| 2018 | 2019 | ||||||

| Price: | 2.18 | EPS | 0 | 0 | |||

| Shares Out. (in M): | 31 | P/E | 0 | 0 | |||

| Market Cap (in $M): | 68 | P/FCF | 0 | 0 | |||

| Net Debt (in $M): | 0 | EBIT | 0 | 0 | |||

| TEV (in $M): | 0 | TEV/EBIT | 0 | 0 | |||

Sign up for free guest access to view investment idea with a 45 days delay.

Description

Summary

180 Degree Capital is a closed end fund selling at an unjustified discount to (a growing) NAV due primarily to (1) indiscriminate / non-fundamental mechanical selling due to the fund’s conversion from a BDC to a CEF and (2) the market’s overlooking TURN’s most recent portfolio movements (including Turtle Beach, Mersana, and Synacor), which ought to contribute heftily to Q2 2018 NAV growth.

CEO Rendino (and multiple other insiders) have been purchasing shares personally in the open market, most recently increasing his stake by 15% on May 15, 2018. The Company also has buyback authorization in place up to $2.5 million by August 21, 2018, while a greater portion of NAV is turning into cash, most recently with the sale of Adesto Technologies (IOTS).

Short-term opportunity: As NAV grows and is appreciated by the market, discount ought to continue to narrow, for a relatively straightforward path to ~30% upside over the next 3 to 6 months.

Long-term (12+ months) opportunity:

-

Excess monetization of private investments: D-Wave is likely nearing an IPO (1-3 years) and is one of the only pure-play quantum computing assets. It is held on the balance sheet at $10 million. AgBiome recently received another round of funding form the Gates Foundation.

-

Formation and scaling of the broker-dealer business: TURN’s first SPV in TheStreet was a success, and TURN has closed on its second SPV in April 2018. Illustratively, scaling the business to $200 million in AUM could bring in management fees equal to ~3% of the NAV.

-

Optionality in new CEO Kevin Rendino’s deal-making ability: Given other entities trade at premiums to NAV / book given their operators, one ought to not rule out the possibility that TURN could eventually trade at a premium given a demonstrated ability thus far to find creative ways to increase value.

This is a microcap, so the usual disclaimers apply...

Business Overview

180 Degree Capital was formerly Harris & Harris Group, Inc, a BDC investing in private companies. In December 2016, Harris and Harris announced it would separate into 180 Degree Capital Corp and HALE.life Corp, separating its health and medicine assets from its existing portfolio, which was completed in March 2017. Concurrently with the transition to a closed end fund, new CEO Kevin Rendino began running TURN. Rendino previously worked for 20+ years on the Basic Value Fund at BlackRock with ~$13 billion in assets. He writes quarterly shareholder letters that I’ll let everyone else come to their own conclusions on. It’s worth noting that he has no outside funds / conflicts of interest; this is his full-time job. At the least, he talks the talk, and we believe he has also demonstrated creative ways to create value. More on that shortly.

Since Q1 2017, the Company reduced expenses, previously running ~$1.6 million per quarter on average over the previous 5 years, down to $740k today. This happened with relatively easy steps such as laying off staff and moving offices from NYC to New Jersey ($300k annual rent is now just $34k).

Each of the 3 private investments that consist of over 5% of NAV have been stable in value, with AgBiome growing in value with new funding rounds and increased in comps values.

Private (Legacy) Investments

AgBiome

AgBiome provides early-stage research and discovery for agriculture and utilizing the crop microbiome to identify products that reduce risk and improve yield. AgBiome received a series A in April 2013 and November 2014 for $17.5 million each, followed by a $34.5 million series B from the Gates Foundation in August 2015, and finally a multi-year $6.8 million Gates Foundation Grant in July 2016. Value to TURN over the past two years has grown from $5.7 million to $11.1 million today.

D-Wave

D-Wave is a Canada-based quantum computing company. Per the company,

- D-Wave is the leader in the development and delivery of quantum computing systems and software, and the world's only commercial supplier of quantum computers. Our mission is to unlock the power of quantum computing for the world. We believe that quantum computing will enable solutions to the most challenging national defense, scientific, technical, and commercial problems.

Quantum computing works on an entirely different plane than classic computing; classic computers operate binarily (0 or 1), while quantum computers operate on quantum bits, which can be in superpositions. While quantum computers aren’t expected to replace classic computers, they would theoretically be literally millions of times faster, enabling breakthroughs in a variety of industries.

The company has customers and partnerships with companies such as Google, NASA, Lockheed, and Volkswagen. Most recently, D-Wave announced a Quantum Cloud (read: AWS on steroids) customer win in Oak Ridge National Lab, and the launch of a “Quadrant” machine learning business unit in May 2018.

Per Rendino on the Q4 2017 call,

The way D-Wave is going to have – is going to come monetize for them to execute a couple of more things they need to do in making their quantum computing IP more commercial and more cloud oriented. If they can do that and the management decides and the board decides it's time then they'll be companies like Google and Amazon and Microsoft and IBM and the rest that probably will clamor to own it.

If they want to continue to think that they can become a $10 billion or $20 billion or $30 billion business by constantly waiting for good dough, and always waiting for something else to happen in order for that to happen, then those same companies that may be a buyer of that business are going to leapfrog them and D-Wave is going to end up as an also-ran company.

Thus, Rendino is putting pressure on management and the board to monetize sooner rather than later. This would most likely be in the form of an IPO, though given the strategic nature of the asset, IBM, MSFT, GOOG, etc. could bid and it’d be a drop in the bucket.

There is also an element of optionality in TURN through D-Wave, as there are very few – if any – pure-plays on quantum computing. Should the market get bulled-up on the technology in the same way that we’ve seen in technologies such as 3D printing, AI / Machine Learning, IoT, or most recently in crypto, TURN would likely see substantial inflows. There are already people who want to buy the stock,

Anecdotally, Rendino has said that he wouldn’t be surprised to see a $40 million valuation on TURN’s stake vs. the current $10 million. Each $10 million in incremental value is $0.32 per share.

HZO, Inc

HZO manufactures thin-film nanotechnology that protects electronics from corrosive damage in the assembly process. The result is that manacturers can create new products and features that would it would otherwise be incapable of creating. The Company’s website features case studies from recognizable customers such as Nike, Motorola, TAG Heuer, and Dell, to name a few. The Company most recently had its Nanosys technology featured in next-gen Samsung televisions.

HZO has received a total of $48.6 million in funding, per Crunchbase. TURN’s cost basis is $9.1 million vs. a current $6.8 million. Valuation has improved sequentially in the past 2 quarters.

Synacor Inc.

Synacor is one dark spot on the record thus far. TURN’s cost basis is $3.9 million vs. a current value of $2.5 million. The company provides managed internet portals on behalf of its customers (ex: log in to AT&T or HBO Go). It was awarded a massive AT&T contract in 2016, but fell heavily in August 2017 when it announced revenue delays in that deal while keeping long-term guidance intact. Management has lost credibility, but TURN still believes the stock offers value. Letters provide additional commentary.

Public Investments

Adesto Technologies (IOTS)

Harris & Harris was an original investor in Adesto while private, which turned into equity upon the company’s October 2015 IPO. Rendino has been selling down the position, most recently filing an amended 13D on May 21 showing 760,322 shares against the 1.5 million in Q1. This position turning into cash ought to only improve the relative discount to NAV.

TheStreet (TST)

TURN provided a total $7.85 million financing in TheStreet (TST), which included $4.0 million from TURN’s balance sheet and $3.85 million from a fund managed by 180 (family office and HNW). Note that the latter funds aren’t consolidated, but TURN recognizes fee income. The company retired the preferred stock and Rendino subsequently joined the board. At time of investment, TST traded at less than 1x EV to revenues, with 90% recurring subscriptions, and TURN believed it was worth 2x that based on comps. Rendino also provided commentary on managing outside capital,

The TST transaction also affords us the opportunity to manage third-party capital, which provides 180 with income and the potential for additional returns on invested capital. It also allows us to take advantage of opportunities for investment that would otherwise be difficult to complete solely from cash on our balance sheet.

Between stock, options, and RSUs, TURN’s cost basis is $4.9 million, while currently valued at $8.3 million.

Turtle Beach Corporation (HEAR)

Turtle Beach is the leading headset provider (over 40% share) to the gaming industry (PC, Xbox, Playstation, etc.). Part of its initial mispricing arose as it had a complex balance sheet, with $19 million of preferred stock. TURN invested $3.5 million in HEAR at $3.50 per share as HEAR took out its preferred stock on April 27, 2018. Note that the company had already reported preliminary Q1 numbers of positive EBITDA and revenues up 174 to 181% YoY on April 9, 2018; this information was already “in the market.” This growth is part due to e-sports popularity in general, yet more so due to the growth of the Battle Royale game format (Fortnite), which lends itself to headset use. HEAR has since rallied to over $17 per share as of this writing, on the back of full Q1 2018 results and a strong full-year guide to $26 million in EBITDA.

Given the substantial rise in the stock at such a rapid pace, one might believe that this poses a substantial risk to TURN’s NAV. I think this is a mistake. Even with HEAR at $18 / share, the company would trade at a pro forma EV to Revenues of ~1.6x and EV to EBITDA of ~13x, which isn’t especially egregious for a company growing revenue by ~37% in 2018. Given now over a $200 million market cap, shops such as Craig Hallum, Barrington, etc. will likely come of the woodwork with buy initiations and stories around long-term growth in e-sports and gaming. However, there’s always the option to short HEAR to better isolate the discount to NAV if one wishes.

USA Truck, Inc (USAK)

USA Truck is a truck logistics services business. Upon 180’s initial investment, USA was in the midst of a turnaround, having recently installed a new management team. Shares traded at 3x EBITDA vs. a longer-term average of 5.4x. TURN initially invested $1.6 million in USAK at $6.59 per share, while shares currently trade at $26.70. TURN currently holds no position, yet the investment again illustrates Rendino’s skill in the space.

As a side note, Rendino tends to have a unique personality and is unafraid of confrontation. See comments from the Richardson Electronics (RELL) Q4 2017 conference call,

On the Xplore Technologies (XPLR) Q4 2017 conference call,

Valuation / Short-term Opportunity

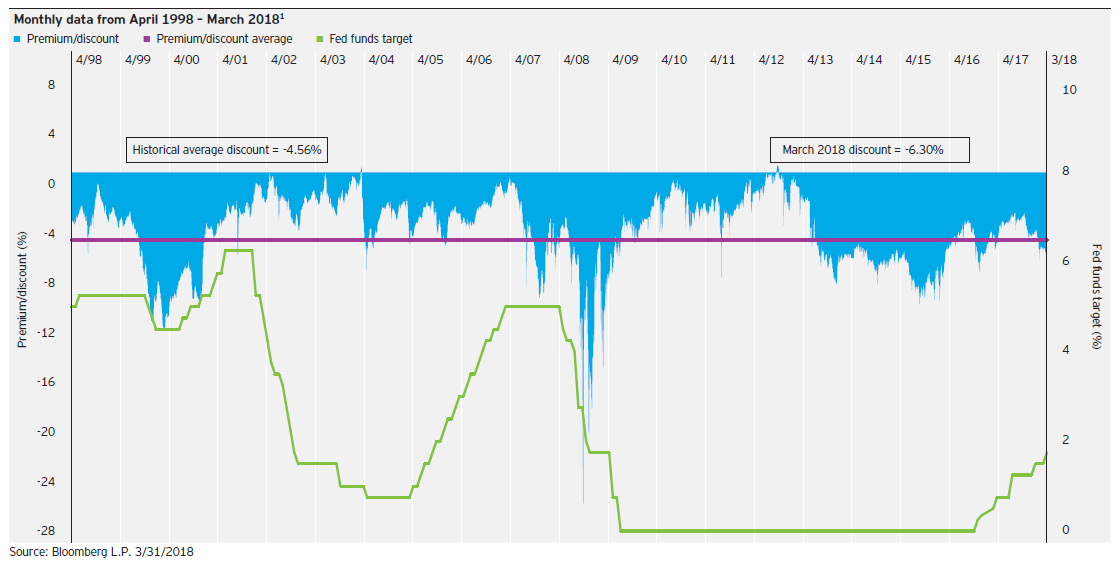

In the near-term, TURN’s NAV in Q2 2018 ought to be substantially higher given: mark to market movements in the portfolio, especially the Company’s $1 million investment in Turtle Beach (HEAR). Historical CEF discounts are typically low to mid-single-digits, with major discounts typically occurring in a period of tremendous market distress (00 and 08), or on an individual basis when managers have a history of destroying value.

Neither of these are the case any longer at TURN. Rather, the Company is merely an orphaned equity after having converted from a BDC to a closed end fund in March 2017, while the previous management team destroyed value. As shown, the Company’s discount to NAV has tracked closely alongside growth in NAV, as the market becomes more or less confident regarding future prospects.

Given what ought to be substantial NAV growth in Q2 2018 as well as a more liquid NAV, the discount ought to continue to close, for ~30% upside.

Additional sources of upside not included in NAV above include:

-

TURN holds $68 million in NOLs that don’t begin to expire until 2026, and $21 million in capital loss carryforwards (no expiration). If the fund utilizes just 25% of these carryforwards at a 20% tax rate, that’s worth $0.14 per share.

-

TURN does not recognize accrued incentive fees. Given the TST SPV success thus far, this ought to add another ~$0.04 at current TST prices, notwithstanding future SPVs.

-

D-Wave stake is currently recorded at $10 million. As mentioned, Rendino thinks there could be upside here on monetization either via an IPO or strategic buyout.

As a comp, Pender Growth Fund (TSXV:PTF) is a CEF that also holds a stake in D-Wave. 87% of NAV remains in private unlisted investments, yet the fund trades at $4.25 vs. an NAV on April 27 of $4.42, or a less than 4% discount.

Long-term Opportunity

In the longer-term, TURN also holds upside through (1) excess monetization of private assets and (2) development of the broker-dealer business. The former is relatively straightforward; the value of TURN’s three largest private holdings has been growing in aggregate, and given trends in quantum computing (D-Wave) and recent valuation rounds (AgBiome), it seems likely that these could end up contributing to further NAV growth in the same way that was seen in Mersana Therapeutics’s IPO.

With respect to the broker-dealer business, 180 started managing outside capital for the first time through an SPV in Q4 2017. TURN also hired Robert Bigelow as Head of Fund Development in October 2017. Bigelow formerly worked at Bear Stearns and founded Blue River Asset Management, which managed $1.7 billion at its peak.

Given disclosure that the Company accrued $7,161 in management fees from November 10 to December 31, 2017, the management fee looks to be ~1.33%. This is not a large number, yet it lowers “net expenses” so to speak in the near-term, while the opportunity to scale is already being taken advantage of. The SPVs also have incentive fees, yet the Company doesn’t accrue for it. Given TST’s performance merely from November 10, 2017 to December 31, 2017, this figure is ~$110,000. Given TST has risen an additional ~24% YTD, this incentive fee should come through nicely.

As of Q1 2018, management stated they are currently targeting completing the licensing process in Q2 2018. On April 18, 2018, the Company raised $3.35 million in capital for the second SPV, with the target company yet to be announced. If one does a little poking around on whose transcripts Rendino tends to show up on, one could venture to guess which company this might be.

In the next 2-3 years, it’s conceivable to see the strategy scale to larger companies / more AUM. Though the initial focus has been on hitting singles and doubles (and a home run in HEAR), letters have noted an “initial focus” on <$100 million market capitalization public companies, yet broader language remains,

“Future investment focus in value creation through constructive activism in what we believe are deeply undervalued public companies.”

I’d be hard-pressed to think that after 20 years on a large cap fund and given recent wins, that he doesn’t have some additional capital that could become available. Partnerships are an additional option; Rendino has stated as much,

“We believe that our new simplified structure and focus could lead to partnerships or other opportunities.”

For illustrative purposes, $200 million in capital at 1.25% management fees (excluding incentive fees) would be worth ~3% of the current NAV.

Risks

Private portfolio is monetized below marked values

Rendino is a terrible investor / destroys capital

Ongoing expenses eat into NAV faster than NAV grows

Conclusion

TURN offers a clear path to ~30% returns 3-6 months as the market gains greater visibility on (1) NAV stability and growth, especially in Q2, (2) NAV discount closing on a new investor base post-BDC conversion, and (3) Rendino’s ability and long-term plans. D-Wave / private investents are a free option, and given that entities such as BOMN and SYTE trade at substantial premiums to NAV, it's not far-fetched to see TURN trade at a premium as well.

I and/or others I advise hold a material investment in the issuer's securities.

Catalyst

NAV growth

Discount closes

| show sort by |