acquisition cost may be over $25 million.

Wuxi had a book value of $9.6 million at March 2009; a net loss of $3.7 million in 2008, and a net loss of $1.1 million in 2007. Its gross profit actually declined by 35% from 2007 to 2008. Revenue was rapidly contracting: 2009 Q1 revenue was $0.75 million, or down 63% year over year.

Working capital position was negative $15 million. Cashflow from operations in the first quarter was negative $4.1 million. Wuxi had been sued five times and brought to arbitration over bad debts. The company lost all six cases and had not repaid any of the debts at year-end 2008.

The situation was so dire that the auditor issued a going concern warning and Wuxi had to take a $3.8 million “advance” from ABAT a few months prior to the acquisition. ABAT should have been purchasing Wuxi in bankruptcy court, not at over 2x a questionable book value.

The pro-forma statement of operations (page F-40) is very enlightening.

|

($'000) |

ABAT |

Wuxi Angell |

Intercompany Eliminations |

PF Combined |

Wuxi Net Contribution |

|

2008 Rev |

45,172 |

9,332 |

6,079 |

48,425 |

3,253 |

In other words, after eliminating the battery revenue that ABAT was previously getting from Wuxi, ABAT was paying 7x FY08 revenue for a business that was about to go bust. If we estimate SAAR from the 2009 Q1 revenue number, and use the same intercompany elimination percentage, we get an absurd price of 18x sales.

Subsequent revenue growth numbers seem impossible. As a standalone company, Wuxi generated an estimated $1 million revenue in the first four months of 2009. Yet, ABAT claimed $20 million of “electric vehicle” revenue in 2009, which means that average monthly sales grew by 9.5x from the first four months of the year to the last eight months of the year. Meanwhile, the combined companies had fewer employees at year-end 2009 than legacy ABAT alone at year-end 2008.

ABAT claims that Wuxi’s shareholders are not related parties to ABAT, but it also says that one of the owners, Bao Jin, was a major shareholder of ABAT, with one million shares. Chairman Fu agreed to buy his ABAT shares “in order to facilitate the purchase of Wuxi Angell.” The majority owner of Wuxi was a Chinese entity whose shareholding is opaque. Also, Wuxi was audited by Bagell Josephs Levine, the same firm that was auditing ABAT at the time. Despite ABAT’s claim of non-relatedness, it is hard to believe that these individuals were not friendly, especially since ABAT clearly overpaid for Wuxi.

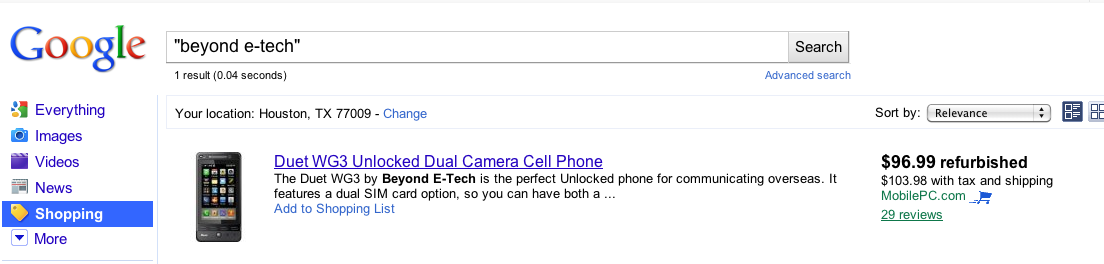

ABAT spent $1.5 million on another suspicious transaction

Quoting the 10-K:

In December 2008 Advanced Battery Technologies purchased a 49% equity interest in Beyond E-Tech, Inc. (BET), a corporation located in Texas that distributes cellular telephones manufactured in China to its order by Flying Technology Development Co. and Lenovo China. The purchase price for the shares was $1.5 million cash.

A search of Beyond E-Tech shows that BET-branded phones exist, but as the 10-K reveals, these are simply white label devices purchased from ODMs. It looks like BET sent some samples to review websites to get reviewed, but besides that, there is virtually zero mentioned about the company online, and I cannot find any reputable merchants selling their product. Does this business still exist? Was it ever a “real” company?

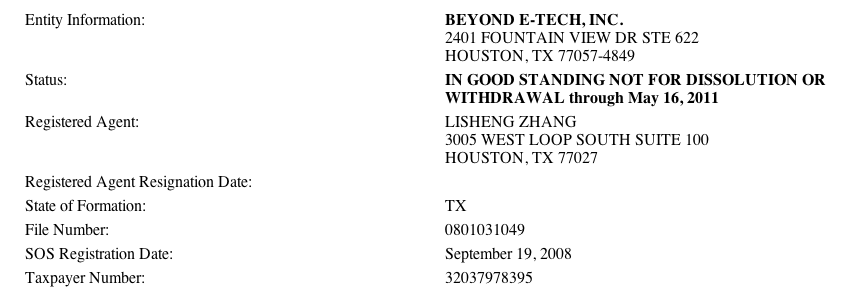

To dig deeper, I looked up Beyond E-Tech, Inc. on the State of Texas Comptroller’s website.

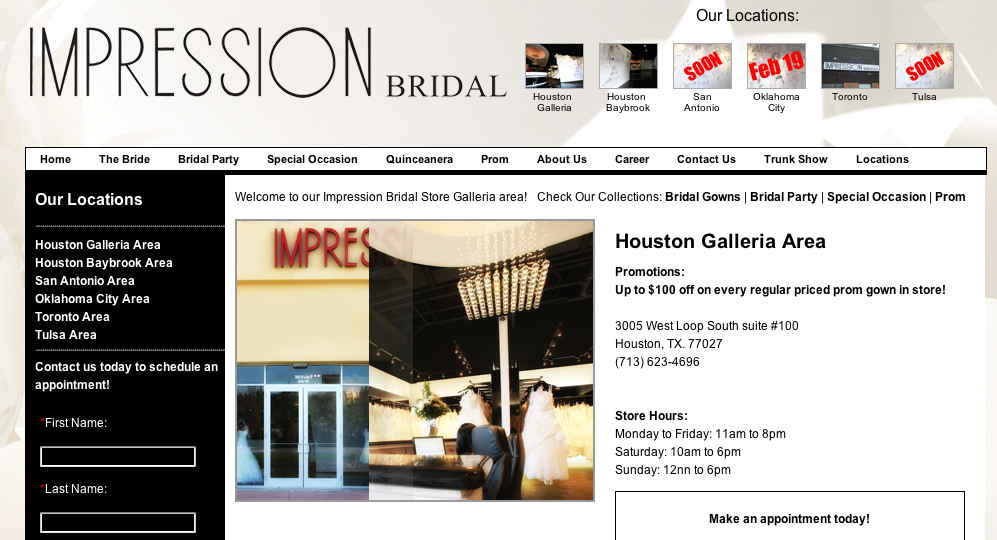

We see that the entity was created only two months prior to ABAT’s equity purchase, with the registered agent listed as: Lisheng Zhang, 3005 West Loop South Suite 100, Houston, TX 77027.

It turns out that 3005 West Loop South Suite 100 is actually the retail address of “Impression Bridal”.

Just to be sure, I called Impression Bridal and the friendly clerk informed me there was no Lisheng Zhang associated with that location.

A registered agent is a designated person who must be available during all business hours to receive service of process, otherwise, the company can automatically lose its corporate status and protection. This is important enough that every legitimate corporation is going to have legitimate registered agent information. (One can pay an “agent service” $70/yr to handle this)

Based on the above evidence, I wonder whether this is another sham transaction intended to funnel cash out of the company.

ABAT issued 11 million common shares to Chairman Fu and two other individuals to repay a “loan” which appears to be fabricated

In the company’s 2006 10-K, filed April of 2007, ABAT disclosed that it had entered into a contract in January 2005 with Chairman Fu and two other individuals. This purported contract “acknowledged” [ABAT’s wording] that these three individuals had loaned $4.8 million to ABAT and that this contract “provided” that ABAT would issue 11.2 million shares to satisfy $3.3 million of the loan ($0.33 per share). At the time that the disclosure was made, the stock was trading at $0.60 per share.

The loan is not listed in the 2005 10-K balance sheet or 2004 balance sheet. There was no explicit disclosure in the 2005 10-K or 2004 10-K under the related party transactions footnote.

I doubt this was an honest oversight because $4.8 million is greater than the total disclosed liabilities on the 2004 balance sheet. This so-called “loan” appears to be entirely fabricated. I doubt that Chairman Fu would lend money to the company without recording a liability in the financial statements.

Management has done many other related party transactions

The 2004 10-K risk factors include this gem:

RELATED PARTY TRANSACTIONS MAY OCCUR ON TERMS THAT ARE NOT FAVORABLE TO ADVANCED BATTERY TECHNOLOGIES.

What an understatement.

In addition to the egregious transactions described above, here is a brief list of “piggy bank” transactions:

2004-2005: The company sold goods to related parties. At the end of 2005, the company had a large account receivable from one of these parties. I believe this was, in effect, a kind of interest-free loan.

January 2006: Fu sells 30% of HLJ ZQPT to ABAT for 11 million shares. The company admits that Fu structured the transaction and the Board did not get a fairness opinion.

…It is likely that Mr. Fu will engage in other transactions with Advanced Battery Technologies and/or ZQ Power-Tech, including transfers of all or part of his interest in ZQ Power-Tech to Advanced Battery Technologies. It is unlikely that the Board of Directors will obtain independent confirmation that the terms of such related party transactions are fair.

January 2006: Fu sells a patent on “a nano material lithium ion battery and its production process” to the company for 4.4 million shares

2006: The company made interest-free, unsecured loans of $884,929 to companies owned by Chairman Fu.

Q1 2009: ABAT made an interest-free loan of $19,355 to a company where Fu sits on the board of directors

July 2009: The company agrees to lease a house from the Chairman for $4,000 per month.

Chairman Fu has sold an estimated 28 million shares since 2004

During the same time period, the company’s diluted share count tripled. The number of shares sold by Fu is greater than the shares outstanding at the time the company obtained its listing.

|

|

s/o |

Fu % |

Fu shares |

Shs rcvd |

Change |

|

2004 |

24.2 |

43.8% |

10.6 |

|

|

|

2005 |

41.0 |

19.5% |

8.0 |

|

(2.6) |

|

2006 |

50.6 |

15.8% |

8.0 |

15.4 |

- |

|

2007 |

49.4 |

15.8% |

7.8 |

11.2 |

(15.6) |

|

2008 |

54.2 |

14.4% |

7.8 |

|

(11.2) |

|

2009 |

58.0 |

15.7% |

9.1 |

|

1.3 |

|

2010 |

76.5 |

11.9% |

9.1 |

|

- |

|

|

|

|

|

Net Sales |

(28.1) |

This is an estimate that understates sales to the extent of options received, and overstates sales to the extent that any shares received in the related-party transactions went to other individuals. However, I believe it to be roughly correct.

The addition of 1.3 million shares in 2009 is explained by a 1 million share purchase that was part of the Wuxi transaction, and the balance (I believe) by options.

Despite a parade of auditors and multiple restatements, ABAT still has material weaknesses

Prior to 2006, ABAT was audited by PKF CPA in Hong Kong. HLJ ZQPT was audited by Rosenberg Rich Baker Berman & Company. For the fiscal years 2006-2008, ABAT was audited by Bagell, Josephs, Levine & Co (which later merged with Friedman). ABAT’s 2009’s audit was done by Friedman and 2010 audit by EFP Rotenberg. Auditor changes are a red flag, as they may be a sign of “opinion shopping.”

Another red flag: both Friedman and EFP Rotenberg identified material weaknesses.

Quoting EFP:

(a) a lack of expertise in identifying and addressing complex accounting issues under U.S. Generally Accepted Accounting Principles among the personnel in the Company’s accounting department, which has resulted in errors in accounting that necessitated a restatement of the financial statements for 2008 and 2009 and (b) inadequate review by management personnel of the Company’s reports prior to filing, which resulted in errors in prior filings that necessitated the filing of amendments to the 2009 Annual Report and the Quarterly Reports through the quarter ended September 30, 2010. [emphasis added]

Translation: Management does not understand GAAP and failed to read its own filings.

Not exactly confidence-inspiring.

ABAT’s RTO promoter, John Leo, is behind a number of suspicious Chinese reverse mergers, most notably CYXI

ABAT’s reverse merger was the brainchild of John C. Leo, who was also ABAT’s first public-company CFO. John Leo has been involved in a number of shady Chinese reverse mergers, most notably, China Yingxia (CYXI).

CYXI now trades on the Pink Sheets for $0.01 and two CYXI executives were sentenced to death in China for fraud. They made the mistake of defrauding Chinese investors prior to defrauding Americans.

How many $250 million companies cannot even get their own name right?

The “Exact name of registrant” in ABAT’s SEC filings is Advanced Battery Technologies, Inc., but the company's website alternately calls the company:

- United States Advanced Battery Technologies, Inc.;

- United States Advanced Battery Technology, Inc.;

- United States Advanced Battery Technology Company;

- USA Advanced Battery Technology, Inc.;

- U.S. ABAT Group (China) Co., Ltd.; or

- ABAT Group

(depending on which page you are on). None of these latter six names is listed in the company’s 10-K, and yet the company’s real name is nowhere on its website! If you were running a legitimate company with over $100 million in the bank, wouldn’t you be sure to get the name of your company right?

A more disconcerting question: is there an undisclosed “ABAT Group” Chinese entity holding assets that belong to shareholders?

Virtually zero fundamental institutional ownership

Looking at the list of top holders at 12/31, out of the top nine, seven are major index product providers, one is a “social” fund which appears to be a closet indexer, and one is a quantitative fund. None of these funds is likely to have done any due diligence on this company. There are no fundamental institutions with a significant shareholding. Another multi-hundred million market cap company with this characteristic was China MediaExpress (CCME). We all know how that turned out.

Conclusion

ABAT is the most egregious Chinese RTO I have seen. If the ownership status of HLJ ZQPT alone is not enough of a red flag, ABAT has a self-dealing management, falsely represented business description, serial equity issuances to acquire related or poor businesses, ludicrous profitability claims, customers that cannot be verified, multiple audit problems, the list goes on and on. This company has the dubious honor of achieving every major red flag that one looks for in a Chinese RTO fraud.

If CBEH is any guide, the market is eager to punish companies that do suspicious acquisitions funded by dilution. I would not want to be on the long side of this one.

Disclosure: At the time of publication, we and our affiliates are “short” ABAT through its common stock and options. We intend to profit from our short positions by covering, hedging, or otherwise unwinding them at lower stock prices. We reserve the right to add to or reduce our “short” positions at any time, and we do not intend to disclose these transactions, either before or after they are made. This article is provided for informational purposes only and is not a recommendation to buy or sell any security.

Catalyst

| show sort by |